This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

For example, there might be a bucket for income received (sales), another for money spent on supplies (expenses), and accounts for things like cash on hand, money owed to you by customers (accountsreceivable), and money you owe to vendors (accounts payable).

Consisting of a series of steps, the accountsreceivable process refers to the money owed to a business for the purchase and delivery of goods or services. Accountsreceivable (AR) provides the critical link between making the sale and receiving payment.

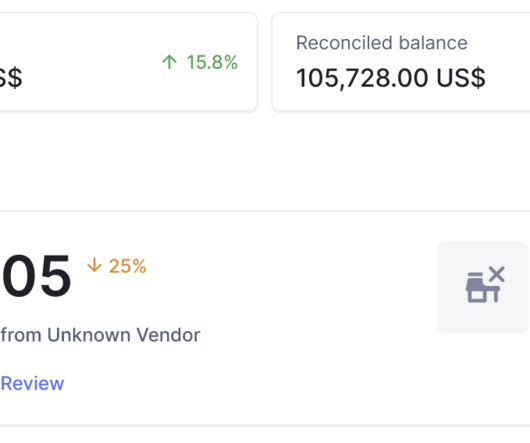

Accountsreceivable reconciliation is a crucial process within accounting and financial management practices undertaken regularly by a business. As transactions with customers and clients occur, businesses generate accountsreceivable, which represent amounts owed to them for goods and services sold or rendered.

An accountsreceivable balance refers to a company’s outstanding invoices that customers have not yet settled. In other words, it is the amount of money owed to a business by its customers for goods or services provided but for which it has not received payment.

Accountsreceivable is a fundamental concept in business finance, serving as an essential component of a company’s working capital and cash flow management. This article aims to demystify the accountsreceivable process, elucidating its significance, operational mechanisms, challenges, and optimization strategies.

The end of month close process plays a vital role in ensuring the accuracy, integrity, and transparency of financialrecords for businesses of all sizes. Its primary purpose is to ensure the accuracy and completeness of financialrecords so that financialstatements can be prepared for internal and external reporting purposes.

Picture this: a team of expert bookkeepers diligently managing your financialrecords and transactions without setting foot in your office. Traditional bookkeepers are professionals responsible for recordingfinancial transactions, maintaining ledgers, and preparing financialstatements manually or using basic accounting software.

Substantive testing is an audit procedure that examines the financialstatements and supporting documentation to see if they contain errors. These tests are needed as evidence to support the assertion that the financialrecords of an entity are complete, valid, and accurate. What is Substantive Testing?

A Certified Public Accountant is an accounting professional who performs tasks such as auditing books or analyzing financialstatements. CPA Jobs and Specializations CPAs have the opportunity to move into different accounting jobs throughout their careers. What Is a CPA?

Forcast A/R and More with Gaviti Gaviti’s accountsreceivable automation solution streamlines your A/R processes and helps your team work better. Statement analysis: This approach looks at a company’s financialstatements to see trends and relationships between different factors and cash flow.

Nowadays, when it comes to maintaining financialrecordstatements and account books for businesses, it has become a highly stressful and cumbersome task. We, at Outsourced Bookkeeping, provide accounts payable services to organizations and businesses.

Facilitating Tax Compliance Tax time can be daunting for small business owners, but meticulous record-keeping makes the process smoother. By maintaining accurate financialrecords, businesses can easily report income, expenses, and deductions, minimizing the risk of errors or audits.

Proper bookkeeping basics practices ensure accurate financialrecording, allowing you to make informed decisions and comply with legal and tax requirements. In this guide, we will explore the essential accounting principles every small business owner should know. But one aspect that should never be overlooked is bookkeeping.

Source documents are the physical basis upon which business transactions are recorded. Source documents are typically retained for use as evidence when auditors later review a company's financialstatements , and need to verify that transactions have, in fact, occurred. For example, a company is in the consulting business.

Book Reconciliation entails the comparison of different types of financialrecords of a company. These records may be internal financialrecords or external. Companies maintain various internal records to track their financial activities accurately and ensure compliance with accounting standards.

