This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Bookkeepers ensure these buckets are properly categorized and meticulously record every deposit and withdrawal. This ongoing process provides a clear picture of a company’s financial health at any given time. Regulatory bodies may use them to ensure companies comply with financialreporting standards.

However, simply recording transactions in the general ledger is not sufficient to ensure accurate financialreporting. Ensure Financial Accuracy: Reconciling the general ledger helps ensure that the recorded account balances accurately reflect the actual financial transactions.

In effect, the reconciliation statement is a document that presents the comparison between the internal financial records of a company (e.g. It typically outlines outstanding checks, deposits in transit, bank fees, errors, and any other differences between the two sets of records. Bank Statement ).

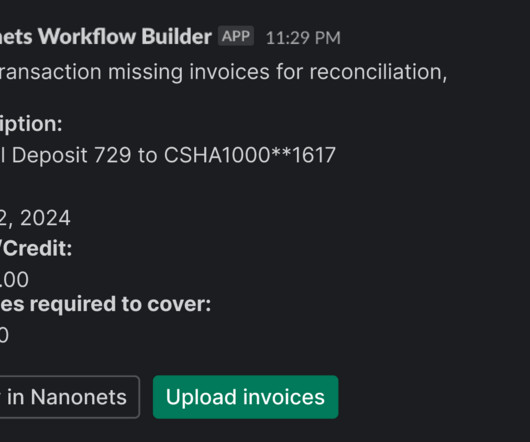

By doing regular balance sheet reconciliations, financial teams can address fraudulent activity, detect errors, and resolve discrepancies promptly. Accurate and timely financialreporting is important in maintaining trust with stakeholders and making informed business decisions. We note this to be $21,500 as of 5/31/2024.

This means no more: Manual dataentry into a computer. Producing financialreports in a spreadsheet. Because automation runs with the click of a button compared to someone having to key in financial information entry manually, you can speed up the turnaround time of your deliverables and financialreporting.

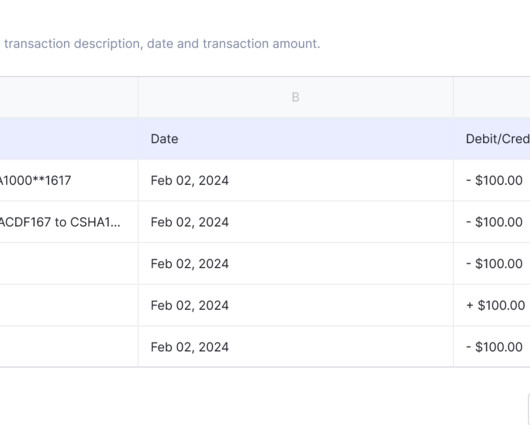

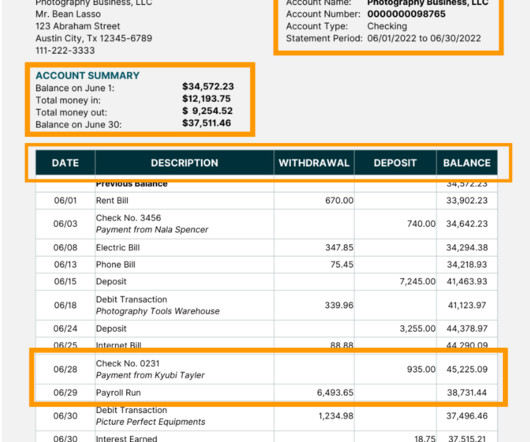

Reconciling the bank statement involves comparing the company's internal financial records or ledger to the bank statement received via the bank. Bank reconciliation can help ensure the company's accurate financialreporting when done regularly. Match the deposits in the two statements.

This serves as a safeguard against errors or potential fraudulent activities before the company finalizes its financialreports. Identifying and Investigating Discrepancies: Searching for missing deposits or unauthorized charges, and contacting the bank if needed.

However, let's understand the manual bank reconciliation process once: Step 1: Gather documents On the bank side, you need the bank statements, outstanding checks, deposits, and any pending transactions. Match the deposits in the two statements. They have to be adjusted as shown in the next steps.

