This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Bookkeepers ensure these buckets are properly categorized and meticulously record every deposit and withdrawal. This ongoing process provides a clear picture of a company’s financial health at any given time. Accountants can specialize in various areas, such as tax, auditing, forensic accounting, or financial management.

Having separate business accounts enables your ecommerce accounting services to accurately keep track of revenues, expenses, and profits, therefore making it easy to prepare for taxes and maintain your general well-being financially. Moreover, when audited, well-organized records prove to be lifesavers.

A Bank Reconciliation Statement is a financial document that ensures that the cash balances recorded in the internal financialrecords align with the financialrecords presented in the bank statement. General Ledger ) and the bank’s records (e.g. Bank Statement ). Bank Statement ).

Introduction to Bank Reconciliation Journal Entries Bank reconciliation is an important process in accounting that ensures the accuracy and integrity of a company's financialrecords. It involves the comparison between the company’s internal financialrecords and those of the bank.

If a customer calls you and asks about their payment, can you see the date it was received and deposited? If not, it may be time to rework your current accounting policies to implement audit trails. Despite what many business owners believe, audit trails aren’t reserved only for companies that receive an audit.

This article highlights the importance of bank reconciliation, and its role in maintaining financial control, accountability, and protection against errors and fraud. Bank reconciliation involves comparing a company's internal financialrecords with those provided by the bank. What Is a Bank Reconciliation?

Whether it's ensuring that expenses align with available funds or guaranteeing that business transactions accurately reflect the company's financial standing, tracking checks outstanding and reconciling bank statements is non-negotiable. Looking out for a Reconciliation Software?

This prevents unauthorized individuals from accessing sensitive financial data. Regular Audits and Updates: A reputable expense management tool conducts regular security audits and updates to identify vulnerabilities and patch them promptly. How often should financialaudits be conducted?

Accurate financialrecords are essential for businesses to meet auditing requirements and avoid potential fines or penalties for non-compliance. By having a systematic process in place for reconciling payments, business users can ensure that all transactions are recorded properly and that financial reports are reliable.

In the world of finance and accounting, the process of reconciliation plays a vital role in ensuring accurate and transparent financialrecords. It is a crucial process for businesses to identify discrepancies, resolve errors, and maintain the integrity of their financial statements. What is Reconciliation?

Maintaining accurate financialrecords is vital for any business, and the general ledger, as the central repository of financial transactions, plays a critical role in this process. This documentation serves as a reference for future audits, reviews, and internal control purposes.

Step #3 Identify items that have hit the company records but are missed on the bank statement. Cash that has been received and recorded by the company but has not yet been recorded on the bank statement is called " deposits in transit." These need to be adjusted in the company's records.

As transactions flow through various channels, the risk of human oversight increases, leading to inaccuracies in recording payment details. This dilemma of mistakes can result in misaligned financialrecords, delayed reconciliations, and a potential domino effect on downstream financial processes.

Expense reconciliation is a process within finance and accounting that ensures that a company's financialrecords accurately reflect its spending activities. At its core, it involves comparing financial data from various sources within a business to identify any discrepancies or errors and bring them into alignment.

Recording purchase invoices as soon as they are received and verified helps detect potential fraud related to duplicate payments, fictitious vendors, or inflated expenses. Prompt depositing and recording cash receipts minimizes the risk of theft or misappropriation. To list just a few: Accounts receivable reconciliation.

Need for Account Reconciliation Account Reconciliation ensures the accuracy and integrity of financialrecords by identifying discrepancies and errors, thus fostering trust among stakeholders and facilitating informed decision-making. It's essential to ensure that all transactions are accurately recorded and accounted for.

They provide a record of customer orders, helping businesses streamline their fulfillment processes and ensure efficient inventory management. In contrast, invoices are important for accounting records and tracking payments. Invoice date 5. Due date 6. Accepted payment methods 7.

Reconciling payments involves verifying whether the payments received in the company's bank account match the corresponding invoices or payment records in the company's financial system. It ensures accuracy, financial integrity, fraud detection, compliance, efficient cash flow management, and informed decision-making.

Direct Bank Transfers Seamless Payments: Automated payroll systems facilitate direct deposits into employees’ bank accounts, streamlining the payment process and eliminating the need for manual cheque handling. Efficient Reporting: Generates accurate reports needed for audits and compliance checks. Enhanced Data Security 6.1

Finance reconciliation plays a pivotal role in ensuring the reliability and accuracy of a business's financialrecords. This essential practice involves comparing transactions and other financial activities with supporting documentation and resolving any discrepancies that may arise. What is finance reconciliation?

