This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Related Courses Bookkeeping Guidebook Corporate Cash Management How to Audit Cash What is a BankReconciliation? A bankreconciliation is the process of matching the balances in an entity's accounting records for a cash account to the corresponding information on a bank statement.

BankReconciliation is the process of matching the company's cash books to the bank statement. Reconciliation includes matching the company’s balance sheet, income statement, bank statements, and expenses. Bankreconciliation is crucial for identifying and minimizing such losses.In

Related Courses BankReconciliation Essentials Bookkeeping Guidebook How to Audit Cash What is a BankReconciliation Statement? A bankreconciliation statement is a form used to compare internal records of checking account activity to those stated by the bank.

A proof of cash is essentially a roll forward of each line item in a bankreconciliation from one accounting period to the next, incorporating separate columns for cash receipts and cash disbursements. A proof of cash is more complicated to complete than a bankreconciliation.

According to Amazon Web Services , APIs are mechanisms that enable two software components to communicate with each other using a set of definitions and protocols. Improved Efficiency With APIs, accounting and finance teams can automate tasks such as data entry and bankreconciliations, saving time and reducing the manual workload.

The report may also be used as part of the bankreconciliation process, to determine which issued checks have not yet cleared the bank, and so are reconciling items. The report is used to determine the exact payments included in a check run; as such, it is considered a necessary part of the accounts payable process.

Or, a bankreconciliation is used to detect unexplained withdrawals from a savings account. Once these issues have been identified, managers can take steps to reduce the risk of their re-occurrence, typically by altering the underlying process.

Related Courses BankReconciliation Essentials How to Audit Cash Optimal Accounting for Cash What is a Bank Balance? A bank balance is the ending cash balance appearing on the bank statement for a bank account. Terms Similar to Bank Balance The bank balance is also known as the balance per bank.

Related Courses BankReconciliation Essentials Bookkeeping Guidebook How to Audit Cash What is an Outstanding Deposit? An outstanding deposit is that amount of cash recorded by the receiving entity, but which has not yet been recorded by its bank.

The concept is commonly used in regard to the ending cash balance, which is then compared to the cash balance in the monthly bank statement as part of a bankreconciliation. These two balances are rarely the same, due to such adjusting items as uncashed checks, deposits in transit , and bank account fees.

Review bankreconciliations , count on-hand cash, confirm restrictions on bank balances, issue bank confirmations. Substantive Procedures This step involves a broad array of procedures, of which a small sampling are: Analysis. Conduct a ratio comparison with historical, forecasted, and industry results to spot anomalies.

This review process is known as a bankreconciliation. Daily BankReconciliationsBank statements can be delivered on paper or as electronic versions that customers can access on the bank website and download.

It is essential to reconcile your book balance to the balance per bank on a regular basis, to ensure that your accounting records are aligned with the bank’s records, and that all discrepancies between these balances have been investigated and corrected.

Related Courses BankReconciliation Essentials Bookkeeping Guidebook How to Audit Cash What is an NSF Check? An NSF check is a check that was not honored by the bank of the entity issuing the check, on the grounds that the entity's bank account does not contain sufficient funds.

Dext Precision , as an example, will scan the ledger for the period in question and point out warnings for things such as duplicates, unreconciled items, problems with bankreconciliations multi-coded contacts, and a whole lot more. The post Accounting Automation: The Definitive 2023 Guide appeared first on Future Firm.

Related Courses BankReconciliation Essentials Bookkeeping Guidebook How to Audit Cash What is a Book Balance? An organization uses the bankreconciliation procedure to compare its book balance to the ending cash balance in the bank statement provided to it by the company's bank.

Accounting for Bank Charges A business that incurs bank charges will usually record them as expenses as part of its monthly bankreconciliation process. Related AccountingTools Courses BankReconciliation Essentials Corporate Cash Management How to Audit Cash Related Articles Bank Debits Debit Memo

An outstanding check is a check payment that has been recorded by the issuing entity, but which has not yet cleared its bank account as a deduction from its cash balance. The concept is used in the derivation of the month-end bankreconciliation.

If you are not sure about the nature of a debit, contact your bank for an explanation. Related AccountingTools Courses BankReconciliation Essentials Corporate Cash Management How to Audit Cash Related Articles Bank Charge Debit Memo How to Reconcile a Bank Statement Memo Debit

Other reasons for a returned check are as follows: The check is drawn on a foreign account The check has been disfigured, so that payee, account, or payment information cannot be discerned The check contains a mismatch between the numeric and written amount to be paid The check was presented for payment too long after the check date, rendering it void (..)

The term can also be applied to a situation where an individual attempts to make a purchase with a debit card, and there are not sufficient funds in the underlying bank account to pay for the transaction. Related Articles BankReconciliation Procedure NSF Check The BankReconciliation Process

Related Courses Corporate Cash Management How to Audit Cash What are Bank Errors? Bank errors are transactions that have been incorrectly recorded by a bank in a customer’s account. There are usually few bank errors, which are concentrated in the areas of incorrect check and deposit amounts.

