This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Reconciling your bank accounts means matching up your accounting software to your bank statements. When you only work with an annual taxaccountant, this doesn't happen very often. In fact, it's on our list of the top three small business accounting mistakes.

Guide to the Vendor AccountReconciliation Process Running a business involves collaboration with various vendors who provide different kinds of products and services. Vendor reconciliation , a crucial part of this process, involves scrutinizing purchase-related documents to ensure accuracy in all vendor transactions.

Easing the Pressure of Skilled Talent Shortages An exciting AI application in the accounting world is its potential to enable non-tax professionals to take on some of a firm’s workload, allowing CPAs to work more efficiently and focus on strategic tasks that require their expertise.

Why is it Important to Reconcile your Bank Account? Reconciliation is a crucial accounting process that ensures the accuracy of the financial close process. It ensures that the money credited or debited in your bank account matches the money being expended or made. How do you reconcile your bank statement?

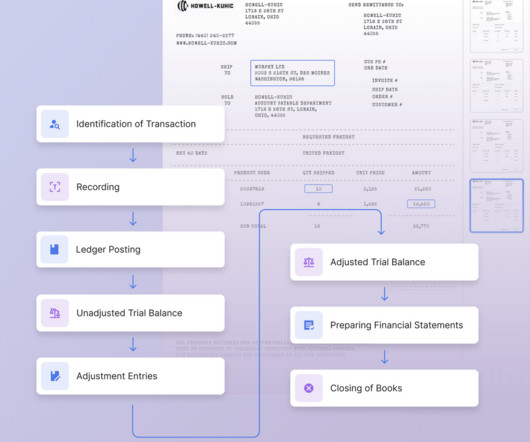

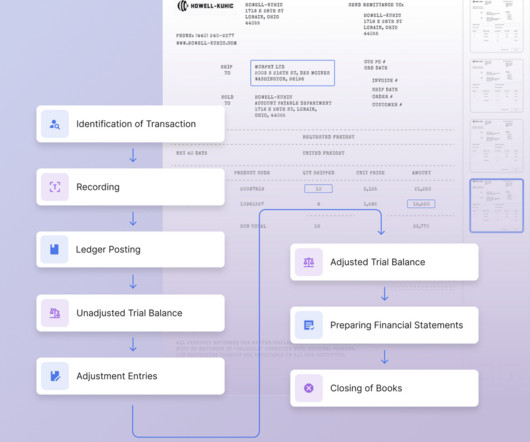

Month-end close is a widely accepted accounting standard that is aimed at keeping an accurate set of financial records and detecting errors/fraud. It involves recording, reviewing, and reconciling records at the end of every month. Month-end reconciliation is the most important part of the month-end close process.

To ensure the integrity of financial data, accountants and bookkeepers rely on the general ledger accountreconciliation process. This process involves comparing general ledger accounts with supporting documents using reconciliation software to identify discrepancies and take corrective measures.

Reconciliation includes matching the company’s balance sheet, income statement, bank statements, and expenses. Having an accurate set of financial statements is essential, or it can lead to complications in financial planning, tax compliance, and legal matters. Why is it important to reconcile your bank statements?

Reconciliation includes matching the company’s balance sheet, income statement, bank statements, and expenses. Having an accurate set of financial statements is essential, or it can lead to complications in financial planning, tax compliance, and legal matters. Why is it important to reconcile your bank statements?

While the year-end closing process is familiar to most due to tax reporting, it’s not the only necessary period-end process a business should have. The month-end closing process is just as essential, especially if you want to avoid the headache and overwhelm of last-minute error corrections spanning months during tax seasons.

Accurate financial reporting is essential for business and food tax purposes. The ramifications can be severe without proper accountingreconciliation. From underpaying taxes to potential fines, not getting an accurate picture of the business can be detrimental. Trying to handle it alone can be challenging.

Bank Reconciliation is a subset of Book Reconciliation, wherein the ledger figures are compared against the entries in a bank statement. This essay will describe book reconciliation and its types, including bank reconciliation, and show how all forms of accountingreconciliation are essential for effective financial management.

Also, credit card reconciliation is the process of confirming that all transactions on your credit card statement are properly reflected in your accounting records. Credit card reconciliation is important for businesses and individuals alike. This is important for tax purposes and financial reporting.

After noting the discrepancies flagged by the general ledger and the bank statement, note how the bank account balance changes over the next few days. Ascertain the impact and note any unnoticed entries that hit the bank account. Reconciling transactions across these various accounts and currencies adds complexity to the process.

Key Takeaways: Intercompany reconciliation is done between companies with the same parent entity. Reconciliation helps remove duplicate entries and rectify errors. This is essential for financial reporting and tax compliance. An account is considered reconciled when all the internal transactions can cancel out each other.

Not surprisingly, Fortune Business Insights reports that the global reconciliation software market is projected to grow from $1.28 What is Payment Reconciliation Software? Correct or adjust accounting records accordingly. billion in 2023 to $3.40 billion by 2030, at a CAGR of 14.9%

These regulatory agencies control the amount of taxes withheld, how benefits and garnishments are paid and record retention requirements. First, it helps you carefully track expenses associated with payroll, including gross wages, employer taxes, and benefits offered. Payroll accounting increases your chances of proper classification.

Whether it's paying invoices on time, preparing for tax season, or maintaining good relationships with suppliers, mastering accounts payable reports is crucial for maintaining financial health. Key Takeaways: Accounts payable reports help track and report business expenses.

A staff accountant primarily serves as a key financial advisor and strategist, overseeing crucial aspects of financial management and various accounting procedures. Streamlining Finance Communications : A staff accountant can handle communications for your firm, promptly addressing queries from suppliers, customers, and employees.

QuickBooks Payroll Although it works automatically with QuickBooks, QuickBooks Payroll is a QuickBooks app that brings together payroll, HR, tax compliance, and health benefits – everything you need to make it through another payroll cycle. When tax time comes, you’ll be so glad to have both of these tools in your arsenal.

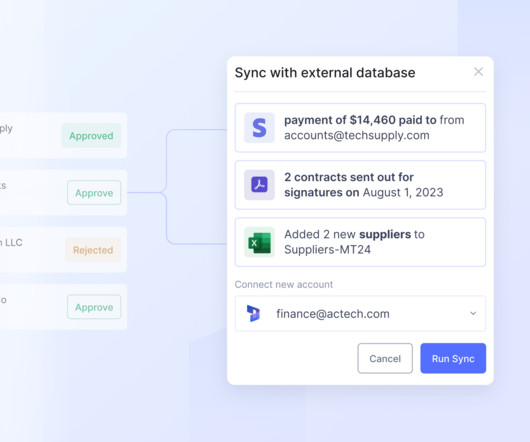

Advantage 3: In-app Reconciliation & Verification Get rid of your complex Excel macros and niche data analytics tools, and instead, use Nanonets to reconcileaccount balances, tie out final totals, and even set approval rules for certain transactions. This feature even works internationally!

This makes it difficult for them to reconcile their general ledger, chase down any errors, and can ultimately slow down the accounting cycle overall. Bill source: bill.com When invoice automation software is primarily used in the accounting industry, it’s almost guaranteed to be good.

We organize all of the trending information in your field so you don't have to. Join 52,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content