This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

GeneralLedger Reconciliation The GeneralLedger (GL) is a silent custodian of a company's financial narrative. It is a record of all financial transactions of an enterprise and provides a comprehensive account of the organization's monetary activities. What is the GeneralLedger?

They are used to change the ending balances in the generalledger accounts when accrual basis accounting is used. Related Courses Bookkeeper Education Bundle Bookkeeping Guidebook What are the Debit and Credit Rules? Debits and credits are the opposing sides of an accounting journal entry.

A journal entry is usually recorded in the generalledger ; alternatively, it may be recorded in a subsidiary ledger that is then summarized and rolled forward into the generalledger. The generalledger is then used to create financial statements for the business.

The intent of adding these entries is to correct errors in the initial version of the trial balance and to bring the entity's financial statements into compliance with an accounting framework , such as Generally Accepted Accounting Principles or International FinancialReporting Standards.

Accounting entries are also needed by an organization’s auditors; they cannot conduct an audit without having a complete set of financial records, and those records are created with accounting entries. In short, it is impossible for a business to create financialreports or have them audited unless they use accounting entries.

Suppliers may also require audited financial statements before they will be willing to extend trade credit (though usually only when the amount of requested credit is substantial). Observe assets, review purchase and disposal authorizations, review lease documents, examine appraisal reports, recalculate depreciation and amortization.

Account reconciliation is the process of comparing generalledger accounts (usually from the balance sheet) with supporting documents, such as bank statements, sub-ledgers, and other underlying transaction details. Reconciliation in accounting is essential for ensuring that the generalledger balance is complete and accurate.

The essential steps of the accounting cycle include analyzing and recording transactions, posting to the generalledger, preparing a trial balance, making adjusting entries, preparing financial statements, making closing entries, and sometimes making reversing entries.

Review and Adjust Financial Statements At the annual close, you need to thoroughly review the financial statements prepared by your bookkeeping team against the client’s generalledger accounts. What to put on your checklist for this task: Compare financial statements with the generalledger.

Transparency and Trust: Enhances stakeholder confidence through clear, reliable financialreporting. Regulatory Compliance and Accuracy Adherence to financial regulations is non-negotiable, and the R2R process ensures organizations stay compliant while maintaining the accuracy of their financialreports.

Use automated workflows to manage the accounts payable process (including sending payments automatically and generatingfinancialreports). Enter the Invoice in the GeneralLedger: Once the invoice is approved, it is entered as a credit in the generalledger’s accounts payable account and classified as an ‘open invoice’.

Discrepancies in your financialreports could lead to inaccurate data for future decisions, a mistake that could quickly spell disaster for any business. It also allows you to confirm that all payroll entries, including accruals, are posted to the accurate ledgers. The two must have the same closing balances.

Roll forward fixed assets: prepaid, expense accruals, etc. Review standard/recurring journal entries for completeness Run the critical financialreports, particularly the trial balance and generalledger to give them the “eye test.” Perform reconciliations: bank, credit card, inventory, etc.

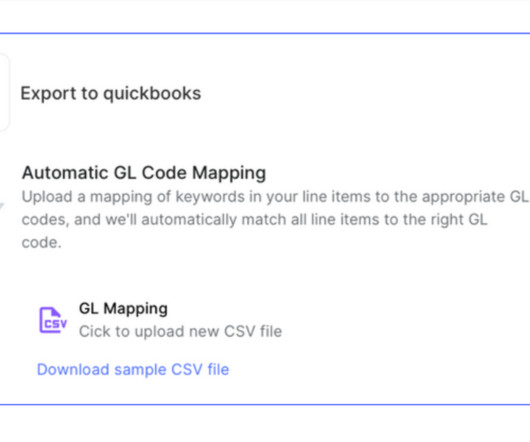

Artificial intelligence is used to learn from past experience and suggest specific generalledger (GL) codes or approval routing paths. Coding Invoices AP automation helps a company establish rules that will choose the correct generalledger (GL) code for each invoice.

We organize all of the trending information in your field so you don't have to. Join 52,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content