This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Related Courses Bookkeeping Guidebook Corporate Cash Management How to Audit Cash Reconciling a bank statement involves comparing the bank's records of checking account activity with your own records of activity for the same account. To reconcile a bank statement, follow the steps noted below. If so, adjust your record of the deposit.

Bank Reconciliation Vs. Book Reconciliation In accounting and financial management, we encounter the terms "Book Reconciliation" and " Bank Reconciliation " These terms are often used interchangeably, leading to ambiguity regarding their meanings. What Is Book Reconciliation?

Related Courses Bank Reconciliation Essentials Bookkeeping Guidebook How to Audit Cash What is an Outstanding Deposit? An outstanding deposit is that amount of cash recorded by the receiving entity, but which has not yet been recorded by its bank. The bank will record the receipt in the company's account the following Monday, April 3.

The goal of this process is to ascertain the differences between the two, and to book changes to the accounting records as appropriate. Bank Reconciliation Terminology The key terms to be aware of when dealing with a bank reconciliation are: Deposit in transit. Outstanding check. NSF check.

The ending balance of your version of the cash records is known as the book balance , while the bank's version is called the bank balance. It is extremely common for there to be differences between the book balance and bank balance in a bank reconciliation, which you should track down and adjust in your own records. Recording errors.

What is a Deposit in Transit? A deposit in transit is cash and checks that have been received and recorded by an entity, but which have not yet been recorded in the records of the bank where the funds are deposited. Why Does a Deposit in Transit Occur? When is There No Deposit in Transit?

Related Courses Bank Reconciliation Essentials Bookkeeping Guidebook How to Audit Cash What is a Book Balance? A book balance is the account balance in a company's accounting records. Adjustments to Deposits The company may sometimes record a deposit incorrectly, or it may deposit a check for which there are not sufficient funds (NSF).

What is the Book Balance? The book balance is the in-house general ledger record of the same account. Comparing the Bank Balance and Book Balance There are multiple differences between the bank balance and book balance, which are as follows: Checks outstanding. Deposits in transit. Unrecorded fees.

What is a Book Balance? A book balance is the account balance in a company's accounting records. The Difference Between the Bank Balance and Book Balance The bank balance reported by your bank is usually different from the book balance in your accounting records. Deposits in transit. Interest on deposited cash.

These services streamline operations, keep your books clean, and provide you with the insights you need to make better business decisions, whether you’re selling locally or shipping goods across the globe. That’s why investing in optimized accounting services for ecommerce stores isn’t merely a good idea, it’s crucial.

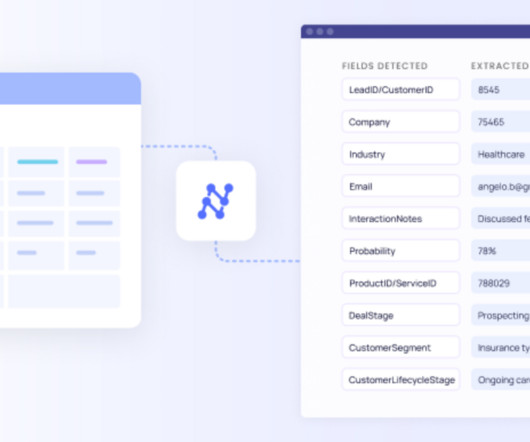

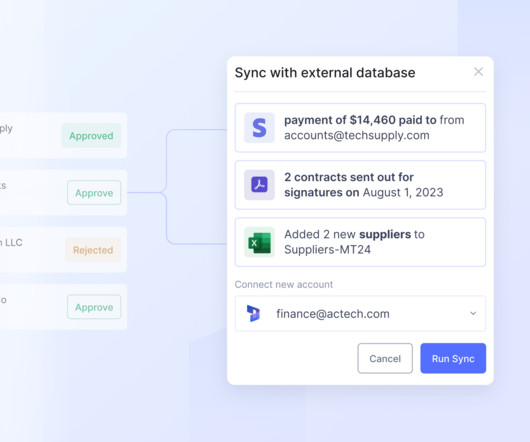

Integrate Nanonets Reconcile financial statements in minutes Explore for Free Manual reconciliation processes are more complex when balance sheet transactions require reconciliation across multiple general ledgers, ERPs, invoices, and bank accounts. Note the balance as per the books recorded by your company at the end of the period.

