This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

What’s the difference between bookkeeping and accounting? We’ll define each, explore the differences between bookkeeping and accounting, and discuss what it takes to pursue roles in the fields. Bookkeeping involves categorizing each transaction, specifying the amount involved, and tracking it in the relevant account.

Skilled in all aspects of bookkeeping, including accounts payable/receivable, bank reconciliations, payroll processing, and financial reporting. Processed accounts payable and receivable, ensuring timely payments and collections. Reconciled bank statements monthly, maintaining accurate financialrecords.

As tax season approaches, many small business owners find themselves scrambling to organize their financialrecords and ensure they comply with the intricate web of tax regulations. The IRS requires businesses to keep detailed records of all financial transactions. Get Caught Up Overwhelming by bookkeeping backlog?

In the background, what actually keeps profitable online stores up and running is wise financial management. That’s why investing in optimized accounting services for ecommerce stores isn’t merely a good idea, it’s crucial. These tools simplify daily financial responsibilities and integrate your online sales platform.

Accounts receivable fraud is becoming an increasingly pressing threat for businesses of all sizes, especially companies that grow or make a lot of changes. What makes Accounts Receivable Professionals and Operations Especially Vulnerable to Fraud? So it is important to encourage a culture of vigilance and accountability.

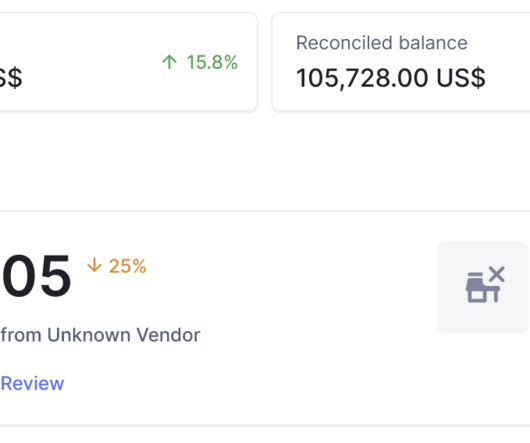

Why is it Important to Reconcile your Bank Account? Reconciliation is a crucial accounting process that ensures the accuracy of the financial close process. It ensures that the money credited or debited in your bank account matches the money being expended or made. How do you reconcile your bank statement?

Accounts receivable reconciliation is a crucial process within accounting and financial management practices undertaken regularly by a business. As transactions with customers and clients occur, businesses generate accounts receivable, which represent amounts owed to them for goods and services sold or rendered.

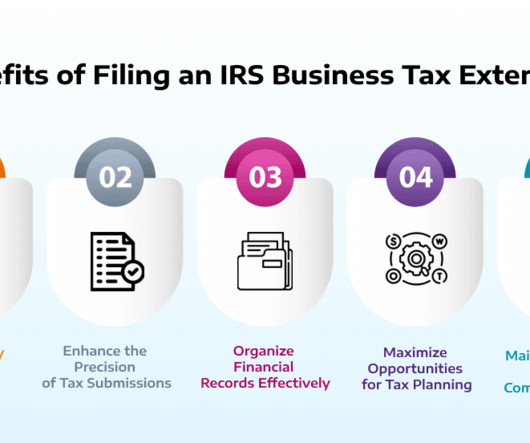

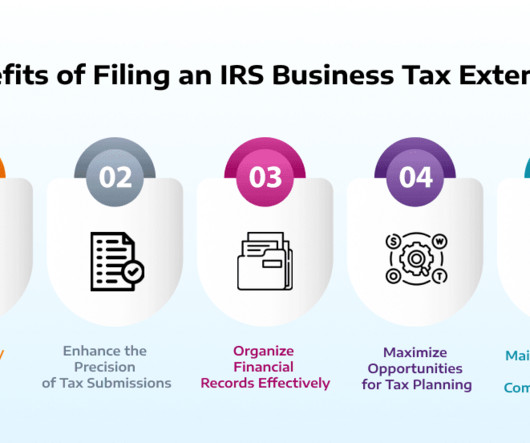

While its not an extension to pay taxes owed, it grants businesses the flexibility to organize their financialrecords. This extension offers invaluable support for companies managing complex financials or experiencing delays in gathering necessary documents. Alternatively, they could incur penalties and interest.

While its not an extension to pay taxes owed, it grants businesses the flexibility to organize their financialrecords. This extension offers invaluable support for companies managing complex financials or experiencing delays in gathering necessary documents. Alternatively, they could incur penalties and interest.

Accounting gets left behind while business moves forward. Take a look at this bookkeeping cleanup checklist to get all your financial ducks in a row. You are looking to gather all of your bank statements, receipts, invoice, and other related financial information. What records need to be brought up to date?