Recording transactions, Managing accounts receivable and payable, Monitoring the cash flow, Reconciling bank accounts, Creating journal entries, Issuing invoices, Payroll tax preparation, income tax, sales tax, tax return, etc. Bookkeeping is the process of tracking finances and keeping records. When to Hire a Full Charge Bookkeeper?

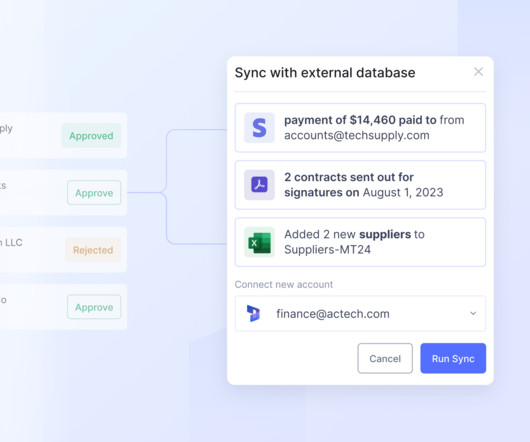

Automated Accounts Reconciliation software like Nanonets can cohesively consolidate all data sources on one platform, automate the matching logic across external data sources and general ledgers, effectively provide an audit trail, and keep the process transparent for the accounting team personnel involved.

There are several types of general ledger reconciliations: Bank Reconciliation : This type of reconciliation involves comparing the transactions recorded in the general ledger with those reflected in the company's bank statements. Scalability and Adaptability : Automation is scalable and adaptable to evolving business needs.

Establishing a record-keeping system for tracking income and expenses is essential. Accurate financialrecords can simplify tax preparation, inform business decisions, and ensure legal and financial compliance. First and foremost, you need to establish a record keeping system to maintain accurate financialrecords.

One misplaced digit could lead to miscalculations, resulting in financial discrepancies that could harm your business. Accounting automation ensures precision, minimizes errors, and maintains the integrity of your financialrecords. These trails prove invaluable during audits and compliance checks.

Stripe directly fetches this data through Financial Connections on a daily basis, ensuring alignment between Stripe's records and actual bank deposits. Thorough Documentation : Complete records of the reconciliation process provide comprehensive insights and facilitate audits.

Incorrect data entries and data omissions can lead to inaccurate financialrecords. Lack of security Manual accounting processes typically involve maintaining physical records. Easy access to essential data helps track trends, detect fraud, and assess a business's financial health.

The goal of an expense reimbursement process is not just to ensure that employees are compensated in a timely and fair manner but also to maintain accurate financialrecords and comply with tax laws and regulations. Reconciliation Tools Reconciliation is crucial for maintaining accurate financialrecords and ensuring compliance.

Account reconciliation is a critical process in accounting, which ensures that financialrecords are accurate and consistent. By incorporating efficient reconciliation in accounting practices, organizations can maintain a solid financial foundation, detect discrepancies, and reduce the risk of financial errors.

A real estate accountant is in charge of several financial duties involved in the administration of real estate assets. A real estate accountant’s primary responsibilities include: Bookkeeping : maintaining accurate financialrecords, including rent roll, accounts payable, accounts receivable, and general ledger.

Bank statement processing is essential for accurate reconciliation , auditing, and financial reporting. Maintain an efficient audit trail for future retrieval. Reconciliation This step involves matching the extracted data with the company’s internal records. general ledgers ).

In this blog, we will explore the essential task of filling out receipt books, a foundational element of financialrecord-keeping for both small and large businesses. Documenting transactions in receipt books ensures accuracy in financial management, compliance with tax regulations, and the ability to resolve discrepancies with ease.

This lets you have the right financialrecords which are a must for reporting and tax times. Financial Statements: Invoicera can make important statements like income report, cash flow details, and the overall money situation paper. This can be especially helpful during audits or tax season.

In addition to accelerating the reconciliation process, reconciliation software also enables an audit trail, significantly improving transparency and accountability. Once approved, the reconciled data is securely stored in a centralized database, ensuring an auditable trail.

We organize all of the trending information in your field so you don't have to. Join 52,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content