This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Reduce Days Sales Outstanding (DSO): Objective: Decrease the average number of days it takes to collect payments, thereby improving cash flow. Efficient Collection Processes: Streamlined invoicing and follow-up procedures leading to quicker payments. A lower DSO indicates prompt collections, enhancing cash flow.

Processed accounts payable and receivable, ensuring timely payments and collections. Reconciled bank statements monthly, maintaining accurate financialrecords. Generated monthly financial reports, including profit and loss statements and balance sheets. Created and maintained spreadsheets for tracking key financial data.

Review Your Books: Perform regular reviews of your businesss financialrecords to ensure that it is accurate and up to date. Heres how you can streamline document collection, bookkeeping, and tax filing preparation: 1. Common deductions include office supplies, travel expenses, and interest on business loans.

This is especially true when it comes to scaling collections. In the past, this was done by hiring more team members to manage ERP dunning emails or collections calls. But now, there is more data available that can be used to streamline and improve A/R collections management. What is A/R Collections Automation?

This is especially true when it comes to scaling collections. In the past, this was done by hiring more team members to manage ERP dunning emails or collections calls. But now, there is more data available that can be used to streamline and improve A/R collections management. What is A/R Collections Automation?

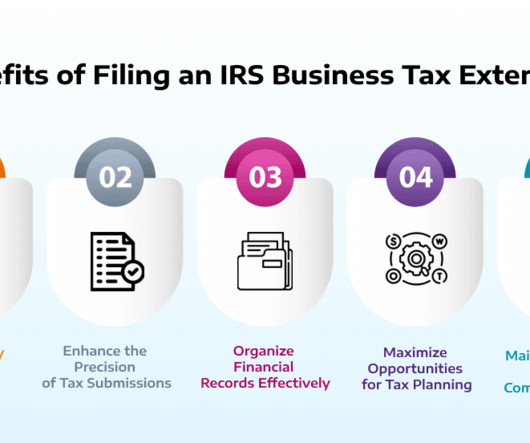

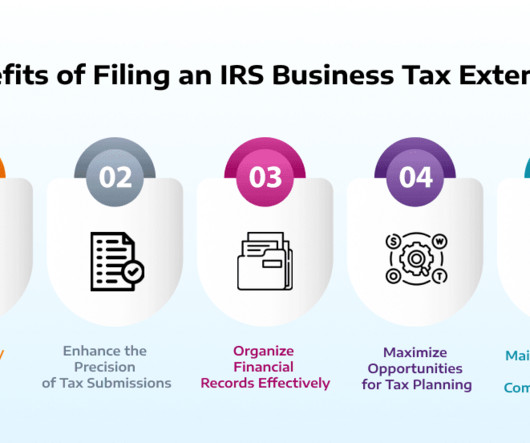

While its not an extension to pay taxes owed, it grants businesses the flexibility to organize their financialrecords. This extension offers invaluable support for companies managing complex financials or experiencing delays in gathering necessary documents. Alternatively, they could incur penalties and interest.

Bookkeeping is the process of recording and organizing all financial transactions for your business. It involves tracking every dollar that goes in and out of your accounts, ensuring your financialrecords are accurate and up to date. Timely collections improve your cash flow.

While its not an extension to pay taxes owed, it grants businesses the flexibility to organize their financialrecords. This extension offers invaluable support for companies managing complex financials or experiencing delays in gathering necessary documents. Alternatively, they could incur penalties and interest.

Account management: They manage accounts payable and receivable, process invoices, reconcile accounts, and ensure timely payments and collections. Basic financial reporting: They generate basic financial reports, such as income statements and balance sheets, summarizing financial activity for a specific period.

The complexity of such fraud often requires detailed audits and advanced analytical tools to detect discrepancies in reported revenue versus actual collections. Plus, it allows you to collect receivables without identifying your bank account information to your customers.

At a high level, this process is accomplished through invoicing and collections, and includes sending the invoice, managing collections, processing payments, matching payments to invoices, and posting the payments. If the internal review of the invoice checks out, the collections outreach begins.

Tax Implications Marketplace: Goods and Services Tax (GST) obligations may vary depending on whether the platform collects and remits GST on behalf of sellers. Proper financial management can enhance profitability, improve compliance, and support long-term growth. Still doing accounting the old way?