By evolving your bookkeeping process, you can be more confident that your financialrecords are accurate and up-to-date. As the business grows, it may become more challenging to keep track of all the financial transactions manually. You will be able to reconcileaccounts faster and more accurately.

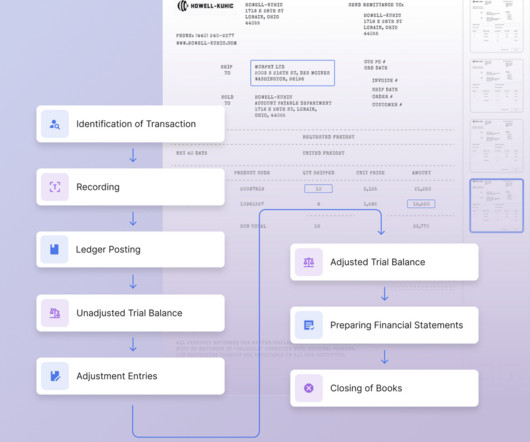

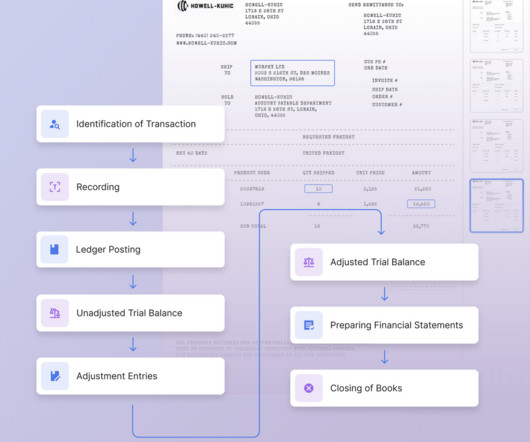

The end of month close process plays a vital role in ensuring the accuracy, integrity, and transparency of financialrecords for businesses of all sizes. Its primary purpose is to ensure the accuracy and completeness of financialrecords so that financial statements can be prepared for internal and external reporting purposes.

Picture this: a team of expert bookkeepers diligently managing your financialrecords and transactions without setting foot in your office. Traditional bookkeepers are professionals responsible for recordingfinancial transactions, maintaining ledgers, and preparing financial statements manually or using basic accounting software.

Seven Best Practices for Effective Account Reconciliations From Mesopotamia's rudimentary ledgers tracking livestock and crops to the second-century BCE Indian treatise " Arthashastra ", accounting has been a cornerstone of economic management in any civilized society.

How SMEs in Singapore Can Use ChatGPT for Everyday Work Tasks Managing an SME in Singapore involves juggling a multitude of tasks, from keeping track of financials to ensuring regulatory compliance. Whether youre handling accounting services , managing your team, or overseeing operations, time is always of the essence.

A Guide to NetSuite Account Reconciliation Accurate financialrecords are an important part of any business’ ability to make informed decisions and also adhere to legal regulations. What Is Account Reconciliation?

Introduction to Account Reconciliation Account reconciliation is the critical process of comparing your general ledger with internal and external sources. Account Reconciliation can be a fairly manual task, especially right before the monthly close. Why is Account Reconciliation so Important?

The Importance of Accounts Reconciliation Companies handle a variety of finance-related documents, ranging from bank statements to invoices and payroll records. Amidst this deluge of numbers and figures lies a crucial task: account reconciliation.

On the company side, you require the company's cashbook, which records both incoming and outgoing transactions. Step 2: Match deposits Following double-entry accounting, a debit in the bank statement is recorded as a credit in the cashbook, and vice versa. Why is it important to reconcile your bank statements?

In this digital world, QuickBooks is a comprehensive bookkeeping and accounting software that is helping numerous businesses to smoothly record their finances. QuickBooks accounting software is highly popular and loaded with numerous features – from bank integration to bookkeeping services.

Consider using accounting software or apps to streamline this process. Maintain separate bank accounts, credit cards, and accountingrecords for your business to avoid confusion and streamline the tax filing process. Ensure that all income and expenses are properly recorded, and resolve any discrepancies or errors.

Guide to the Vendor Account Reconciliation Process Running a business involves collaboration with various vendors who provide different kinds of products and services. What is Vendor Reconciliation In accounts payable (AP) activities, a vendor is an individual or entity that provides goods or services to the company.

What is a Bank Reconciliation Statement Bank reconciliation is the process that ensures that a company's recorded cash balances align with the funds in their bank accounts. In effect, the reconciliation statement is a document that presents the comparison between the internal financialrecords of a company (e.g.

Managing payments and transaction records for your business seems easy enough, right? But as businesses grow and cash flow increases, its harder for accounting teams to keep up. Accurate financialrecords are essential for businesses to meet auditing requirements and avoid potential fines or penalties for non-compliance.

