This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

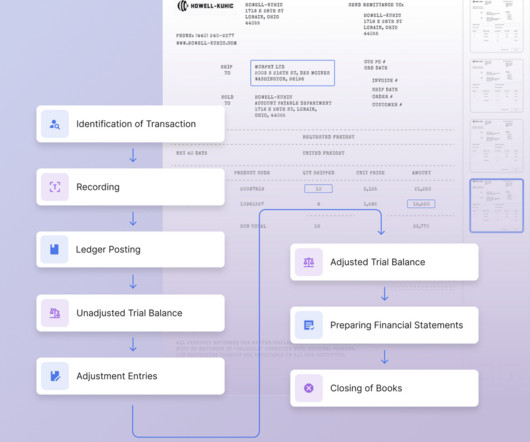

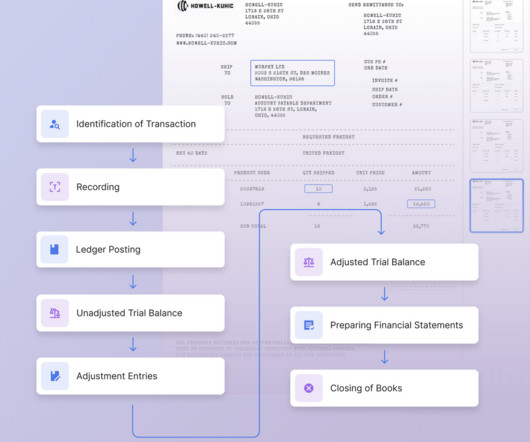

What’s the difference between bookkeeping and accounting? We’ll define each, explore the differences between bookkeeping and accounting, and discuss what it takes to pursue roles in the fields. Bookkeeping involves categorizing each transaction, specifying the amount involved, and tracking it in the relevant account.

Related Courses Bookkeeping Guidebook Corporate Cash Management How to Audit Cash Reconciling a bank statement involves comparing the bank's records of checking account activity with your own records of activity for the same account. To reconcile a bank statement, follow the steps noted below.

Multi-Channel Sales Accounting: How to Track Revenue Across Multiple Platforms Expanding your business across multiple sales channels can boost revenue, but it also brings accounting challenges. Set Up a Centralised Accounting System Using a cloud-based accounting system helps consolidate all sales data in one place.

With continuous cash flow activity, various payment channels, and expenses from all directions, using reliable accounting services for ecommerce business has become as essential as marketing and customer support activities and investment. Also Read: 6 Reasons why cloud accounting is good for your business and how it helps you grow 2.

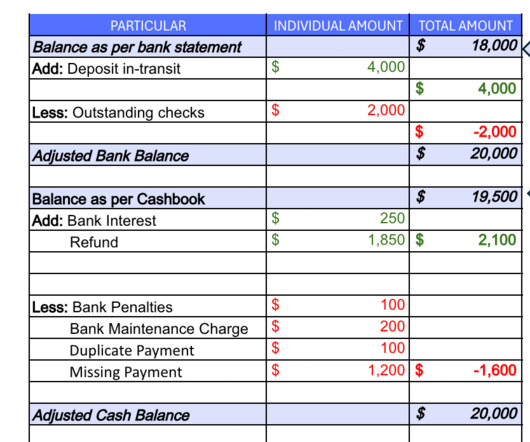

What is a Reconciling Item? A reconciling item is a difference between balances from two sources that are being compared. These items are stated in an account reconciliation , so that the balance from one source is adjusted by reconciling items to arrive at the balance from the other source. Deposits in transit.

Why is it Important to Reconcile your Bank Account? Reconciliation is a crucial accounting process that ensures the accuracy of the financial close process. It ensures that the money credited or debited in your bank account matches the money being expended or made. How Often Should You Reconcile Your Bank Statements?

Related Courses Bank Reconciliation Essentials Bookkeeping Guidebook How to Audit Cash What is an Outstanding Deposit? An outstanding deposit is that amount of cash recorded by the receiving entity, but which has not yet been recorded by its bank. The bank will record the receipt in the company's account the following Monday, April 3.

Our B2B Payment Security study with the Institute of Finance & Management (IOFM), found that checks account for the largest share of financial loss due to fraud, ranging from less than $50,000 to more than $1 million. Cost-Savings According to Mastercard , ePayments via v irtual cards can drive cost savings of $0.50

What is a Deposit in Transit? A deposit in transit is cash and checks that have been received and recorded by an entity, but which have not yet been recorded in the records of the bank where the funds are deposited. Why Does a Deposit in Transit Occur? When is There No Deposit in Transit?

