This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Related Courses Bookkeeping Guidebook How to Audit Receivables New Controller Guidebook The reconciliation of accounts receivable is the process of matching the detailed amounts of unpaid customer billings to the accounts receivable total stated in the general ledger. This is the most common reason for a difference.

Its primary purpose is to ensure the accuracy and completeness of financial records so that financialstatements can be prepared for internal and external reporting purposes. As part of the process, the AP team takes steps to ensure the past month’s financial records are accurate.

Related Courses Accountants' Guidebook Bookkeeping Guidebook New Controller Guidebook An accountant is a person who records business transactions on behalf of an organization, reports on company performance to management, and issues financialstatements. Management reports are issued to the management team.

Transactions may be caused by normal business activity, such as billing customers or recording supplier invoices , or they may involve adjusting entries , which call for the use of journal entries. Terms Similar to Ledger Account A ledger account is also known as an account.

FinancialStatements and Analysis 1. Review FinancialStatements Take a look at your “big three” accounting reports: income statement, balance sheet, and cash flow statement for accuracy. It will also give you a great picture of your business’s overall financial health.

Understanding accrued revenue meaning is essential because it aligns a companys financialstatements with the business’s actual performance. Key Takeaways Accrued revenue is a current asset , recorded when a business earns income but hasnt yet billed or received payment. Accounting Treatment : Recorded as a current asset.

It is especially necessary to create year-end adjustments when the financialstatements are to be audited by the company’s auditors. For example, an interest billing from the bank may arrive late, so the expense is accrued. Accrual of revenue that has been earned but not yet billed.

For example, a billing clerk, payables clerk, or payroll clerk may report to the bookkeeper. The position can be assisted by an outside CPA who advises on how to record certain of the more complicated business transactions. The full charge bookkeeper may supervise various accounting clerks.

By maintaining your books regularly, reviewing reports, and reconciling your accounts at the end of each month, you can avoid bookkeeping disasters. Accounts Payable: Recurring monthly bills and payments such as car insurance and loan payments should be entered into the books. Is your bookkeeping disorganized?

Source documents are typically retained for use as evidence when auditors later review a company's financialstatements , and need to verify that transactions have, in fact, occurred. If employee hours are being billed to customers, then it also supports the creation of customer invoices.

Traditional bookkeepers are professionals responsible for recording financial transactions, maintaining ledgers, and preparing financialstatements manually or using basic accounting software. These professionals play a crucial role in ensuring the accuracy and integrity of a company's financial records.

Manually reconciling bank statements. Producing financial reports in a spreadsheet. to prepare their financialstatements. All eyes are currently on Countable , a much more modern working papers and financialstatement preparation software that connects to Xero & QBO to automate the year-end process.

The role of payment reconciliation in maintaining financial accuracy is critical, as it helps businesses track their income, verify the legitimacy of transactions and prevent discrepancies. Accurate financial records are essential for businesses to meet auditing requirements and avoid potential fines or penalties for non-compliance.

Reconcile Cash and Receipts At the end of each day, reconcile all cash payments and payment receipts received in the general ledger to get a good idea of each client’s cash balance. Review Accounts Payable Review accounts payable at the end of the week to see if any bills are still outstanding.

Depending on the type of subledger, it might contain information about transaction dates, descriptions, and amounts billed, paid, or received. The ending balances in the general ledger are used to create financialstatements for each reporting period. A summary-level entry is periodically recorded in the general ledger.

Integrate Nanonets Reconcilefinancialstatements in minutes Explore for Free Are you a spreadsheet wizard who won't back down against the most daunting and time consuming transaction tasks? If Pricing is an issue you may try to use Power Query to reconcile in excel. Use CubeSoftware.

Essential Insights: Purpose : The core objective of cash reconciliation is to identify mismatches between the cash on hand and the sales transactions recorded, thereby safeguarding against financial inaccuracies in a company's records. Recording the starting cash amount in the drawer, itemized by bill and coin types.

QuickBooks is one of the most widely used apps for bookkeeping, and it offers a convenient way to reconcile credit cards without needing external tools. Step 1: Go to the reconciliation menu In the top help menu bar, search for 'Reconcile.' ' Then, select the account you wish to reconcile.

Billing Clerk The billing clerk position is responsible for invoicing customers, submitting the invoices to customers by whatever means are required, issuing credit memos, and keeping the billing records up-to-date. It also reconciles general ledger accounts. It also reconciles general ledger accounts.

Also, credit card reconciliation is the process of confirming that all transactions on your credit card statement are properly reflected in your accounting records. Why is reconciling credit cards difficult? Reconciling credit cards can be difficult for several reasons. These fees can be difficult to keep track of.

In simple words, bookkeepers ensure that all of your business income, expenses and transactions are recorded in your book and they reconcile your company’s financial accounts every month. In addition to that, bookkeepers can also help you prepare your company’s financialstatement and financial report.

Billing Cycle If the company recognizes revenue at the end of each month but sends invoices at the start of the following month, the timing of the billing cycle may not align with recognizing the revenue received. One-Time Projects Especially prevalent for SaaS companies where customers are billed after implementation completion.

Intercompany accounting is significantly more complicated than standard accounting since it requires balancing multiple ledgers, tracking internal/external transactions, forex conversion, performing intercompany eliminations and settlements, and preparing a consolidated financialstatement. Why is intercompany Reconciliation important?