Reconcile bank statements The next step in your bookkeeping cleanup checklist is to reconcile your bank statements. Make a note of any discrepancies, like a missing check or deposit. So once you catch up on your books, continue to reconcile your bank statements each month.

It typically outlines outstanding checks, deposits in transit, bank fees, errors, and any other differences between the two sets of records. Check out Nanonets Reconciliation where you can easily integrate Nanonets with your existing tools to instantly match your books and identify discrepancies.

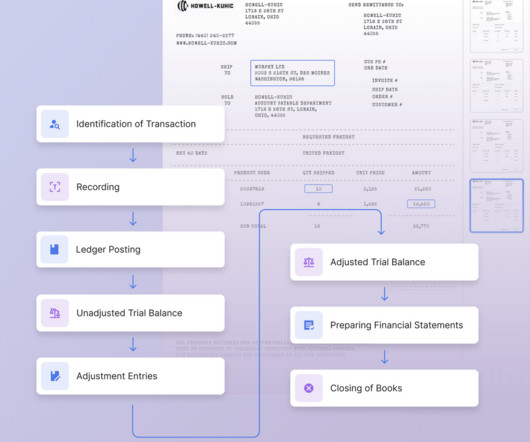

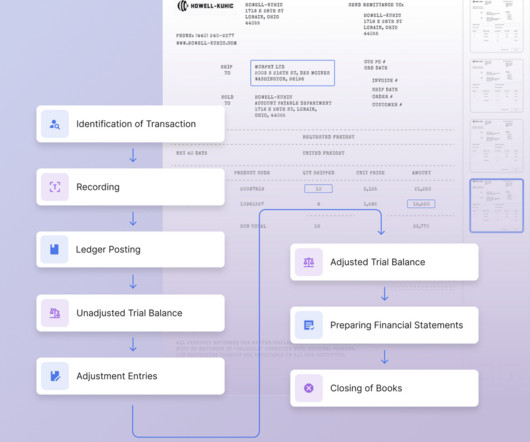

Bank Reconciliation is the process of matching the company's cash books to the bank statement. However, let's understand the manual bank reconciliation process once: Step 1: Gather documents On the bank side, you need the bank statements, outstanding checks, deposits, and any pending transactions.

Bank Reconciliation is the process of matching the company's cash books to the bank statement. However, let's understand the manual bank reconciliation process once: Step 1: Gather documents On the bank side, you need the bank statements, outstanding checks, deposits, and any pending transactions.

At the heart of this reconciliation lies the creation of journal entries, which serve to align discrepancies between the company's books and the bank statement. Check out Nanonets Reconciliation where you can easily integrate Nanonets with your existing tools to instantly match your books and identify discrepancies.

By maintaining your books regularly, reviewing reports, and reconciling your accounts at the end of each month, you can avoid bookkeeping disasters. Finally, having clean books simplifies making wise business choices and helps you stay organized for tax season. Are you looking for someone to manage your books?

The bank reconciliation process involves several steps: Gathering Necessary Documents: Collecting bank statements, checkbooks, deposit slips, and invoices, bills, and receipts for comparison. Identifying and Investigating Discrepancies: Searching for missing deposits or unauthorized charges, and contacting the bank if needed.

In the meantime, the difference will be a reconciling item. Update Deposits in Transit Go to the deposits section of the bank reconciliation module. The system will display a list of deposits in transit. Match these deposits against the list of deposits that have cleared the bank, as listed on the bank statement.

