This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Connecting your systems directly: Reduces manual dataentry and errors Ensures automatic syncing of sales transactions Helps track platform-specific fees and commissions 3. Integrate Your Sales Platforms with Accounting Software Many accounting tools allow integration with multiple sales platforms.

Deposit Taxes Deposit payroll taxes and verify their transmission to the government. Review Reports If payroll calculations are either outsourced or use payroll software, print the following reports and review the underlying transactions for errors. Process payroll again until these issues have been corrected.

Balance sheet reconciliation is a critical financial process that aligns the financial statements with external documentation such as bank statements, invoices, and general ledger entries. These involve check-marking, the ability to adjust balances, and documenting any findings during the balance sheet reconciliation process.

A Bank Reconciliation Statement is a financial document that ensures that the cash balances recorded in the internal financial records align with the financial records presented in the bank statement. In effect, the reconciliation statement is a document that presents the comparison between the internal financial records of a company (e.g.

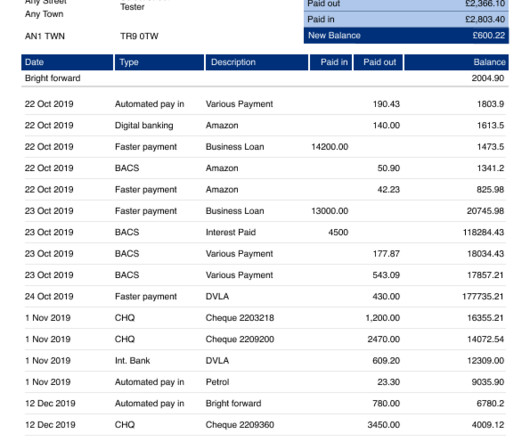

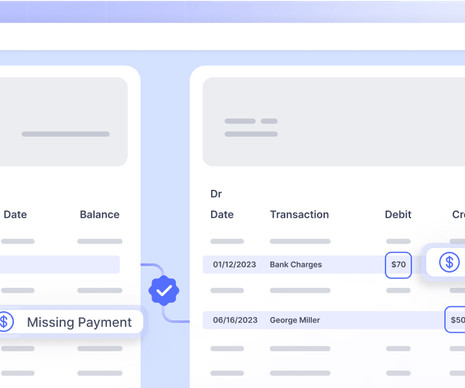

However, let's understand the manual bank reconciliation process once: Step 1: Gather documents On the bank side, you need the bank statements, outstanding checks, deposits, and any pending transactions. Match the deposits in the two statements. They have to be adjusted as shown in the next steps.

However, let's understand the manual bank reconciliation process once: Step 1: Gather documents On the bank side, you need the bank statements, outstanding checks, deposits, and any pending transactions. Match the deposits in the two statements. They have to be adjusted as shown in the next steps.

One method involves a thorough review of documents and transactions to verify their accuracy and consistency with bank statements. Adjusted Bank Balance: The ending balance adjusted for any outstanding deposits or withdrawals not yet recorded by the bank. Outstanding Checks: Checks issued by the company but not yet cleared by the bank.

This includes documenting payment amounts, dates, and relevant details to maintain a comprehensive financial record. Bank Deposits: Depositing received funds into the appropriate bank accounts ensures liquidity and provides a clear trail for financial reconciliation.

At the core of accounts management lies account reconciliation, the process of comparing various financial documents to ensure accuracy and accountability. Document Process: Maintain detailed records of steps, findings, and adjustments. Investigate Discrepancies: Analyze differences, trace transactions and rectify errors.

Book Reconciliation serves as the umbrella term, encompassing a broader spectrum of financial data matching that involves comparing the ledger entries with figures from other financial documents. Detecting Discrepancies: Bank reconciliation helps spot outstanding checks, deposits in transit, and bank errors.

However, the GL is not the sole repository of financial data. Businesses maintain a multitude of other financial documents, including bank statements, invoices , bills, cash payment receipts, and more. It ensures that all bank transactions, including deposits, withdrawals, and bank fees, are accurately recorded in the general ledger.