Examples of such items are recording expenses for supplier invoices that have not yet arrived, recording revenue for customer invoices that have not yet been billed, recording errors spotted in the month-end bankreconciliation , adjusting for transactions that were initially recorded in the wrong account, or accruing for unpaid wages earned.

Reconciling the bank statement involves comparing the company's internal financial records or ledger to the bank statement received via the bank. Key takeaways: Bankreconciliation is the transaction matching of your records against the bank statement. How do you reconcile your bank statement?

The actual amount of cash on hand can vary from the ledger cash amount if a business does not conduct bankreconciliations on a regular basis. Related Articles Cash Reconciliation Terms Similar to Ledger Cash Ledger cash is also known as book cash.

Related Courses BankReconciliation Essentials Bookkeeping Guidebook How to Audit Cash What is a Bounced Check? A bounced check is a check that does not have a sufficient amount of cash in the underlying bank account to support the payment, so the issuing bank refuses to honor it.

In accounting, the "in transit" term is most commonly applied to deposits that are in transit from a company to its bank, resulting in a reconciling item on the company's bankreconciliation if the checks are in transit at the end of a month. The bank does not record the check in its books until the following day, August 1.

A payer can verify whether the checks it has issued have been classified as cancelled by accessing the on-line check record posted by the payer's bank. This information is most commonly used as part of the bankreconciliation process, but can also be used to prove to a payee that a check payment was made, and that the check was cashed.

A deposit in transit is cash and checks that have been received and recorded by an entity, but which have not yet been recorded in the records of the bank where the funds are deposited. It records the check as a cash receipt on the same day, and deposits the check at its bank at the end of the day. Why Does a Deposit in Transit Occur?

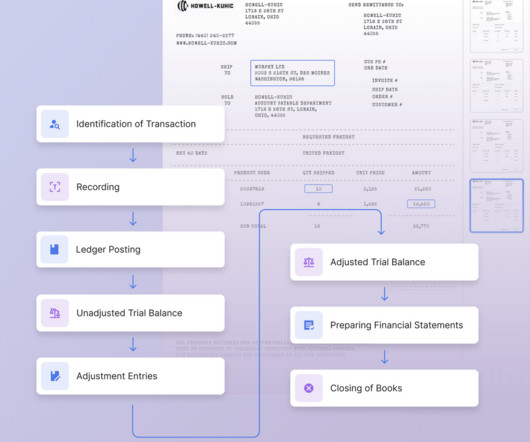

Comparing an Unadjusted and Adjusted Trial Balance Given these definitions, the difference between the two types of trial balance are the adjusting entries made into the accounting system after the unadjusted trial balance is prepared.

The latter definition is more commonly used. Thus, in most situations, the primary difference between the ledger balance and available balance is checks that the company or individual has deposited in his account, but which the bank has not yet made available for use.

Some reconciling items may require adjustment to the records of the recording entity, such as an uncashed check fee that has been imposed by the entity's bank. These are fees charged by an entity’s bank, such as check processing fees, that have not yet been recorded by the firm in its accounting records.

Another example is a bankreconciliation , which can detect unexpected withdrawals from a bank account. Examples of Detective Controls An example of a detective control is a physical inventory count , which can spot instances in which the actual inventory is lower than what is stated in the accounting records.

For example, the schedule should show instances in which a check was issued near the end of a reporting period and was not listed as an outstanding check in the bankreconciliation. Kiting is occurring if the same cash deposit is appearing in two accounts at the same time.

The information in the cash book is routinely compared to the bank's records via a bankreconciliation to ensure that the information in the book is correct. If not, an adjusting entry is made to bring the cash book into conformance with the bank's information.

Related Courses Bookkeeping Guidebook Corporate Cash Management How to Audit Cash What is a Restrictive Endorsement? A restrictive endorsement limits the use of a financial instrument (usually a check ).

This situation typically arises when a person or business is too optimistic in assuming that deposited funds have cleared the bank and are available for use, and so writes checks for which funds are not yet available.

Related Courses Bookkeeper Education Bundle Bookkeeping Guidebook What is an Account Reconciliation? An account reconciliation is the actions taken to prove that an account balance is valid. It is also a key task to be completed before an organization’s books are audited at the end of each year.

Related Courses Corporate Cash Management Credit and Collection Guidebook Effective Collections How to Audit Cash What is a Post Dated Check? A post dated check is a check on which the issuer has stated a date later than the current date.

External auditors will likely want to use internally-prepared reconciliation statements as part of their auditing procedures , since the statements allow them to focus on reconciling items, especially in large-balance accounts that are materially significant components of the financial statements.

Examples of accounting events that frequently involve compound journal entries are: Record all payments and deductions related to a payroll Record the account receivable and sales taxes related to a customer invoice Record multiple line items in a supplier invoice that relate to different expenses Record all bank deductions related to a bankreconciliation (..)

We organize all of the trending information in your field so you don't have to. Join 52,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content