This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The accountant takes that raw data and transforms it into a meaningful story. Accountants analyze the information recorded by the bookkeeper. They use this data to prepare financialstatements, such as income statements, balance sheets, and cash flow statements.

Reducing Errors Through Automated DataEntry Receipt Scanning : Utilises Optical Character Recognition (OCR) technology to automatically capture information from receipts, such as the date, amount, and vendor. Time Efficiency : Reduces the time spent on manual dataentry, freeing up resources for strategic initiatives.

These standards align with international financial reporting norms, ensuring consistency and transparency in financialstatements. Real-time financial reporting ensures businesses stay compliant without manual intervention. Reduces errors in financialstatements, improving audit readiness.

Gone are the days of tedious manual dataentry and stacks of paper ledgers. Businesses are now embracing the virtual to streamline their financial management processes. Picture this: a team of expert bookkeepers diligently managing your financialrecords and transactions without setting foot in your office.

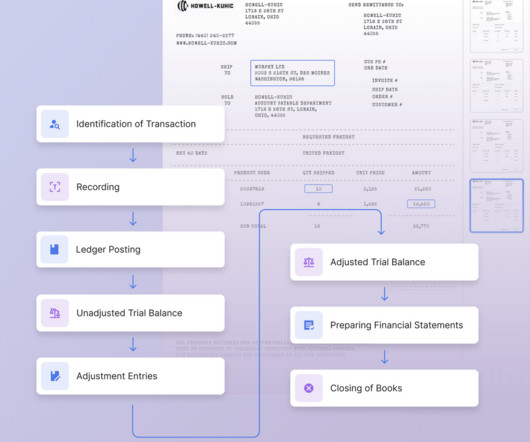

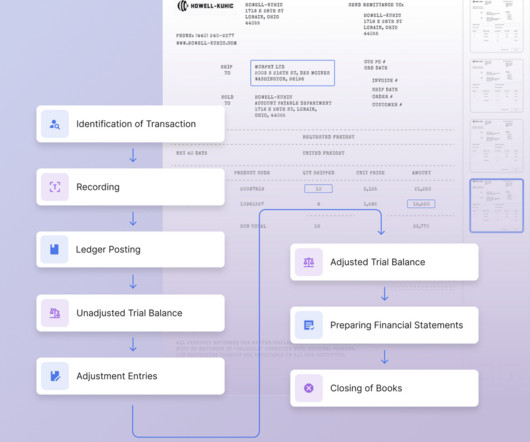

The end of month close process plays a vital role in ensuring the accuracy, integrity, and transparency of financialrecords for businesses of all sizes. Its primary purpose is to ensure the accuracy and completeness of financialrecords so that financialstatements can be prepared for internal and external reporting purposes.

A Certified Public Accountant is an accounting professional who performs tasks such as auditing books or analyzing financialstatements. CPAs work closely with clients to review financialstatements and perform audits to ensure compliance. What Is a CPA? Are CPA Jobs in Demand?

Artificial intelligence (AI) can perform various tasks related to accounting, such as dataentry, analysis, and report generation. However, these tasks can be time-consuming and prone to errors, which can result in delayed payments, inaccurate financial reporting, and, ultimately, negative impacts on the company’s bottom line.

Even though a CPA may comprehend the value of keeping precise financialrecords, guaranteeing compliance with tax rules can be a difficult undertaking. CPAs can assign work such as bank reconciliations, financialstatement creation, and dataentry to a group of qualified experts by using bookkeeping services.

Proper bookkeeping basics practices ensure accurate financialrecording, allowing you to make informed decisions and comply with legal and tax requirements. Double-entry bookkeeping : This principle states that every financial transaction should be recorded in at least two accounts, with equal debits and credits.