Learning to reconcile with QuickBooks Online is a starting step for using QuickBooks to manage books. QuickBooks is a handy tool to help you reconcile your accounts without using any external tools. Step 1: Go to the reconciliation menu Search for “Reconcile” in the top help menu bar.

I recommend starting out with all invoices, customer payments, and deposits. Tip #2: Reconcile business bank and credit card accounts. Symptom #1: Whenever they go into bank deposits , they see that they have a lot of old unclear transactions in undeposited funds. Step #3: A deposit is recorded to the correct bank account.

Manually reconciling bank statements. Before the books are closed, it’s typical for senior accountants to review the books to spot any accounting errors or potential issues. Most firms help their small business clients with different finance and accounting operations like their books, bill pay, payroll, accounts payable, etc.,

AvidXchange’s supplier portal helps Doron Contracting save time and more easily reconcile invoices. AvidXchange’s supplier portal helps Doron Contracting save time and more easily reconcile invoices. She can match her books to the supplier portal to ensure invoices are paid in full and on time. And what day?’” Doron said.

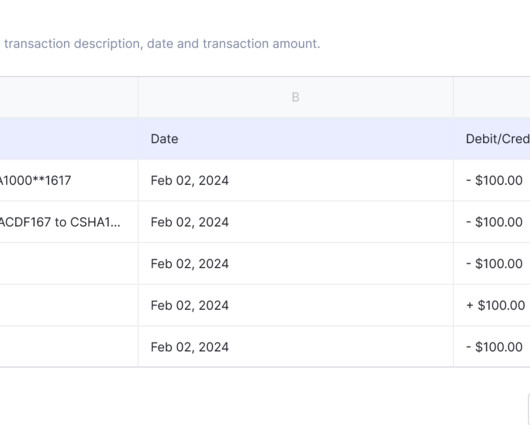

A bank reconciliation statement is a financial document that compares a company's bank account balance to the transactions recorded on its general ledger, often called the "cash books." For example, a deposit of $5,000 on June 1st and a check #123 for $1,000 on June 3rd. " We need to add these to the bank statement. "

That’s a long time to think about those jobs and have them on the books.” With this early payment option, if a supplier chooses to accelerate an eligible invoice, AvidXchange deposits the funds directly into their account in as little as 24 hours for a small fee. He appreciates the service and the ability to clear his books.

Any discrepancies may have arisen at the bank (such as a transposed number in a check payment or a deposit), for which the bank should be contacted at once to make an adjusting entry. A bank statement is a document that is issued by a bank once a month to its customers, listing the transactions impacting a bank account.

How do you communicate, share documents, and collaborate on the books? Client collaboration: Client Hub (use discount code vwasek5mb to receive 50% off your first 3 months), or Keeper (use this link to book a demo, and use my affiliate code: VMWasek to receive 3 months of free white labelling). Step 2: do the reconciliations.

Whether it's ensuring that expenses align with available funds or guaranteeing that business transactions accurately reflect the company's financial standing, tracking checks outstanding and reconciling bank statements is non-negotiable. Neglecting them can result in fees, credit damage, and legal consequences.

In accounting, the "in transit" term is most commonly applied to deposits that are in transit from a company to its bank, resulting in a reconciling item on the company's bank reconciliation if the checks are in transit at the end of a month. The bank does not record the check in its books until the following day, August 1.

A reconciliation statement is a document that begins with a company's own record of an account balance , adds and subtracts reconciling items in a set of additional columns, and then uses these adjustments to arrive at the record of the same account held by a third party. Debt accounts. Accounts receivable.

