This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Related Courses Accountants’ Guidebook Bookkeeper Education Bundle Bookkeeping Guidebook The generalledger is the master set of accounts that aggregates all transactions recorded for a business. Verify that the ending detail for the account matches the ending account balance.

What is a GeneralLedger? A generalledger is the master set of accounts that summarize all transactions occurring within an entity. The generalledger is comprised of all the individual accounts needed to record the assets , liabilities , equity , revenue , expense , gain , and loss transactions of a business.

Related Courses Closing the Books The Soft Close The Year-End Close How to Prepare FinancialStatements The preparation of financialstatements involves the process of aggregating accounting information into a standardized set of financials. Based on this information, write footnotes to accompany the statements.

Related Courses How to Conduct a Compilation Engagement How to Conduct a Review Engagement How to Conduct an Audit Engagement What is a FinancialStatement Audit? A financialstatement audit is the examination of an entity's financialstatements and accompanying disclosures by an independent auditor.

Related Courses Bookkeeper Education Bundle Bookkeeping Guidebook What is a GeneralLedger? A generalledger is the master set of accounts that summarize all transactions occurring within an entity. There may be a subsidiary set of ledgers that summarize into the generalledger.

Related Courses Accountants’ Guidebook Bookkeeper Education Bundle Bookkeeping Guidebook The generalledger clerk position is accountable for creating journal entries and assembling supporting documentation, as well as for tracking the contents of accounts , creating portions of the financialstatements , and writing related disclosures.

Posting in accounting is when the balances in subledgers and the general journal are shifted into the generalledger. Posting only transfers the total balance in a subledger into the generalledger, not the individual transactions in the subledger. What is the GeneralLedger?

Related Courses Accountants’ Guidebook Bookkeeper Education Bundle Bookkeeping Guidebook What is the GeneralLedger? A generalledger is the master set of accounts that summarize all transactions occurring within an entity.

Maintaining accurate financial records is vital for any business, and the generalledger, as the central repository of financial transactions, plays a critical role in this process. Ensuring the accuracy and integrity of the generalledger requires regular reconciliation.

Related Courses Bookkeeping Guidebook How to Audit Receivables New Controller Guidebook The reconciliation of accounts receivable is the process of matching the detailed amounts of unpaid customer billings to the accounts receivable total stated in the generalledger. The two information sources for this reconciliation are noted below.

The fixed asset accountant , generalledger clerk , and tax accountant are most likely to be involved in the use of journal entries. There may be a number of closing entries at the end of each reporting period that the generalledger clerk is tasked with entering into the accounting system.

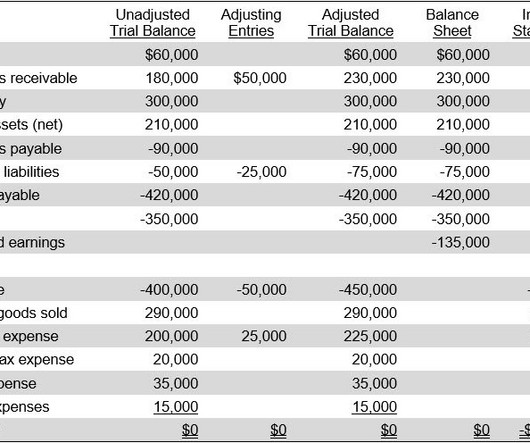

A trial balance is an accounting report that states the ending balance in each generalledger account. The purpose of a trial balance is to ensure that all entries made into an organization's generalledger are properly balanced. A trial balance lists the ending balance in each generalledger account.

Related Courses Bookkeeper Education Bundle Bookkeeping Guidebook Closing the Books Posting in accounting is when the balances in subledgers and the general journal are shifted into the generalledger. Instead, all information is directly stored in the accounts listed in the generalledger.

A subsidiary ledger stores the details for a generalledger control account. Once information has been recorded in a subsidiary ledger, it is periodically summarized and posted to a control account in the generalledger , which in turn is used to construct the financialstatements of a company.

The unadjusted trial balance is the listing of generalledger account balances at the end of a reporting period, before any adjusting entries are made to the balances to create financialstatements. Related Courses Bookkeeping Guidebook Closing the Books The Year-End Close What is an Unadjusted Trial Balance?

A transaction is a business event that has a monetary impact on an entity's financialstatements , and is recorded as an entry in its accounting records. A high-volume transaction, such as a billing to a customer, may be recorded in a specialized journal , which is then summarized and posted to the generalledger.

Related Courses Accountants’ Guidebook Bookkeeper Education Bundle Bookkeeping Guidebook What are the Basics of Financial Accounting? This article gives an overview of financial accounting basics for the non-accountant. Its orientation is toward recording financial information about a business.

Related Courses The Balance Sheet The Interpretation of FinancialStatements What is the Statement of Changes in Equity? The statement of changes in equity is a reconciliation of the beginning and ending balances in a company’s equity during a reporting period.

The intent of adding these entries is to correct errors in the initial version of the trial balance and to bring the entity's financialstatements into compliance with an accounting framework , such as Generally Accepted Accounting Principles or International Financial Reporting Standards.

