This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Processed accounts payable and receivable, ensuring timely payments and collections. Reconciled bank statements monthly, maintaining accurate financialrecords. Generated monthly financial reports, including profit and loss statements and balance sheets. Prepared and submitted payroll taxes accurately and on time.

Account management: They manage accounts payable and receivable, process invoices, reconcile accounts, and ensure timely payments and collections. Basic financial reporting: They generate basic financial reports, such as income statements and balance sheets, summarizing financial activity for a specific period.

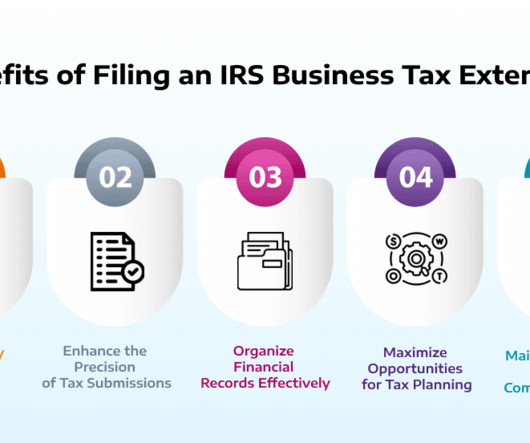

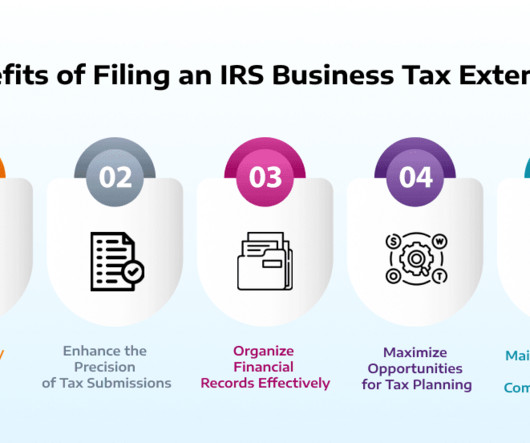

While its not an extension to pay taxes owed, it grants businesses the flexibility to organize their financialrecords. This extension offers invaluable support for companies managing complex financials or experiencing delays in gathering necessary documents. Alternatively, they could incur penalties and interest.

While its not an extension to pay taxes owed, it grants businesses the flexibility to organize their financialrecords. This extension offers invaluable support for companies managing complex financials or experiencing delays in gathering necessary documents. Alternatively, they could incur penalties and interest.

Take a look at this bookkeeping cleanup checklist to get all your financial ducks in a row. Collect all your financialrecords It’s hard to say which part of this process is the most difficult, but depending on the type of business you have, rounding up all your past financialrecords may be the most time-consuming.

Accounts receivable reconciliation is a crucial process within accounting and financial management practices undertaken regularly by a business. Reconciling accounts receivable involves comparing the balances in the accounts receivable ledger with supporting documentation, such as invoices, receipts, and customer payments.

The complexity of such fraud often requires detailed audits and advanced analytical tools to detect discrepancies in reported revenue versus actual collections. Plus, it allows you to collect receivables without identifying your bank account information to your customers.

Picture this: a team of expert bookkeepers diligently managing your financialrecords and transactions without setting foot in your office. These professionals play a crucial role in ensuring the accuracy and integrity of a company's financialrecords. Sounds futuristic?

The role of payment reconciliation in maintaining financial accuracy is critical, as it helps businesses track their income, verify the legitimacy of transactions and prevent discrepancies. Accurate financialrecords are essential for businesses to meet auditing requirements and avoid potential fines or penalties for non-compliance.

That’s because you have a moral and legal responsibility to protect your client’s financialrecords. Keep on Reconciling When a human is inserting information into the machine, there is a very high chance that an error might occur. Create Backup You can secure your data on QuickBooks by backing it up.

Below are some of the main benefits of implementing this automation into your workflow: Time Efficient Bookkeeping Manually logging into various banking platforms, downloading bank statements, and reconciling the transactions one by one, can quickly become very time-consuming. Bookkeepers are no strangers to this concept.

A Bank Reconciliation Statement is a financial document that ensures that the cash balances recorded in the internal financialrecords align with the financialrecords presented in the bank statement. General Ledger ) and the bank’s records (e.g. Bank Statement ).

As we approach the end of the year, it’s essential for small business owners to review their financialrecords and ensure everything is in order. Reconcile Bank Accounts Ensure your bank statements align with your accounting records. This step helps maintain accuracy in your financialrecords.

Gathering data over longer periods may require cross-collaboration with teams and even manual data collection. Make better credit decisions, lower DSO, and reconcile payments with near perfection. Automation eliminates the manual components behind the data collection process, making it more efficient. Lack of historic data.

