This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

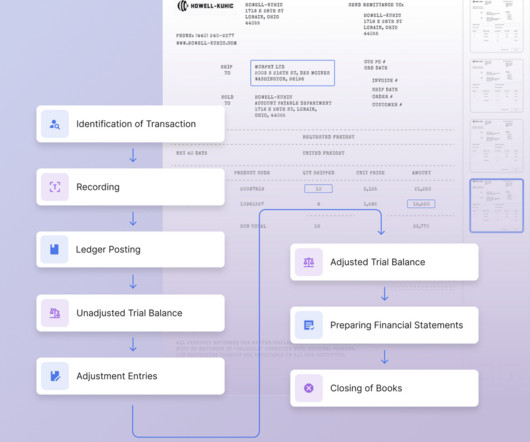

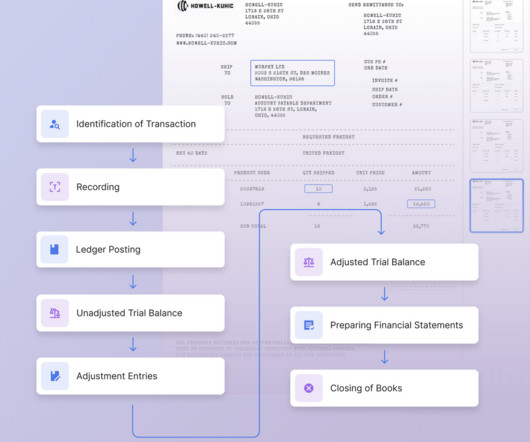

What Is a BankReconciliation Statement? A bankreconciliation statement is a financial document that compares a company's bankaccount balance to the transactions recorded on its general ledger, often called the "cash books." How to perform a BankReconciliation?

BankReconciliation Vs. Book Reconciliation In accounting and financial management, we encounter the terms "Book Reconciliation" and " BankReconciliation " These terms are often used interchangeably, leading to ambiguity regarding their meanings. What Is BankReconciliation?

BankReconciliation is the process of matching the company's cash books to the bank statement. Reconciliation includes matching the company’s balance sheet, income statement, bank statements, and expenses. Bankreconciliation is crucial for identifying and minimizing such losses.In

BankReconciliation is the process of matching the company's cash books to the bank statement. Reconciliation includes matching the company’s balance sheet, income statement, bank statements, and expenses. Bankreconciliation is crucial for identifying and minimizing such losses.In

Accounts payable will need to keep on top of the ever-changing environment and keep up to speed with new security threats. Best practices should include performing daily bankreconciliations, so any unusual activities can be spotted as soon as possible. This would further reduce AP employees' manual workload.

Even though a CPA may comprehend the value of keeping precise financial records, guaranteeing compliance with tax rules can be a difficult undertaking. CPAs can assign work such as bankreconciliations, financial statement creation, and data entry to a group of qualified experts by using bookkeeping services.

It’s a crucial step to ensure that you prepare an accurate set of statements for financial reporting, planning, and tax compliance. Closes can be quite stressful as the general turnaround time is <1 week, while you just have 2-3 days to reconcile all your accounts. Here is how you can do monthly reconciliation.

Why is it Important to Reconcile your BankAccount? Reconciliation is a crucial accounting process that ensures the accuracy of the financial close process. It ensures that the money credited or debited in your bankaccount matches the money being expended or made. How do you reconcile your bank statement?

Credit card reconciliation is important for businesses and individuals alike. For businesses, credit card reconciliation ensures that all expenses are properly accounted for and reported. This is important for tax purposes and financial reporting. link] Use a reconciliation template and open it on your Excel.

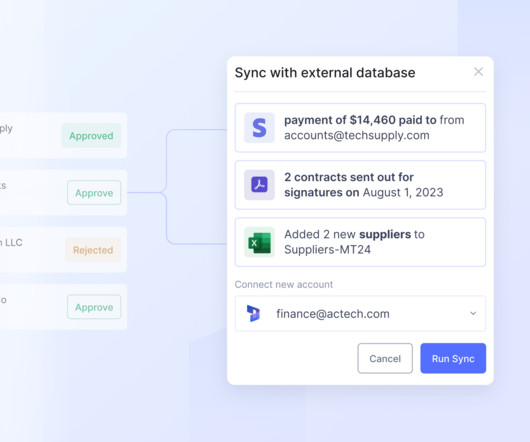

To ensure the integrity of financial data, accountants and bookkeepers rely on the general ledger accountreconciliation process. This process involves comparing general ledger accounts with supporting documents using reconciliation software to identify discrepancies and take corrective measures.

Accurate financial reporting is essential for business and food tax purposes. The ramifications can be severe without proper accountingreconciliation. From underpaying taxes to potential fines, not getting an accurate picture of the business can be detrimental. Trying to handle it alone can be challenging.

That’s where the best accounting software for CPAs and accounting firms comes into play. Comprehensive compliance and reporting The best accounting software for CPAs and accounting firms should have comprehensive compliance capabilities that are updated to keep up with changing rules.

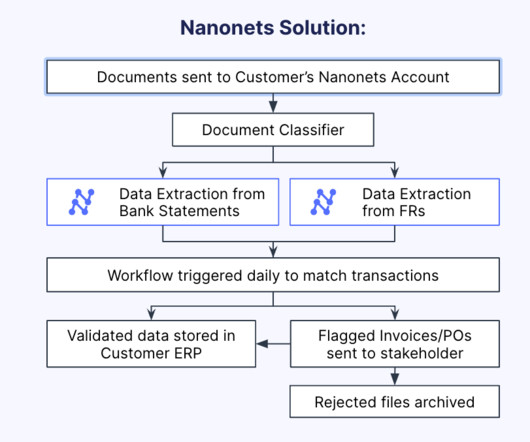

The following table presents the best features of a few popular Payment Reconciliation Automation Tools Software Key Features Nanonets - Automated document processing - Data extraction - Data matching - Workflow automation - Centralized repository Oracle Netsuite - Cloud-based suite of financial management solutions (..)

QuickBooks Payroll Although it works automatically with QuickBooks, QuickBooks Payroll is a QuickBooks app that brings together payroll, HR, tax compliance, and health benefits – everything you need to make it through another payroll cycle. When tax time comes, you’ll be so glad to have both of these tools in your arsenal.

We organize all of the trending information in your field so you don't have to. Join 52,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content