Organizations use AI to process payments in real-time, resulting in quicker reconciliation, more accurate financialrecords, and an improved cash flow. More accurate financialrecords also lead to businesses proactively managing their cash flow and other enhanced decision making. Use cases include: Real-time processing.

To make this process as smooth and seamless as possible you need to create a process to collect essential details such as business financialrecords, invoices, receipts and tax documents. Could you please gather the following documents: Business financialrecords (e.g.,

Essential Accounting Tips for Singapore’s F&B Industry The food and beverage (F&B) industry in Singapore faces unique challenges, especially in terms of financial management. In this post, we’ll cover some essential accounting practices and tips that can help streamline financial management for F&B businesses in Singapore.

Gather Relevant Documents Collect all the necessary documents required for the audit, including vendor invoices, purchase orders, payment records, contracts, and approval documents. Access Controls : Verify that only authorized personnel can access the AP system and financialrecords.

These procedures can indicate possible problems with the financialrecords of a client, which can then be investigated more thoroughly. Analytical procedures involve comparisons of different sets of financial and operational information, to see if historical relationships are continuing forward into the period under review.

Keeping track of payments, memberships, renewals, and other financialrecords manually can quickly become overwhelming, time-consuming, and prone to errors. Notify clients of upcoming dues and ensure timely collections while reducing manual follow-ups. This ensures steady cash flow without you having to manually remind clients.

The first thing to understand is that the CRA is entitled to review all financialrecords from the period under review. Take a look at your tax return and collect any information you need to support your claim. These documents will include bank statements, invoices, T4 slips, and tax returns.

Accounts receivable reconciliation is a fundamental accounting process that involves comparing and verifying the balances in the accounts receivable ledger against supporting documentation and external records. Any discrepancies found are investigated and resolved to maintain the integrity of the financialrecords.

All companies need to master tax systems by understanding how registration functions alongside collection procedures as well as remittance protocols. Using an invoice factoring calculator can assist in keeping financialrecords in sync when dealing with advances on receivables.

Gathering data over longer periods may require cross-collaboration with teams and even manual data collection. Automation eliminates the manual components behind the data collection process, making it more efficient. Requires more time and resources. Lack of historic data. Overlooks more immediate cash flow needs.

Take a look at this bookkeeping cleanup checklist to get all your financial ducks in a row. Collect all your financialrecords It’s hard to say which part of this process is the most difficult, but depending on the type of business you have, rounding up all your past financialrecords may be the most time-consuming.

It is easy to feel overwhelmed with the amount of information that needs to be collected and make mistakes when it comes to reporting income or expenses. Contact us at 855-998-3041 to confirm compatibility with your financial institution. Simplify your financial management and focus on what matters most.

As we approach the end of the year, it’s essential for small business owners to review their financialrecords and ensure everything is in order. Reconcile Bank Accounts Ensure your bank statements align with your accounting records. This step helps maintain accuracy in your financialrecords.

It’s a fundamental part of a company’s working capital and financial health, with the AP department responsible for processing invoices, making payments, and managing relationships with vendors. Keep Records Up-to-Date Maintain up-to-date records throughout the year. How Often Should an Audit for AP be Conducted?

From 1099 preparation services to year-end bookkeeping and full-year QuickBooks write-ups , ensuring your financialrecords are accurate and compliant can be daunting. To prepare for this process, ensure you collect a W-9 form from every eligible vendor. Service providers such as landscapers or cleaners.

Accurate financialrecords are essential for businesses to meet auditing requirements and avoid potential fines or penalties for non-compliance. By having a systematic process in place for reconciling payments, business users can ensure that all transactions are recorded properly and that financial reports are reliable.

Picture this: a team of expert bookkeepers diligently managing your financialrecords and transactions without setting foot in your office. These professionals play a crucial role in ensuring the accuracy and integrity of a company's financialrecords. Sounds futuristic? What is digital bookkeeping?