Even though a CPA may comprehend the value of keeping precise financialrecords, guaranteeing compliance with tax rules can be a difficult undertaking. CPAs can assign work such as bank reconciliations, financialstatement creation, and data entry to a group of qualified experts by using bookkeeping services.

This article compares and contrasts between them and identifies the required abilities for accounting professions. To know more about Accounting Technicians vs Accountants, develop financialstatements, and prepare reports for tax purposes, Contact Billah & Associates.

By implementing the right strategies and utilizing modern technologies, businesses can overcome these accounting hurdles and ensure a smoother financial flow. Let's explore some common accounting problems and their solutions. One of the major problems faced by businesses is material errors in financialstatements.

An audit is an independent examination of a company’s financialstatements by a licensed auditor. The purpose is to ensure that the financialstatements accurately reflect the company’s financial position and comply with the Singapore Financial Reporting Standards (SFRS) and the Companies Act.

You’re not maintaining accurate financialrecords It’s imperative to maintain organised financialrecords, not just to remain in compliance with the IRAS and financial auditors, but also to present a comprehensive view of your company’s financial position to potential investors.

You’re not maintaining accurate financialrecords It’s imperative to maintain organised financialrecords, not just to remain in compliance with the IRAS and financial auditors, but also to present a comprehensive view of your company’s financial position to potential investors.

Running a small business can cause you to shoulder a lot of burdens, especially in the financial realm. Keeping track of revenues and expenditures to maintain a proper cash flow must be cautiously organized so that you are not off track on your funds or financialrecords when you are filing taxes.

Introduction to Bank Reconciliation Journal Entries Bank reconciliation is an important process in accounting that ensures the accuracy and integrity of a company's financialrecords. It involves the comparison between the company’s internal financialrecords and those of the bank.

They specialize in custom talent selection and training for accounting systems and excel in modern cloud accounting software. Besides bookkeeping, they can handle other accounting tasks, with potential tax law training needed. Outsourcing can provide consistent and reliable record-keeping.

Matching and validating entries would mean data consolidation across sub-ledgers, vendor invoices, bank statements, receipts, and accountreceivables to ensure timely and accurate month-end and year-end closing of the financial books. Each balance should match its corresponding entry in the general ledger for any source.

Lack of accountreceivable services is also one of the many reasons in this case. Inaccurate records in finance – Precise financial documentation is vital to facilitate shrewd business choices. By doing so, they can effectively manage their finances.

In simple terms, the accounting cycle refers to the series of steps that businesses follow to record and process financial transactions, from identifying the transactions to preparing financialstatements. The accounting cycle is a series of steps that businesses follow to record and process financial transactions.

Substantive procedures are intended to create evidence that an auditor assembles to support the assertion that there are no material misstatements in regard to the completeness, validity, and accuracy of the financialrecords of an entity.

The Role in Maintaining Compliance & Detecting Fraud In addition, payment reconciliation plays a key role in ensuring compliance with tax regulations and accounting standards. Accurate financialrecords are essential for businesses to meet auditing requirements and avoid potential fines or penalties for non-compliance.

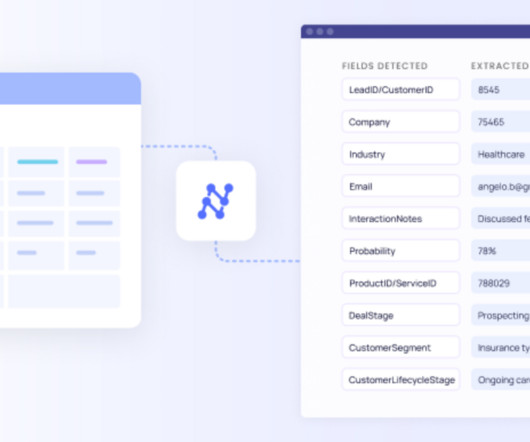

This article will provide a comprehensive understanding of account reconciliation, the benefits and challenges of outsourcing this activity, and the transformative potential of automated reconciliation software. Integrate Nanonets Reconcile financialstatements in minutes Try for Free What is Accounts Reconciliation?

