This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

What are FinancialStatements? Financialstatements are a collection of summary-level reports about an organization's financial results, financial position , and cash flows. They include the income statement, balance sheet, and statement of cash flows. Inaccurate basis for forecasts.

What are Budgeted FinancialStatements? Budgeted financialstatements contain the expected financial results, financial position , and cash flows of a business. These budgeted financials include an income statement , balance sheet , and statement of cash flows.

What are Comparative FinancialStatements? Comparative financialstatements are the complete set of financialstatements that an entity issues, revealing information for more than one reporting period.

What are Pro Forma FinancialStatements? Pro forma financialstatements are financial reports issued by an entity, using assumptions or hypothetical conditions about events that may have occurred in the past or which may occur in the future.

Related Courses How to Conduct a Compilation Engagement How to Conduct a Review Engagement How to Conduct an Audit Engagement What is a FinancialStatement Review? A review does not require the accountant to obtain an understanding of internal control , or to assess fraud risk , or other types of audit procedures.

Related Courses The Income Statement Public Company Accounting and Finance What are Interim FinancialStatements? Interim financialstatements are financialstatements that cover a period of less than one year. The interim statement concept can apply to any period, such as the last five months.

Related Courses How to Conduct a Compilation Engagement How to Conduct a Review Engagement How to Conduct an Audit Engagement What is a FinancialStatement Audit? A financialstatement audit is the examination of an entity's financialstatements and accompanying disclosures by an independent auditor.

For example, managers could have created false sales , which require that corresponding accounts receivable also be stated on the books. The CEO decides to take a "big bath" in its accounting by taking the following steps: Write off selected assets. A big bath can be employed to write off these receivables.

What are General Purpose FinancialStatements? General purpose financialstatements are those financialstatements released to a broad group of users. These statements include the following: Income statement. Who Receives General Purpose FinancialStatements?

What is an Accounting Convention? An accounting convention is a common practice used as a guideline when recording a business transaction. It is used when there is not definitive guidance in the accounting standards that govern a specific situation.

Understanding financialstatements is essential for accounting and finance team members, CEOs, business owners, creditors, and shareholders. This article provides financialstatement basics and some more advanced concepts for complex companies.

What is a FinancialStatement Compilation? A financialstatement compilation is a service to assist the management of a business in presenting its financialstatements. When completed, the accountant provides a written report that should accompany the compiled financialstatements.

What are Accounting Reports? Accounting reports are compilations of financial information that are derived from the accounting records of a business. More commonly, accounting reports are considered to be equivalent to the financialstatements. Why are Accounting Reports Important?

Related Courses How to Conduct a Compilation Engagement How to Conduct a Review Engagement How to Conduct an Audit Engagement What is Public Accounting? Public accounting refers to a business that provides accounting services to other firms. This can include the handling of many accounting functions on an outsourced basis.

What is Nonprofit Accounting? Nonprofit accounting refers to the unique system of recordation and reporting that is applied to the business transactions engaged in by a nonprofit organization. Nonprofit accounting employs the following concepts that differ from the accounting by a for-profit entity: Net assets.

Related Courses Cost Accounting Fundamentals Financial Analysis What is Cost Accounting? Cost accounting examines the cost structure of a business. None of these tools are used by financialaccountants, who are more concerned with the production of financialstatements.

Related Courses Accountants' Guidebook Bookkeeping Guidebook What is an Accounting Period? An accounting period is the span of time covered by a set of financialstatements. This period defines the time range over which business transactions are accumulated into financialstatements.

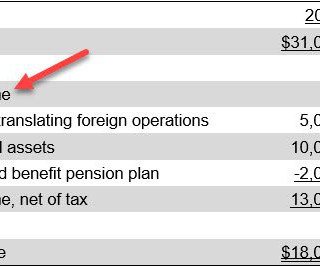

Other comprehensive income is those revenues, expenses, gains, and losses under both Generally Accepted Accounting Principles and International Financial Reporting Standards that are excluded from net income on the income statement. This means that they are instead listed after net income on the income statement.

Related Courses Accountants’ Guidebook Bookkeeper Education Bundle Bookkeeping Guidebook What is the Accounting Cycle? The accounting cycle is the actions taken to identify and record an entity's transactions. These transactions are then aggregated at the end of each reporting period into financialstatements.

The key element in the preceding definition is intent. A company could make false representations in its financialstatements simply because the accounting staff made a mistake in compiling certain financial information.

What is Accounting Practice? Accounting practice is the system of procedures and controls that an accounting department uses to create and record business transactions. Auditors rely upon consistent accounting practice when examining a company's financialstatements.

What is Tax Accounting? Tax accounting refers to the rules used to generate tax assets and liabilities in the accounting records of a business or individual. Tax accounting is derived from the Internal Revenue Code (IRC), rather than one of the accounting frameworks , such as GAAP or IFRS.

Related Courses Bookkeeper Education Bundle Bookkeeping Guidebook What is the Cash Basis of Accounting? The cash basis of accounting is the practice of recording revenue when cash has been received, and recording expenses when cash has been paid out. Audited financialstatements.