Creating 1099 reporting is one task that can take less time with accounts payable (AP) automation. Simplified Reconciliation Automated systems can provide timely reporting and visibility into supplier payments, making it easier to reconcileaccounts during tax season. Tax season is a busy time for finance departments.

A bank reconciliation is the process of matching the balances in an entity's accounting records for a cash account to the corresponding information on a bank statement. The goal of this process is to ascertain the differences between the two, and to book changes to the accounting records as appropriate.

If you were to ignore these differences, there would eventually be substantial variances between the amount of cash that you think you have and the amount the bank says you actually have in an account. The result could be an overdrawn bank account, bounced checks , and overdraft fees. Account shut down. Demanded by auditors.

However, let's understand the manual bank reconciliation process once: Step 1: Gather documents On the bank side, you need the bank statements, outstanding checks, deposits, and any pending transactions. Match the deposits in the two statements. They have to be adjusted as shown in the next steps.

Related Courses Bookkeeping Guidebook Corporate Cash Management How to Audit Cash Optimal Accounting for Cash What is a Proof of Cash? A proof of cash is essentially a roll forward of each line item in a bank reconciliation from one accounting period to the next, incorporating separate columns for cash receipts and cash disbursements.

Accounting gets left behind while business moves forward. Open up your accounting software and assess what might be missing from there. Your chart of accounts is a list of the types of categories or accounts that you use to classify each transaction. As a small business, you want to avoid having too many accounts.

What is a Bank Reconciliation Statement Bank reconciliation is the process that ensures that a company's recorded cash balances align with the funds in their bank accounts. It typically outlines outstanding checks, deposits in transit, bank fees, errors, and any other differences between the two sets of records.

However, let's understand the manual bank reconciliation process once: Step 1: Gather documents On the bank side, you need the bank statements, outstanding checks, deposits, and any pending transactions. Match the deposits in the two statements. They have to be adjusted as shown in the next steps.

Seven Best Practices for Effective Account Reconciliations From Mesopotamia's rudimentary ledgers tracking livestock and crops to the second-century BCE Indian treatise " Arthashastra ", accounting has been a cornerstone of economic management in any civilized society.

Introduction to Account Reconciliation Account reconciliation is the critical process of comparing your general ledger with internal and external sources. Account Reconciliation can be a fairly manual task, especially right before the monthly close. Why is Account Reconciliation so Important?

Balance sheet reconciliation resolves any discrepancies in the financial statements with external documentation so that companies adhere to accounting standards and reflect their actual financial position. Finance teams can also follow specific templates designed to reconcile their balance sheets manually.

Bank Reconciliation Vs. Book Reconciliation In accounting and financial management, we encounter the terms "Book Reconciliation" and " Bank Reconciliation " These terms are often used interchangeably, leading to ambiguity regarding their meanings. What Is Book Reconciliation?

Introduction to Bank Reconciliation Journal Entries Bank reconciliation is an important process in accounting that ensures the accuracy and integrity of a company's financial records. Integrate Nanonets Reconcile financial statements in minutes Try for Free What is Journal Entry in accounting?

Accounting firms relying on memory alone to keep up with their clients’ accounting tasks risk overlooking essential work assignments or missing critical deadlines. Plus, we review a few daily, weekly, monthly, quarterly, and annual accounting tasks successful firm owners keep tabs on to prevent their teams from getting overwhelmed.

Month-end close is a widely accepted accounting standard that is aimed at keeping an accurate set of financial records and detecting errors/fraud. It involves recording, reviewing, and reconciling records at the end of every month. How to do monthly account reconciliation? Here is how you can do monthly reconciliation.

The bank reconciliation process involves comparing the internal and bank records for a bank account , and adjusting the internal records as necessary to bring the two into alignment. The bank reconciliation process is usually accomplished with the bank reconciliation module in an accounting software package. Check printing fees.

Importance of bank reconciliation in internal control In the world of finance and accounting, accuracy is key. This article highlights the importance of bank reconciliation, and its role in maintaining financial control, accountability, and protection against errors and fraud. What Is a Bank Reconciliation?

Learning to reconcile with QuickBooks Online is a starting step for using QuickBooks to manage books. QuickBooks is a handy tool to help you reconcile your accounts without using any external tools. Step 1: Go to the reconciliation menu Search for “Reconcile” in the top help menu bar.

Account reconciliation is a critical process in accounting, which ensures that financial records are accurate and consistent. This article will provide an in-depth understanding of account reconciliation, its benefits, and how businesses can leverage technology to automate the process. What is Account Reconciliation?