Recording transactions, Managing accountsreceivable and payable, Monitoring the cash flow, Reconciling bank accounts, Creating journal entries, Issuing invoices, Payroll tax preparation, income tax, sales tax, tax return, etc. What Is the Difference Between a Full Charge Bookkeeper and an Accountant?

A bookkeeper is a person responsible for handling a company’s financialrecords, ensuring accuracy and organization. These professionals record and enter every cost and revenue in a ledger or accounting software. Feeling overwhelmed and making mistakes in financialrecords are clear indicators.

The General Ledger is a central accountingrecord that contains all financial transactions of a business, organized in a systematic and structured manner. The GL comprises various accounts, each representing a specific financial aspect of the business.

Benefits of Outsourced Bookkeeping for Tax Planning and Compliance Ensuring correct financialrecords is essential for organizations to be able to come up with wise decisions and increase revenue. They may ensure that firms are fulfilling all filing dates, recommend tax deductions, and offer expert guidance on tax-saving techniques.

Our blogs regularly detail how professional bookkeeping can help businesses survive and thrive beyond simply recording transactions and preparing tax filings, like driving profitability with financial reporting , forecasting cash flow , and optimizing your accountsreceivable.

Gain Insight: Choose software that provides detailed tracking of income, expenses, and overall financial performance to maintain a clear view of your business’s financial health. Maintain Separate Business and Personal Accounts Avoid Confusion: Keep business and personal finances separate by opening distinct bank accounts.

Billing Clerk The billing clerk position is responsible for invoicing customers, submitting the invoices to customers by whatever means are required, issuing credit memos, and keeping the billing records up-to-date. Bookkeeper The bookkeeper position originates accounting transactions and compiles the information into financialstatements.

Whether you are a new entrepreneur or searching for ways to expand your business, the following tips will help you with your bookkeeping and accounting: 1. Have an organised filing system Setting up an organised system for tracking your spending will make it easier to record expenses and generate financialstatements.

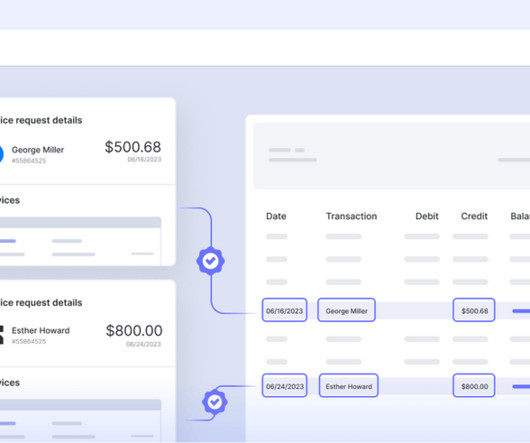

A balance sheet is a financialstatement that provides a snapshot of a company's financial position at a specific point in time. Balance sheet reconciliation is a critical financial process that aligns the financialstatements with external documentation such as bank statements, invoices, and general ledger entries.

It's a process that ensures every payment, adjustment, or write-off tied to an invoice is accounted for and settled. There are no messy records, just tidy transactions. It paves the way for flawless financialrecords, better cash flow, and smooth business operations. Which business owner wouldn't want that?

Intercompany accounting is significantly more complicated than standard accounting since it requires balancing multiple ledgers, tracking internal/external transactions, forex conversion, performing intercompany eliminations and settlements, and preparing a consolidated financialstatement.

Expense reconciliation is a process within finance and accounting that ensures that a company's financialrecords accurately reflect its spending activities. At its core, it involves comparing financial data from various sources within a business to identify any discrepancies or errors and bring them into alignment.

When you first started out, you were paying for business expenses out of your personal bank account and tracking your accounts payable and accountsreceivable using different methods or separate software programs. But the health of your now-thriving business depends on understanding its financial situation.

In simple words, bookkeepers ensure that all of your business income, expenses and transactions are recorded in your book and they reconcile your company’s financialaccounts every month. In addition to that, bookkeepers can also help you prepare your company’s financialstatement and financial report.

We organize all of the trending information in your field so you don't have to. Join 52,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content