The information in the ledger is the highest level of information aggregation, from which trial balances and financialstatements are produced. Thus, information can be rolled up from journals to ledgers to produce financialstatements, and rolled back down to investigate individual transactions.

Related Courses Accountants’ Guidebook Bookkeeper Education Bundle Bookkeeping Guidebook What is a Ledger Account? A ledger account contains a record of business transactions. It is a separate record within the generalledger that is assigned to a specific asset, liability, equity item, revenue type, or expense type.

A journal entry is usually recorded in the generalledger ; alternatively, it may be recorded in a subsidiary ledger that is then summarized and rolled forward into the generalledger. The generalledger is then used to create financialstatements for the business.

The accounting records are aggregated into the generalledger , or the journal entries may be recorded in a variety of sub-ledgers , which are later rolled up into the generalledger. This information is then used to construct financialstatements as of the end of a reporting period.

Thus, there is likely to be an outstanding account payable balance in the ledger at any time. If the purchasing volume is relatively low, then there is no need for a purchase ledger. Instead, this information is recorded directly within the generalledger.

The concept is primarily used in regard to the audit of a company's financialstatements , where the auditors rely upon a variety of assertions regarding the business. The assertion is that all transactions have been recorded within the correct accounts in the generalledger. Classification. Completeness.

Year-end adjustments are journal entries made to various generalledger accounts at the end of the fiscal year , to create a set of books that is in compliance with the applicable accounting framework. It is especially necessary to create year-end adjustments when the financialstatements are to be audited by the company’s auditors.

These transactions are then aggregated at the end of each reporting period into financialstatements. The cycle is also needed to produce financialstatements. In addition, most businesses use accounting software to accumulate transactional data and convert them into financialstatements.

Related Courses Accountants' Guidebook Bookkeeping Guidebook New Controller Guidebook An accountant is a person who records business transactions on behalf of an organization, reports on company performance to management, and issues financialstatements. Management reports are issued to the management team.

Maintains a chart of accounts and generalledger , from which are compiled a set of financialstatements. Assists both internal and external auditors with their examinations of the company's financial reports and controls.

An extended trial balance is a standard trial balance to which are added columns extending to the right, and in which are listed the following categories: Initial balances per generalledger. These are the account totals as of the end of the accounting period , as compiled from the generalledger.

Related Courses Closing the Books The Balance Sheet The Year-End Close The balance sheet is one of the three reports within the financialstatements. If you are operating a manual system, then construct the trial balance by transferring the ending balance in every generalledger account to a spreadsheet.

This information is then aggregated into financialstatements. The third group is the period-end processing required to close the books and produce financialstatements. Prepare FinancialStatements Create the financialstatements from the adjusted trial balance. The steps are noted below.

The total of the transactions in the subledger roll up into the generalledger. A summary-level entry is periodically recorded in the generalledger. A generalledger contains the master set of accounts for an organization, in which all transactions are recorded (other than those recorded in subledgers).

In most cases, an accounting entry is made using the double entry bookkeeping system , which requires one to make both a debit and credit entry, and which eventually leads to the creation of a complete set of financialstatements. An accounting entry is needed to establish an accurate record of every business transaction.

Auditors want to see an account reconciliation for larger accounts, though reconciliations should be performed even in the absence of an auditor request, since this is a good accounting practice that leads to more accurate financialstatements.

An income statement is one of the three components of a complete set of financialstatements , where the other two reports are the balance sheet and statement of cash flows. The following steps will show you how to prepare an income statement.

In concept, it is an unadjusted trial balance , to which is added any adjusting entries needed to close a reporting period (such as for the monthly, quarterly, or annual financialstatements ). These additional entries are then entered in the generalledger , resulting in a completed trial balance.

The trial balance is an accounting report that lists the ending balance in each generalledger account. The first step in the process of creating financialstatements is to prepare a trial balance. This is done in order to aggregate accounting information for inclusion in the financialstatements.

Contra accounts appear in the financialstatements directly below their paired accounts. Related Articles Account Analysis Accounting Adjustments Books of Original Entry GeneralLedger Accounts How to Write an Accounting Journal Entry The Difference Between Nominal Accounts and Real Accounts

The information in these books is then summarized and posted into a generalledger , from which financialstatements are produced. Examples of these accounting journals are the cash journal, general journal , purchase journal, and sales journal.

A control account is a summary-level account in the generalledger. This account contains aggregated totals for transactions that are individually stored in subsidiary-level ledger accounts. The ending balance in a control account should match the ending total for the related subsidiary ledger.

Balance sheet reconciliation is a critical process in finance and accounting that ensures the accuracy and integrity of financialstatements. Balance sheet reconciliation is an essential accounting practice that verifies the accuracy and consistency of financialstatements.

It is a crucial process for businesses to identify discrepancies, resolve errors, and maintain the integrity of their financialstatements. In this article, we will explore the process of reconciliation and discuss the steps. Manual reconciliation can be time-consuming, prone to errors, and inefficient.

A lead schedule is a working paper that lists the detailed generalledger accounts comprising a line item in the financialstatements. The total on a lead schedule should match the total for the corresponding line item in a client’s financialstatements.

We organize all of the trending information in your field so you don't have to. Join 52,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content