The unadjusted trial balance is the listing of general ledger account balances at the end of a reporting period , before any adjusting entries are made to the balances to create financialstatements. What is an Adjusted Trial Balance?

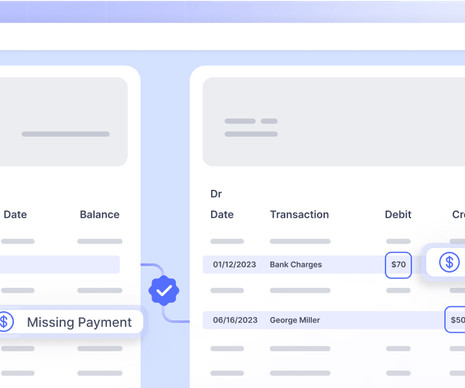

Before making payments to vendors, it's essential to check that the vendor bills the company the correct amount. Accounts payable teams must reconcile payments regularly to avoid double-processing them. Reconcile Discrepancies: Spot any differences, such as missing payments or invoices.

It is a record of all financial transactions of an enterprise and provides a comprehensive account of the organization's monetary activities. However, the GL is not the sole repository of financial data. It ensures that all outstanding bills are accurately accounted for and paid in a timely manner.

An account receivable is documented through an invoice , which the seller is responsible for issuing to the customer through a billing procedure. The accounting staff should reconcile the two as part of the period-end closing process. This is considered a short-term asset , since the seller is normally paid in less than one year.

Bills & Expense Apps Every business has expenses. Simplify your financial management with bills and expense apps that offer the convenience of handling unlimited invoices. Invoicing, Billing & Proposal Apps What good is it to be in business if you don’t get paid? Ready to dive in? You need Practice Ignition.

Payment reconciliation software tools are designed to automate and streamline the process of matching and reconcilingfinancial transactions within a business. Adjustment Recording : Adjustments in the accounting system are made to reconcile accounts, such as accounting for bank fees, interest earned, or rectifying errors.

It links different apps, such as invoicing tools, expense tracking software, and financial dashboards, to automate tasks like creating invoices, reconciling accounts, managing payroll and project deadlines, and much more. The software automatically reconciles all transactions between two sets of records (e.g.,

Another approach utilizes analytical tools to compare current financial activity with historical patterns, aiding in the detection of anomalies or discrepancies. Comparing Bank Statements with Internal Records: Matching transactions, highlighting differences, and verifying balances.

The Importance of Expense Reconciliation Expense reconciliation holds significant importance in the realm of finance and accounting for several reasons: Financial Accuracy : One of the primary reasons for expense reconciliation is to ensure the accuracy of financial records.

Acting as a centralized platform, it retrieves data from the general ledger and compares it with bank statements and invoices, facilitating accurate and swift account reconciliation. Once approved, the reconciled data is securely stored in a centralized database, ensuring an auditable trail. User-friendly interface and easy navigation.

In essence, the intent is to use adjusting entries to produce more accurate financialstatements. It is usually not possible to create financialstatements that are fully in compliance with accounting standards without the use of adjusting entries.

Set up Recurring Transactions Your financial management procedures may be significantly simplified by setting up recurring transactions in Quickbooks Accounting. Automating routine financial activities, such as energy bills, subscription payments, and monthly invoicing, can save time and minimize the possibility of payment defaults.

It typically involves releasing funds for specific purposes, such as paying bills, making payments to suppliers, settling loans, or disbursing wages or salaries to employees. It is categorized as an expense or payment, and its impact on the financial position and income statement is noted. How do Disbursements Work?

Alternatively, the cashier could simply count out the cash for the petty cash fund, if there are enough bills and coins on the premises. However, the difference is so minor that it is completely immaterial to the results in the financialstatements.

By reconciling invoices and payments promptly, businesses can avoid overpaying or missing payments, thereby maintaining healthy cash flow levels. This may involve contacting vendors, reviewing payment documentation, or reconciling records with bank statements.

However, many small business owners see the intricacies of bookkeeping as a chore and don’t do a thorough job of reconciling their finances. Credit card balances, loan payments, and past-due bills weigh down many businesses and reduce their profit-making capacity.

Related Courses Business Ratios Guidebook Credit and Collection Guidebook The Interpretation of FinancialStatements What is Accounts Receivable Analysis? This report divides the age of the accounts receivable into various buckets, which you can sometimes alter within the accounting software to match your billing terms.

Falling behind on your bookkeeping can leave you struggling in multiple areas: Missed payments: If you aren’t tracking bills and invoices, you could miss important due dates. Skewed financial data: If your bookkeeping is behind, your financial reports will be wrong. This could lead to late fees or damage to your credit score.

Other financial documents: Other financial documents such as invoices, receipts, bills, and other proof of income documents can also be used as sources of financial information that can be extracted and stored for various purposes.

This process is vital for a myriad of functions, such as reconciling invoices with the general ledger, and extends to numerous other business processes including inventories, payroll, sales, and customer information, among others. This might involve additional validation checks or comparisons to guarantee the integrity of the reconciled data.

This is particularly useful for tasks like invoice processing, receipt management, and extracting information from financialstatements. This automation allows them to focus on more strategic and analytical aspects of financial management. Users are billed at $0.08 per receipt and $0.16

We organize all of the trending information in your field so you don't have to. Join 52,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content