Read to learn more: Month-End Account Reconciliation Reconciliation is the process of matching the company’s general ledger with payments and deposits recorded in documents like bank statements, credit card statements, or invoices. Refunds: Bank transactions can be refunded, or your deposits can be withheld due to disputes.

Bank reconciliation is essential since it helps in the early detection of fraud, prevents financial statement errors during manual dataentry, and provides a clearer picture of the company's finances. Match the deposits in the two statements. Prevent fraud by flagging unrecorded transactions and prompt investigation.

Take, for instance, omnichannel call centers or document processing. They generate massive amounts of data that require efficient management. Dataentry: You can automate dataentry tasks with OCR and information extraction to greatly reduce the need for manual effort and improves accuracy.

💡 Bank statement verification is the process of confirming that the details in a bank statement—such as deposits, withdrawals, and balances—are accurate and authentic. The bank statement verification process involves several key steps to ensure the accuracy of the financial data provided.

This process typically involves reviewing transactions, invoices, receipts, and other financial documents to verify that they match up with the company's records and budget. Ensure that you have access to accurate and up-to-date financial data to facilitate the reconciliation process.

Here are some compelling reasons why businesses are embracing these tools: Enhanced Accuracy Manual dataentry and calculations are prone to human error. From dataentry to reconciliations, the hours spent on these repetitive tasks could be better utilized in more strategic areas of your business.

Matching and validating entries would mean data consolidation across sub-ledgers, vendor invoices, bank statements, receipts, and account receivables to ensure timely and accurate month-end and year-end closing of the financial books. Retain all supporting documentation.

An outstanding check is a payment yet to be cashed or deposited, remaining within the bank's clearing cycle. Leveraging sophisticated algorithms, reconciliation software ensures precise matching of transactions, including outstanding checks, deposits in transit, and bank fees.

PDF → Excel Convert PDF bank statements to Excel Try for Free A bank extract is data extracted from bank statements or other financial documents. These are official documents issued by a bank that provide detailed information on a customer's account transactions and balances.

Cleared Balance - This begins from the opening balance in the previous screen plus any finance charges added, along with all cleared deposits minus cleared payments. Here are some tips to make it easier for you: Sort by transaction type: Begin by matching deposits and then payments. This organization can reduce confusion.

General ledger reconciliation is a fundamental accounting practice that verifies the consistency and accuracy of account balances, identifies discrepancies, and ensures the financial data aligns with the underlying transactions. These documents will serve as a basis for comparing and reconciling the account balances in the general ledger.

Solution: Invoicing software generates accurate invoices quickly, reducing human error and the time spent on manual dataentry. It is time to forget about the numerous documents, and reports and switch between multiple applications. Challenge 2: Manual Billing Manually creating invoices can be error-prone and time-intensive.

From forging bank statements in job and loan applications to issuing fake bank statements for visa processing and insurance claims, these fake documents seriously threaten individuals, businesses, and financial institutions. Fake bank statements Fake bank statements are fraudulent documents designed to look like genuine bank statements.

Stripe directly fetches this data through Financial Connections on a daily basis, ensuring alignment between Stripe's records and actual bank deposits. It helps to document these protocols and ensure adherence across the organizational spectrum. How to Set up Stripe Reconciliation?

Unlike traditional paper-based invoicing systems, e-invoicing automates the invoicing process, eliminating the need for physical paperwork and manual dataentry. Instead, they can view cloud-stored data at any time to gain insights on invoice and payment status. 2.

It’s not like a traditional bank account where you deposit money but instead more of a relationship with a merchant account provider that serves as a bridge between your customer’s credit account and your business bank account. In total, the time from payment to deposit is about 1-2 days with a merchant account.

PDF → Excel Convert PDF bank statements to Excel Try for Free The digitization of financial documents is an important task for financial institutions like banks as well as individual banking customers and businesses. Check our Nanonets workflow-based document processing software. Want to automate repetitive manual tasks?