Invest in accounting software or hire a professional bookkeeper to maintain organized and up-to-date records. Failure to Reconcile Bank Statements: Ignoring bank reconciliation is a recipe for disaster. Failing to reconcile your bank statements regularly can result in missed transactions, overdrafts, and errors in financial reporting.

Introduction to Bank Reconciliation Journal Entries Bank reconciliation is an important process in accounting that ensures the accuracy and integrity of a company's financialrecords. It involves the comparison between the company’s internal financialrecords and those of the bank.

In the world of finance and accounting, the process of reconciliation plays a vital role in ensuring accurate and transparent financialrecords. It is a crucial process for businesses to identify discrepancies, resolve errors, and maintain the integrity of their financial statements.

Expense reconciliation is a process within finance and accounting that ensures that a company's financialrecords accurately reflect its spending activities. At its core, it involves comparing financial data from various sources within a business to identify any discrepancies or errors and bring them into alignment.

Efficient reconciliation of payments is a vital aspect of financial management for businesses of all sizes. As transactions flow in and out, reconciling payments becomes crucial to ensure accuracy, identify discrepancies, and maintain a clear financial picture. Why is payment reconciliation crucial for businesses?

Need for Account Reconciliation Account Reconciliation ensures the accuracy and integrity of financialrecords by identifying discrepancies and errors, thus fostering trust among stakeholders and facilitating informed decision-making. Make Adjustments: Record missing transactions and correct errors for accurate balances.

This article highlights the importance of bank reconciliation, and its role in maintaining financial control, accountability, and protection against errors and fraud. Bank reconciliation involves comparing a company's internal financialrecords with those provided by the bank. What Is a Bank Reconciliation?

However, the rise in credit card usage has led to financial nightmares across accounting teams at the end of the month because this means the transactions that need to be reconciled are also on the rise. Credit card reconciliation involves matching credit card statements to internal financialrecords.

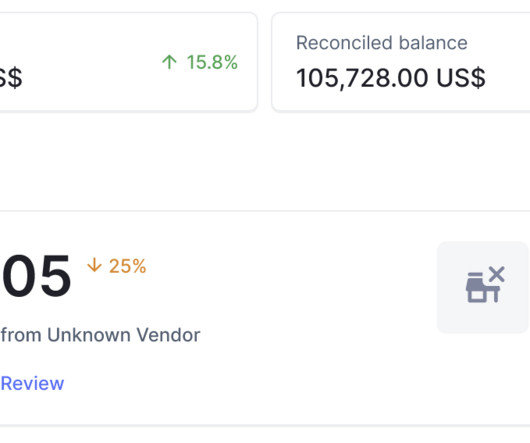

Through effective cash management practices, organizations can ensure the smooth functioning of their operations and uphold the trustworthiness of their financialrecords, making cash reconciliation a non-negotiable aspect of sound financial management. What is Cash Reconciliation? Category A Sales $503.00 -$3.00 Total $880.00

Maintaining accurate financialrecords is vital for any business, and the general ledger, as the central repository of financial transactions, plays a critical role in this process. The process may vary depending on the complexity of the organization and the specific accounts being reconciled.

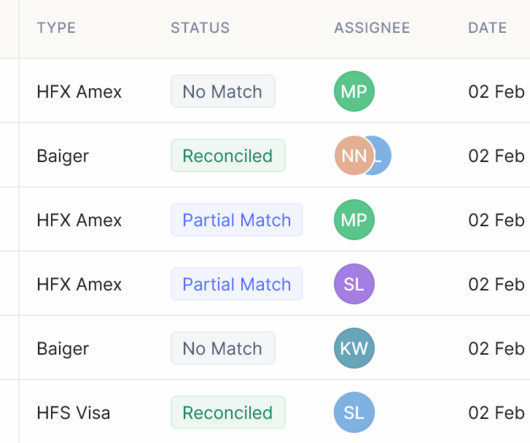

Integrate Nanonets Reconcilefinancial statements in minutes Try for Free What is Bank Reconciliation? Bank account reconciliation compares the financial data in a company's internal accounting books (e.g., Bank account reconciliation compares the financial data in a company's internal accounting books (e.g.,

Integrate Nanonets Reconcilefinancial statements in minutes Try for Free What is Accounts Reconciliation? At its core, account reconciliation is the comparison of multiple sets of financialrecords, such as bank statements and internal accounting records, to identify and rectify discrepancies.

From 1099 preparation services to year-end bookkeeping and full-year QuickBooks write-ups , ensuring your financialrecords are accurate and compliant can be daunting. To prepare for this process, ensure you collect a W-9 form from every eligible vendor. Service providers such as landscapers or cleaners.

Month-end close is a widely accepted accounting standard that is aimed at keeping an accurate set of financialrecords and detecting errors/fraud. It involves recording, reviewing, and reconcilingrecords at the end of every month. Month-end reconciliation is the most important part of the month-end close process.

