This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

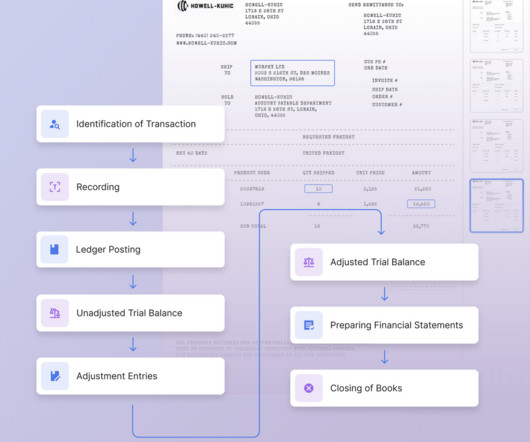

What is a Reconciling Item? A reconciling item is a difference between balances from two sources that are being compared. These items are stated in an accountreconciliation , so that the balance from one source is adjusted by reconciling items to arrive at the balance from the other source.

Related Courses Bookkeeper Education Bundle Bookkeeping Guidebook What is an AccountReconciliation? An accountreconciliation is the actions taken to prove that an account balance is valid. Accountreconciliations are also useful for spotting instances of inappropriate purchases.

An entry reverses a transaction that was in a prior year, and which has already been zeroed out of the account. Related Articles Account Analysis AccountReconciliation Books of Original Entry Final Accounts How to Reconcile an Account The Aging of Accounts

Why is it Important to Reconcile your Bank Account? Reconciliation is a crucial accounting process that ensures the accuracy of the financial close process. It ensures that the money credited or debited in your bank account matches the money being expended or made. How do you reconcile your bank statement?

If so, the liability suspense account is classified as a current liability. Related Articles Account Analysis Accounting Adjustments Accounting System Design AccountsReconciliation (podcast) How to Reconcile an Account When an Accounting Error is Material

As part of the closing process, the accounting staff may engage in the following reconciliation activities: Reconcile the bank statement Reconcile balance sheet accounts to the supporting detail Reconcile inventory records to on-hand balances (if a periodic inventory system is used) Reconciliations are considered an important control activity.

If they match, it means your records and the bank statement are reconciled, and there are no discrepancies. Why is it important to reconcile your bank statements? It's important to reconcile bank statements to identify errors, detect fraud, and maintain an accurate ledger. We have discussed the benefits of reconciliation.

These worksheets may be provided to the auditors as part of the annual audit , as evidence that the balance sheet accounts are correct. Related Articles AccountsReconciliation (podcast) How to Reconcile an AccountReconciliation Statement

How to Conduct an Account Analysis A good way to conduct account analysis is to itemize the contents of an account on a single worksheet of an electronic spreadsheet, and assign the month-end date to that worksheet page. Reconcile the detail on the worksheet to the account balance.

This report provides a detailed overview of the current financial position by listing all accounts payable transactions and their corresponding balances. It allows businesses to reconcile their accounts, identify any discrepancies, and ensure that all payments are accurate and accounted for.

Accountreconciliation Empower staff to assist with reconciling the AP liability account. Bank reconciliation Check bank statements against internal records to ensure all transactions are reported. And the other is, and this is back to the basics, what’s the benefit of accounts payable automation?

Users can categorize expenses, reconcileaccounts, and generate reports all from QuickBooks. Some QuickBooks add-ons just make sense, and this is definitely one of them. With Bill & Pay, automatic invoicing, accountreconciliation , and auto-payments are easier than ever.

Understanding the basics of payroll accounting, the importance and general processes, and how to include automation are vital areas to maximize growth potential and minimize the risk of costly errors. What is Payroll Accounting? Step #5: Reconcile Payroll The final stage of payroll accounting is to complete the payroll reconciliation.

Accounts payable (AP) is a challenging job that demands professionals to juggle numerous tasks simultaneously, from data entry to accountreconciliation to monthly reporting. I am definitely here for it. 15:18 CHRIS ELMORE It’s been a while since I’ve been kind of on a main stage at a conference.

We organize all of the trending information in your field so you don't have to. Join 52,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content