Bank Fees for Returned Checks : If the bank charges fees for returned checks, a journal entry is made to recognize this expense and reduce the Cash account. Common discrepancies include outstanding checks, deposits in transit, bank fees, interest earned, or errors in recording transactions.

It also includes various other steps such as underwriting , documentation, and funding. The Origination in finance is often a lengthy process and it's overseen by the Federal Deposit Insurance Corporation (FDIC) for compliance with Title XIV of the Dodd-Frank Wall Street Reform and Consumer Protection Act.

Time-consuming Traditional accounting methods involve time-consuming tasks such as dataentry, calculations, and reconciliations. Incorrect dataentries and data omissions can lead to inaccurate financial records. Limited real-time insights Financial data compiled and analyzed manually often becomes outdated.

Account reconciliation is the process of comparing general ledger accounts (usually from the balance sheet) with supporting documents, such as bank statements, sub-ledgers, and other underlying transaction details. What is Account Reconciliation? Furthermore, not all reconciling items necessitate adjustments to the balance.

This essential practice involves comparing transactions and other financial activities with supporting documentation and resolving any discrepancies that may arise. This comparison allows for the verification of data accuracy within the business's records.

Payment reconciliation refers to the process of comparing and matching financial data from different sources to ensure accuracy and consistency in the recorded transactions. It involves cross-checking payment records, such as invoices, receipts, bank statements, and other financial documents, to reconcile any discrepancies between them.

Key aspects of bank statement analysis Transaction categorization: Classify entries as deposits, withdrawals, transfers, payments, etc. Bank reconciliation Compare bank statement data with internal records to ensure every transaction is accounted for properly.

Inaccuracies in Expense Reporting Manual DataEntry Errors Mistakes in receipts and expense reports due to human error. Regulatory Compliance Risks Inadequate Documentation Failing to meet the detailed documentation requirements set by tax authorities. This helps in maintaining a checks and balances system.

Data extraction Key bank statement fields Data extraction tools automatically extract pertinent information from bank statements using machine learning-enhanced optical character recognition (OCR) technology. Reconciliation This step involves matching the extracted data with the company’s internal records.

Expense management software automates and digitizes the expense reporting process, eliminating the need for manual dataentry and paper-based receipts. Flow by Nanonets Nanonets is an AI-based expense management software that offers automated data capture for intelligent processing of expenses. Transparent pricing policy.

Flow by Nanonets Flow stands out as the best software for spend management due to its powerful AI-based data extraction platform and a range of advanced features designed to optimize expense control workflows. Flow Automated expense recognition and classification, reducing manual dataentry and GL coding efforts.

However, the clunky spreadsheet, hours of manual dataentry, and paper receipts can be avoided. If you have made them, you know how dreadful it is to manage and process those reports at the end of the month, what we call “closing of the month”, which are actually days of painful dataentry and errors.

Documenting transactions in receipt books ensures accuracy in financial management, compliance with tax regulations, and the ability to resolve discrepancies with ease. Understanding Receipt Books A receipt book is essentially a book of pre-printed forms designed to document transactions between a seller and a buyer.

Manual data leads to errors and wastes valuable time & human resources. A mountain of receipts, hours spent in manual dataentry, and the inevitable human error that creeps in - It's a recipe for financial disaster. Generating meaningful insights from expense data is essential for informed decision-making.

Historically, banks have been intermediaries – a trusted financial entity who could translate excess deposits into loans, translate currencies, and become a trusted party between two unknown parties. By automating a manual process, companies can get more out of their employees and have them focus on high-level tasks instead of dataentry.

Payment Options : You can provide your customers with multiple payment methods, such as accepting online payments via integrating Stripe, EMI payments, accepting deposits, and customizing payment timelines. Expense Tracking : Prepare and dispatch high-quality invoices and quote documents to the clients within a few minutes.

We organize all of the trending information in your field so you don't have to. Join 52,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content