Effective financial management is crucial for the success and growth of any business. One important aspect of financial management is invoice reconciliation. The primary goal of invoice reconciliation is to ensure that the financialrecords of a business are accurate, complete, and in alignment with the goods or services received.

With disconnected data sources and innumerable documentation, accounting teams can face the added task of figuring in interest rates, exchange rates, and timing differences to reconcile balances effectively. Account Reconciliation can be a fairly manual task, especially right before the monthly close. Retain all supporting documentation.

." Reconciliation in accounting refers to the comparing of details of transactions and financial activities between various documents. The vendor reconciliation process is the systematic procedure of verifying and aligning the financialrecords of a company with those of its vendors.

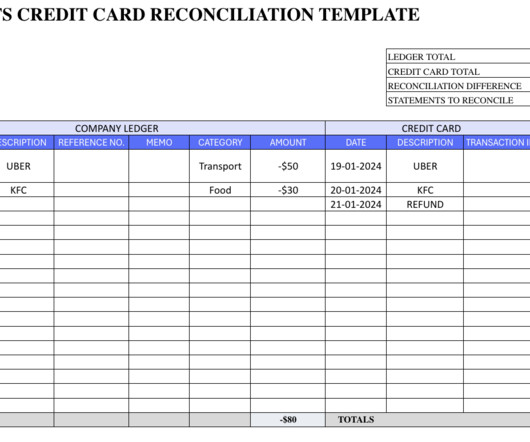

Our free Bank reconciliation template provides a simple way to reconcile your cashbook with your bank statement. Credit card reconciliation is the process of matching credit card records with your company ledger. Credit card reconciliation is the process of matching credit card records with your company ledger.

Petty cash reconciliation is the process of verifying and documenting petty cash transactions to ensure that the amount of cash on hand matches the recorded balance in the petty cash account. It serves as a control mechanism to maintain accurate financialrecords and prevent misuse or misappropriation of funds.

Related Courses Credit and Collection Guidebook Bookkeeping Guidebook Budgeting CFO Guidebook Cost Accounting Fundamentals New Controller Guidebook Payables Management Payroll Management Project Accounting Someone wanting to enter the accounting field can choose to train for a number of possible positions.

Balance sheet reconciliation is a critical process in finance and accounting that ensures the accuracy and integrity of financial statements. It involves comparing and reconciling the balances of various accounts in the balance sheet with supporting documentation. How to reconcile balance sheets?

Vendor Statement Reconciliation involves a meticulous comparison and alignment of a company’s financialrecords with those provided by its vendors. Step 4: Reconcile Payments and Outstanding Balances The reconciliation process extends beyond invoices and purchase orders to encompass payments and outstanding balances.

Payment reconciliation software tools are designed to automate and streamline the process of matching and reconcilingfinancial transactions within a business. Transaction Matching : Bank statement records are compared with entries in the accounting system, ensuring consistency in transaction dates, amounts, and descriptions.

The more financial systems it can connect with, the potential for more accurate financialrecords in real time. Make better credit decisions, lower DSO, and reconcile payments with near perfection. Its client payment portal offers seamless integration with collections, credit, cash application and disputes.

Consider whether the following reasons apply to your financialrecords. Data Entry Errors Data entry errors can happen if the user forgets to record a payment or enters it in the wrong column on the worksheet. Failure to communicate this to the A/R team could create a $5,000 discrepancy in accounting records.

Bookkeepers are generally in charge of the day-to-day tasks to maintain proper financialrecords. Collective Bookkeeping Collective helps you with multiple facets of your business, including registering and LLC formation. Bench Bookkeeping Bench Bookkeeping offers bookkeeping support starting at $299 per month.

The Top Credit Card Reconciliation Softwares in 2024 Credit card reconciliation is a crucial aspect of financial management for businesses of all sizes. It is the process of comparing and matching credit card transactions with corresponding spends and financialrecords to ensure accuracy and transparency in financial reporting.

The announcement of an actual audit can be overwhelming, prompting a scramble to locate important documents, reconcile accounts, and otherwise “get things together.” Are we collecting receivables in a way that smooths out cash flow? Which invoices are causing collection problems? Are our credit terms too loose or tight?

This includes documenting payment amounts, dates, and relevant details to maintain a comprehensive financialrecord. Bank Deposits: Depositing received funds into the appropriate bank accounts ensures liquidity and provides a clear trail for financial reconciliation.

It provides many benefits, including improved accuracy and efficiency in financialrecord keeping. Some advantages of using software for bookkeeping include the following: Reduces manual tasks, such as uploading bank transactions, sending invoices, and reconciling ledgers. Track, reconcile, and manage inventory.

We organize all of the trending information in your field so you don't have to. Join 52,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content