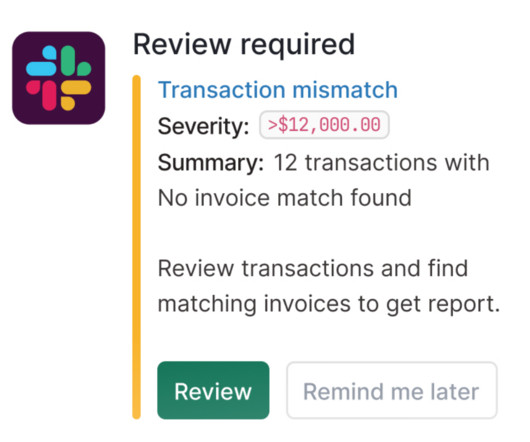

As a matter of fact, by reconciling payments regularly, businesses can quickly detect discrepancies, such as missed or duplicate payments, incorrect amounts or unauthorized transactions. When payments are reconciled promptly, businesses have a clearer understanding of their incoming revenue, allowing for better planning and forecasting.

Matching and validating entries would mean data consolidation across sub-ledgers, vendor invoices, bank statements, receipts, and account receivables to ensure timely and accurate month-end and year-end closing of the financial books. Account Reconciliation can be a fairly manual task, especially right before the monthly close.

Reconcile Cash and Receipts At the end of each day, reconcile all cash payments and payment receipts received in the general ledger to get a good idea of each client’s cash balance. Deposit Cash and Check Payments Most client transactions these days likely take place electronically.

By comparing and reconciling expenses against various financial documents, businesses can detect and correct any discrepancies or errors, ensuring that their financial statements reflect the true state of their finances. Compliance and Regulation : Expense reconciliation is crucial for compliance with financial regulations and standards.

It itemizes the deposits, withdrawals, and other activities impacting the checking account for a one-month period. This can be caused by deposits made by the account holder that have not yet been recorded by the bank, or by checks issued by the account holder that have not yet been presented to the bank.

Prompt depositing and recording cash receipts minimizes the risk of theft or misappropriation. REGULAR, SCHEDULED RECONCILIATIONS To ensure accuracy, a quality bookkeeping system enforces regular reconciliation – comparing and matching financial records from different sources, such as bank statements and company books.

Stripe directly fetches this data through Financial Connections on a daily basis, ensuring alignment between Stripe's records and actual bank deposits. The system intelligently analyses transaction data, identifies patterns, and reconciles accounts efficiently, saving valuable time and resources.

It ensures that all bank transactions, including deposits, withdrawals, and bank fees, are accurately recorded in the general ledger. Inventory Reconciliation : Inventory reconciliation involves reconciling the quantities and values of inventory recorded in the general ledger with the actual physical inventory on hand.

Recording transactions, Managing accounts receivable and payable, Monitoring the cash flow, Reconciling bank accounts, Creating journal entries, Issuing invoices, Payroll tax preparation, income tax, sales tax, tax return, etc. You can focus on making the future bright. When to Hire a Full Charge Bookkeeper?

Maintain Your Books All Year When you file taxes, the IRS will want to inspect all aspects of your small business finances to ensure that you are running your business correctly and paying all of the correct taxes. We make sure your books look seamless, and we track all of your financial metrics for you all year long.

Accounting: For companies, bank statements are crucial for reconciling accounts and ensuring accurate financial records. This simplifies the bank statement verification process and also helps reconcile them faster. Source 💡 As per the Archives of the U.S. Department of Justice , Both 18 U.S.C. §

Accounting professionals often find themselves wrestling with mundane tasks: reconciling transactions, generating reports, or manually inputting data, leaving them little time for value-added activities. Zoho Books Zoho’s invoicing software packs a punch with its comprehensive suite of business applications.

Before closing the books for August, the business records the earned revenue as accrued revenue, ensuring accurate reporting for the period. Example : A customer pays a deposit for a custom product expected to ship months later. So this fills this gap by recognizing income tied to obligations fulfilled before payment is invoiced.

Once approved, the reconciled data is securely stored in a centralized database, ensuring an auditable trail. It quickly matches cash outgoings and receipts, reconciles bank accounts with accounting records, and verifies totals against balance sheets, cash flow statements, and income statements.

We organize all of the trending information in your field so you don't have to. Join 52,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content