I recommend starting out with all invoices, customer payments, and deposits. Tip #2: Reconcile business bank and credit card accounts. Symptom #1: Whenever they go into bank deposits , they see that they have a lot of old unclear transactions in undeposited funds. Step #4: Match the deposit transaction in the bank feed.

Our free Bank reconciliation template provides a simple way to reconcile your cashbook with your bank statement. Download them in CSV format and paste them into individual Excel sheets.Also, find all the outstanding checks, deposits, and any pending transactions. Reconciling 100s of transactions can take days to resolve completely.

Merchant accounts are an important tool for businesses today. In a world where cash and check payments are steadily declining, these accounts enable businesses to accept card-based transactions. Read on to learn more about how using a merchant account to accept virtual card payments can benefit your business.

By maintaining your books regularly, reviewing reports, and reconciling your accounts at the end of each month, you can avoid bookkeeping disasters. Additionally, you should check your bank account to ensure all deposits have cleared the bank. Accounting & Bookkeeping Services by Superior Virtual Bookkeeping LLC

Customer: Lena Doron, Doron Contracting Industry: Construction Lena Doron co-owns Doron Contracting with her husband, Guy Doron, overseeing the administrative work for the business, including accounts and receivables. AvidXchange’s supplier portal helps Doron Contracting save time and more easily reconcile invoices. And what day?’”

By choosing an enhanced direct deposit option , Leading Edge Construction Services Inc. We receive big physical checks and not only do they arrive late, we have to then take them to the bank to deposit and wait even longer for the 3-5 day hold to lift to finally have access to the funds.”

They are needed to ensure that checks are recorded correctly, deposited promptly, and not stolen or altered anywhere in the process. Also, stamp “ for deposit only ” and the company’s bank account number on every check received; this makes it more difficult for someone to extract a check and deposit it into some other bank account.

QuickBooks is one of the most widely used apps for bookkeeping, and it offers a convenient way to reconcile credit cards without needing external tools. Step 1: Go to the reconciliation menu In the top help menu bar, search for 'Reconcile.' ' Then, select the account you wish to reconcile.

A bank reconciliation statement is a financial document that compares a company's bank account balance to the transactions recorded on its general ledger, often called the "cash books." They ensure the financial accuracy of the statements and are an essential process for the accounting teams involved in cash flow management.

In the world of finance and accounting, the process of reconciliation plays a vital role in ensuring accurate and transparent financial records. The aim is to reconcile the data and ensure that transactions match supporting documents across different sources. What are the steps in the Process of Reconciliation?

A bank balance is the ending cash balance appearing on the bank statement for a bank account. The bank balance can also be derived at any time when an inquiry is made regarding the bank's record of the cash balance in an account. A book balance is the account balance in a company's accounting records. Deposits in transit.

Looking for the best accounting practice management software for your firm? Good news, because this is the ULTIMATE accounting practice management software round-up post. Get to know the top accounting practice management software and why it is essential for your business. The Basics of Accounting Practice Management Software.

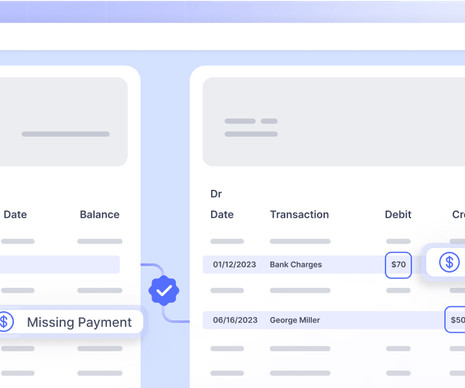

Whether it's ensuring that expenses align with available funds or guaranteeing that business transactions accurately reflect the company's financial standing, tracking checks outstanding and reconciling bank statements is non-negotiable. Outstanding checks are vulnerable to fraudulent activities.

But as businesses grow and cash flow increases, its harder for accounting teams to keep up. As a matter of fact, by reconciling payments regularly, businesses can quickly detect discrepancies, such as missed or duplicate payments, incorrect amounts or unauthorized transactions. Manual spreadsheets can lead to errors.

The bank balance is the balance reported by the bank on a firm’s bank account at the end of the month. The book balance is the in-house general ledger record of the same account. Deposits in transit. What is the Bank Balance? What is the Book Balance? Unrecorded fees.

AvidXchange provides accounts payable (AP) automation Software as a Service (SaaS) to mid-size companies. Once invoices are approved, AvidPay will automatically send payment to a business’ suppliers via their preferred payment method (credit card, direct deposit or mailed check). What Is AvidXchange?

We organize all of the trending information in your field so you don't have to. Join 52,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content