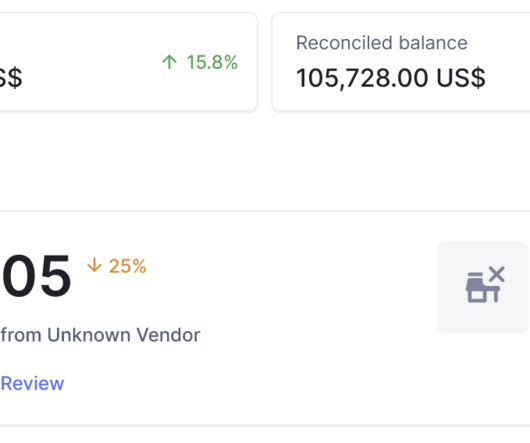

Through effective cash management practices, organizations can ensure the smooth functioning of their operations and uphold the trustworthiness of their financialrecords, making cash reconciliation a non-negotiable aspect of sound financial management. What is Cash Reconciliation? Category A Sales $503.00 -$3.00 Total $880.00

That’s because you have a moral and legal responsibility to protect your client’s financialrecords. It can help to avoid duplicate entries, simplify reporting, and ensure accurate financialrecords. This Quickbooks tip can save you time and help ensure accuracy in your bookkeeping.

Work papers are the collection of documents assembled by an auditor while examining the financialrecords of a client. Work papers provide the evidence upon which an auditor's opinion regarding a client's financialrecords is based. What are Work Papers?

In the world of finance and accounting, the process of reconciliation plays a vital role in ensuring accurate and transparent financialrecords. It is a crucial process for businesses to identify discrepancies, resolve errors, and maintain the integrity of their financial statements. What is Reconciliation?

Automation of data collection enhances the accuracy of financialrecords, leading to smoother audits. Enhancing Regulatory Reporting Automating financial data collection through analytics supports timely and accurate reporting. At Counto, we prioritise your savings and efficiency over hefty fees.

Introduction to Bank Reconciliation Journal Entries Bank reconciliation is an important process in accounting that ensures the accuracy and integrity of a company's financialrecords. It involves the comparison between the company’s internal financialrecords and those of the bank.

Real-time tracking while doing the financialrecording keeps you alerted at all times regarding the current situation of your cash flow and fastens decision-making. Faster collections When debtors are late in making payments, automated systems can issue reminders and charges, resulting in faster payments and lower outstanding balances.

Gain Insight: Choose software that provides detailed tracking of income, expenses, and overall financial performance to maintain a clear view of your business’s financial health. This practice simplifies financial management and prevents confusion. Analyse Financial Reports Regularly 4.1

Implement a system for tracking invoices, payments, and outstanding balances to ensure timely collections and payments. Ignoring Financial Reports: Small business owners often overlook the importance of financial reports in guiding strategic decision-making. Store backups securely off-site or in the cloud for added protection.

Expense reconciliation is a process within finance and accounting that ensures that a company's financialrecords accurately reflect its spending activities. At its core, it involves comparing financial data from various sources within a business to identify any discrepancies or errors and bring them into alignment.

However, these tasks can be time-consuming and prone to errors, which can result in delayed payments, inaccurate financial reporting, and, ultimately, negative impacts on the company’s bottom line. 6) Bookkeeping and Data Entry Bookkeeping and data entry are essential tasks for businesses to maintain accurate financialrecords.

In an era of increasing corporate scandals, financial frauds, and complex business transactions, ensuring the integrity and transparency of financialrecords has become paramount for organizations worldwide. And how can it help small business owners properly care for their financialrecords?

In an era of increasing corporate scandals, financial frauds, and complex business transactions, ensuring the integrity and transparency of financialrecords has become paramount for organizations worldwide. And how can it help small business owners properly care for their financialrecords?

Related Courses Credit and Collection Guidebook Bookkeeping Guidebook Budgeting CFO Guidebook Cost Accounting Fundamentals New Controller Guidebook Payables Management Payroll Management Project Accounting Someone wanting to enter the accounting field can choose to train for a number of possible positions.

Running a small business can cause you to shoulder a lot of burdens, especially in the financial realm. Keeping track of revenues and expenditures to maintain a proper cash flow must be cautiously organized so that you are not off track on your funds or financialrecords when you are filing taxes.

We organize all of the trending information in your field so you don't have to. Join 52,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content