However, let's understand the manual bank reconciliation process once: Step 1: Gather documents On the bank side, you need the bank statements, outstanding checks, deposits, and any pending transactions. Match the deposits in the two statements. They have to be adjusted as shown in the next steps.

Here are some compelling reasons why businesses are embracing these tools: Enhanced Accuracy Manual dataentry and calculations are prone to human error. One misplaced digit could lead to miscalculations, resulting in financial discrepancies that could harm your business. Customers can conveniently view and pay invoices online.

Understanding the intricacies of bank reconciliation journal entries is essential for finance professionals and business owners alike, as it empowers them to identify, address, and prevent errors or discrepancies in financialreporting. Date Account Debited Account Credited Amount 12/21/23 Bank Charges Expense Cash $1000.00

This includes documenting payment amounts, dates, and relevant details to maintain a comprehensive financial record. Bank Deposits: Depositing received funds into the appropriate bank accounts ensures liquidity and provides a clear trail for financial reconciliation.

It ensures that all bank transactions, including deposits, withdrawals, and bank fees, are accurately recorded in the general ledger. It helps in identifying any discrepancies such as stock shortages, overages, or valuation errors that may impact the accuracy of financialreporting.

It’s a crucial step to ensure that you prepare an accurate set of statements for financialreporting, planning, and tax compliance. Data-collection: You must collect your financial documents like general ledger, balance sheet, bank statements, invoices, receipts, etc. This can lead to a date mismatch.

Here are some common ones: DataEntry Errors : Human errors during dataentry can lead to discrepancies between internal records and external sources. Unrecorded Transactions : Failure to record all transactions, such as outstanding checks or pending deposits, can lead to discrepancies in reconciled accounts.

Bank Reconciliation : Bank reconciliation involves matching transactions recorded in the company's general ledger with those listed on the bank statement to verify all the transactions processed by the bank, including deposits, withdrawals, checks, and bank fees. The company follows up on these descrepancies.

Whether it's ensuring that expenses align with available funds or guaranteeing that business transactions accurately reflect the company's financial standing, tracking checks outstanding and reconciling bank statements is non-negotiable. Looking out for a Reconciliation Software?

Time-consuming Traditional accounting methods involve time-consuming tasks such as dataentry, calculations, and reconciliations. Incorrect dataentries and data omissions can lead to inaccurate financial records. Prone to errors Manual accounting is highly susceptible to human error.