Below are some of the main benefits of implementing this automation into your workflow: Time Efficient Bookkeeping Manually logging into various banking platforms, downloading bank statements, and reconciling the transactions one by one, can quickly become very time-consuming. Bookkeepers are no strangers to this concept.

Introduction If you've ever wondered how businesses keep track of their spending or ensure that every dollar is accounted for, you’re in the right place. Expense reconciliation is a process within finance and accounting that ensures that a company's financialrecords accurately reflect its spending activities.

To avoid this, open a separate business bank account and use it exclusively for business-related expenses. Not Keeping Proper Records: Poor record-keeping can quickly spiral into a bookkeeping nightmare. Invest in accounting software or hire a professional bookkeeper to maintain organized and up-to-date records.

Bank Reconciliation Vs. Book Reconciliation In accounting and financial management, we encounter the terms "Book Reconciliation" and " Bank Reconciliation " These terms are often used interchangeably, leading to ambiguity regarding their meanings. These records may be internal financialrecords or external.

While providing a tremendous opportunity for business expansion, third-party delivery services also contribute an additional nuanced layer of accounting complexity. Accurate financial reporting is essential for business and food tax purposes. The ramifications can be severe without proper accounting reconciliation.

Accounts payable software for small business can significantly enhance financial workflow and improve overall efficiency. This powerful tool automates and streamlines the accounts payable processes, helping businesses manage invoices, vendor payments, and maintain accurate financialrecords.

Introduction to Bank Reconciliation Journal Entries Bank reconciliation is an important process in accounting that ensures the accuracy and integrity of a company's financialrecords. It involves the comparison between the company’s internal financialrecords and those of the bank.

This is where the significance of having an expert ally, like Less Accounting, becomes invaluable. The Critical Role of Clean FinancialRecords At the heart of every successful business is the ability to make informed decisions. Tax filings, for example, require precise financial information. We can help!

There seem to be so many ways to mess up your financialrecords without knowing it. Once your receipt is in the platform, you can use our advanced OCR feature to automatically extract data from your receipt and post it directly to your accounting software. Bookkeeping is not for the faint of heart.

Account reconciliation is a critical process in accounting, which ensures that financialrecords are accurate and consistent. This article will provide an in-depth understanding of account reconciliation, its benefits, and how businesses can leverage technology to automate the process. How to ReconcileAccounts?

In the world of finance and accounting, the process of reconciliation plays a vital role in ensuring accurate and transparent financialrecords. It is a crucial process for businesses to identify discrepancies, resolve errors, and maintain the integrity of their financial statements.

Introduction Diving into the world of accounting, reconcilingaccounts becomes a routine yet crucial task, especially when bank or credit card statements roll in. However, the dynamic nature of business means changes or oversights can occur, necessitating a revisit to previously reconciledaccounts.

Efficient reconciliation of payments is a vital aspect of financial management for businesses of all sizes. As transactions flow in and out, reconciling payments becomes crucial to ensure accuracy, identify discrepancies, and maintain a clear financial picture. Why is payment reconciliation crucial for businesses?

Maintaining accurate financialrecords is vital for any business, and the general ledger, as the central repository of financial transactions, plays a critical role in this process. It includes various accounts that track assets, liabilities, equity, revenue, and expenses.

We will cover everything you need to know , from tracking expenses and invoices to reconciling bank statements and choosing the right bookkeeping software. Establishing a record-keeping system for tracking income and expenses is essential. To reconcile your bank statements, you’ll need to take a few simple steps.

There seem to be so many ways to mess up your financialrecords without knowing it. Once your receipt is in the platform, you can use our advanced OCR feature to automatically extract data from your receipt and post it directly to your accounting software. Bookkeeping is not for the faint of heart.

Importance of bank reconciliation in internal control In the world of finance and accounting, accuracy is key. Whether you're managing personal finances or running a business, keeping precise records is crucial for financial health. What Is a Bank Reconciliation? Why are Bank Reconciliations Important?

On the company side, you require the company's cashbook, which records both incoming and outgoing transactions. Step 2: Match deposits Following double-entry accounting, a debit in the bank statement is recorded as a credit in the cashbook, and vice versa. Why is it important to reconcile your bank statements?

Running a successful landscaping business is all about precision—whether it’s in design, operations, or even accounting. However, while you can control many aspects of your business, bookkeeping and accounting can be particularly challenging. “But believe us, mixing them creates even bigger headaches in the long run.

An accounts receivable balance refers to a company’s outstanding invoices that customers have not yet settled. Accountantsrecord this uncollected income as a normal debit balance or asset. So, how can it lead to a negative accounts receivable balance? So, how can it lead to a negative accounts receivable balance?

We organize all of the trending information in your field so you don't have to. Join 52,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content