Presentation of a Business Combination When there is a business consolidation, the acquirer thereafter reports consolidated results that combine its own financialstatements with those of the acquiree.

Related Courses Bookkeeper Education Bundle Bookkeeping Guidebook What is an Accounting Transaction? An accounting transaction is a business event having a monetary impact on the financialstatements of a business. It is recorded in the accounting records of the business.

Related Courses Bookkeeper Education Bundle Bookkeeping Guidebook What is Full Cycle Accounting? Full cycle accounting refers to the complete set of activities undertaken by an accounting department to produce financialstatements for a reporting period. Here are several examples of full cycle accounting: Sales.

What is an Accounting Entry? An accounting entry is a formal record that documents a transaction. In most cases, an accounting entry is made using the double entry bookkeeping system , which requires one to make both a debit and credit entry, and which eventually leads to the creation of a complete set of financialstatements.

The accounting standards do not allow the recognition of a gain contingency prior to settlement of the underlying event. Disclosure of a Contingent Gain If a contingency may result in a gain, it is allowable to disclose the nature of the contingency in the notes accompanying the financialstatements. What is a Gain Contingency?

Related Courses Accountants’ Guidebook Bookkeeper Education Bundle Bookkeeping Guidebook What is a Ledger Account? A ledger account contains a record of business transactions. Terms Similar to Ledger Account A ledger account is also known as an account.

What is the Accrual Basis of Accounting? The accrual basis of accounting is the concept of recording revenues when earned and expenses as incurred. The accrual basis of accounting is advocated under both generally accepted accounting principles ( GAAP ) and international financial reporting standards ( IFRS ).

Related Courses Bookkeeping Guidebook Closing the Books New Controller Guidebook What are Accounting Adjustments? An accounting adjustment is a business transaction that has not yet been included in the accounting records of a business as of a specific date. Recognizing revenue that has not yet been billed.

Related Courses Accountants’ Guidebook Bookkeeping Guidebook The Balance Sheet What are Contra Accounts? A contra account offsets the balance in another, related account with which it is paired. Contra accounts appear in the financialstatements directly below their paired accounts.

Related Courses Activity-Based Costing Cost Accounting Fundamental What is an Expense Allocation? Expense allocations are required by several accounting frameworks in order to report the full cost of inventory in the financialstatements. An expense allocation occurs when indirect costs are assigned to cost objects.

Related Courses Accountants’ Guidebook Bookkeeper Education Bundle Bookkeeping Guidebook What is a Suspense Account? A suspense account is an account used to temporarily store transactions for which there is uncertainty about where they should be recorded. An entry into a suspense account may be a debit or a credit.

Related Courses Financial Analysis The Interpretation of FinancialStatements What is the Accounting Breakeven Point? The accounting breakeven point is the sales level at which a business generates exactly zero profits , given a certain amount of fixed costs that it must pay for in each period.

Accrued revenue is a cornerstone of accrual accounting, playing a vital role in accurately reflecting a company’s financial performance. This article explores the meaning, examples, and importance of accrued revenue, while comparing it with deferred revenue and accounts receivable. What is Revenue Accrual?

Related Courses Bookkeeping Guidebook How to Audit Receivables New Controller Guidebook What is the Allowance for Doubtful Accounts? The allowance for doubtful accounts is paired with and offsets accounts receivable. It represents management’s best estimate of the amount of accounts receivable that will not be paid by customers.

Related Courses Bankruptcy Tax Guide Essentials of Corporate Bankruptcy What is the Liquidation Basis of Accounting? Liquidation basis accounting is concerned with preparing the financialstatements of a business in a different way if its liquidation is considered to be imminent. Forced liquidation.

Accounting for a Guarantee A guarantee can create a liability for the guarantor that may need to be recognized , if the amount of the eventual payment can be reasonably determined and the payment is probable. Related AccountingTools Courses Accounting for Guarantees Sustainability guarantee.

Related Courses Accountants' Guidebook GAAP Guidebook What is a Subsequent Event? A subsequent event is an event that occurs after a reporting period, but before the financialstatements for that period have been issued or are available to be issued.

This is a key part of the financialstatement consolidation process, resulting in a set of financialstatements that are presented solely in the parent company’s reporting currency. Remeasure the financialstatements of the foreign entity into the reporting currency of the parent company.

Or, the transactions are designed to sidestep the reporting requirements of the applicable accounting framework , such as GAAP or IFRS. There has been a general trend in the formulation of accounting standards to allow fewer and fewer off balance sheet transactions. Related AccountingTools Course The Balance Sheet

By using a soft close, the accounting department can issue financialstatements very quickly and then return to its normal day-to-day activities. The reduced accuracy level makes the soft close impractical for reviewed or audited financialstatements that are read by outsiders.

An adverse opinion is a statement made by an entity’s outside auditor , that the entity’s financialstatements do not fairly represent its results, financial position , and cash flows. It may also result in the firing of a firm’s CFO and controller , since they are responsible for the financialstatements.

We organize all of the trending information in your field so you don't have to. Join 52,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content