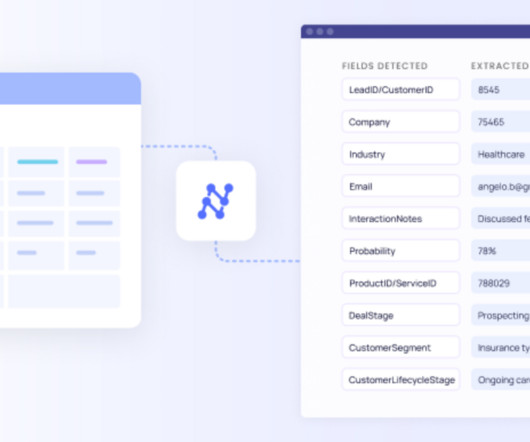

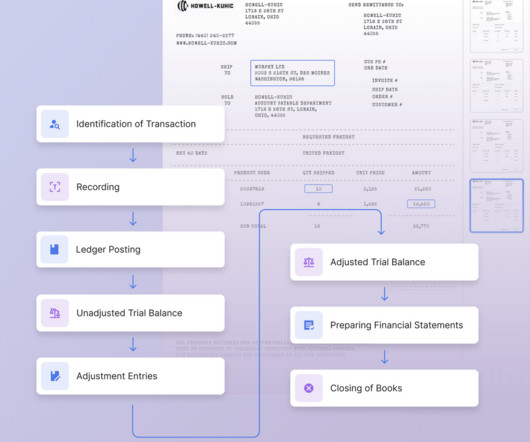

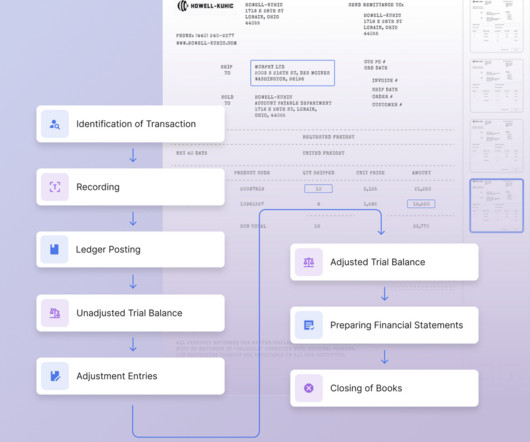

Integrate Nanonets Reconcile financial statements in minutes Explore for Free Types of Account Reconciliation This guide will help you understand the different sub-groups of account reconciliation activities organizations encounter. Account reconciliation is essential to ensuring the accuracy and integrity of financialreporting.

The extracted data is then sent for bank statement analysis , further processing, and accounting. Bank statement processing is essential for accurate reconciliation , auditing, and financialreporting. Reconciliation This step involves matching the extracted data with the company’s internal records.

Compliance and Regulation : Expense reconciliation is crucial for compliance with financial regulations and standards. Many industries are subject to regulatory requirements regarding financialreporting and transparency. Fraud Prevention: Expense reconciliation plays a critical role in fraud prevention.

It typically includes information such as deposit and withdrawal transactions, account balances, and any fees or charges. By automating the extraction of information from bank statements, individuals and businesses can save time and reduce errors that can occur from manual dataentry.

They bring a bunch of perks: making the process smoother, saving time and cash, and boosting financial oversight. Here’s why they’re essential: Efficiency and Accuracy: Expense management tools automate many aspects of the process, reducing the need for manual dataentry and the risk of human errors.

Accurate financial records are essential for businesses to meet auditing requirements and avoid potential fines or penalties for non-compliance. By having a systematic process in place for reconciling payments, business users can ensure that all transactions are recorded properly and that financialreports are reliable.

Additionally, for checks deposited into the bank, there might be a delay before they are reflected in the bank statement. This helps safeguard the company's assets and mitigate financial risks. Such payments usually involve cash transactions that haven't been captured by the bank yet.

It's like putting your financial transactions under a microscope better to understand your business's financial health and activities. Key aspects of bank statement analysis Transaction categorization: Classify entries as deposits, withdrawals, transfers, payments, etc.

For example, timing differences, such as outstanding checks deducted from a payer's GL cash balance but not yet deposited into the recipient's bank, can cause the bank balance to appear higher than the GL balance. Furthermore, not all reconciling items necessitate adjustments to the balance.

Challenges In Traditional Expense Tracking Methods Traditional methods of expense tracking often involve manual processes, like paper receipts and spreadsheets, leading to several challenges: Errors and Inaccuracies: Manual dataentry can result in mistakes and inaccuracies, leading to discrepancies.

By reconciling payments, businesses can provide evidence of their financial transactions, ensuring adherence to financialreporting standards and fulfilling regulatory obligations. This reconciliation ensures that all payments, deposits, fees, and charges recorded by the business align with the bank's records.

They bring a bunch of perks: making the process smoother, saving time and cash, and boosting financial oversight. Here’s why they’re essential: Efficiency and Accuracy: Financial management tools automate many aspects of the process, reducing the need for manual dataentry and the risk of human errors.

Manual data leads to errors and wastes valuable time & human resources. A mountain of receipts, hours spent in manual dataentry, and the inevitable human error that creeps in - It's a recipe for financial disaster. This is where the financial rubber meets the road.

If the payment is for something else, such as a security deposit, check the other box and write a description. Utilizing AI, it delves into the context of your receipts, understanding the nuances of your financial transactions. Step 3: Payment Details Check the appropriate box to indicate that the payment is for rent.

We organize all of the trending information in your field so you don't have to. Join 52,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content