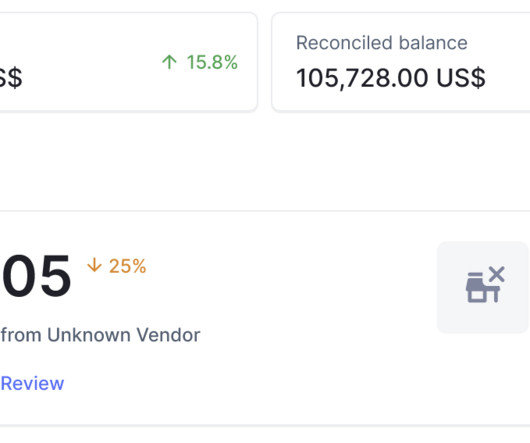

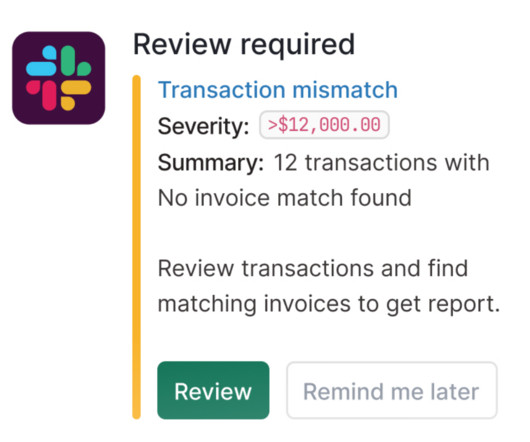

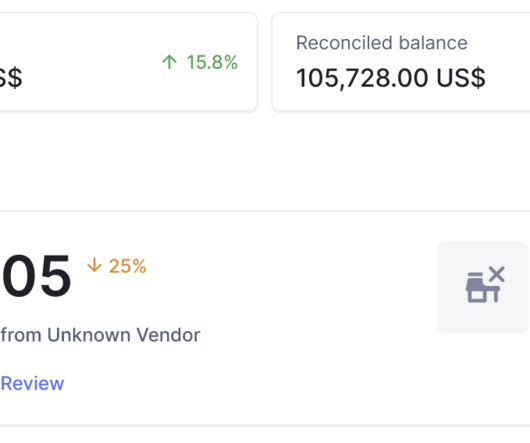

This guide aims to navigate you through the process of undoing a reconciliation in QuickBooks Online, ensuring your financialrecords remain accurate and reflective of your current financial status. Integrate Nanonets Reconcile financialstatements in minutes Try for Free Why is reconciliation needed in QuickBooks Online?

A Bank Reconciliation Statement is a financial document that ensures that the cash balances recorded in the internal financialrecords align with the financialrecords presented in the bank statement. General Ledger ) and the bank’s records (e.g. Bank Statement ).

Bookkeeping is a critical function for any small business aiming for financial stability and sustainable growth. Accurate financialrecords provide essential insights into cash flow, profitability, and overall business health. Here’s a deeper look at when to handle bookkeeping on your own and when to bring in a professional.

Balance sheet reconciliation is a critical process in finance and accounting that ensures the accuracy and integrity of financialstatements. Balance sheet reconciliation is an essential accounting practice that verifies the accuracy and consistency of financialstatements. What is Balance Sheet Reconciliation?

Best Reconciliation Software Tools Reconciliation software is a tool specifically designed to compare financialdata from different sources such as invoices, bank statements, general ledgers, and other financialrecords. This eliminates the need for manual dataentry , which can save time and reduce errors.

Automated Accounts Reconciliation software like Nanonets can cohesively consolidate all data sources on one platform, automate the matching logic across external data sources and general ledgers, effectively provide an audit trail, and keep the process transparent for the accounting team personnel involved.

You’re not maintaining accurate financialrecords It’s imperative to maintain organised financialrecords, not just to remain in compliance with the IRAS and financial auditors, but also to present a comprehensive view of your company’s financial position to potential investors.

You’re not maintaining accurate financialrecords It’s imperative to maintain organised financialrecords, not just to remain in compliance with the IRAS and financial auditors, but also to present a comprehensive view of your company’s financial position to potential investors.

By implementing the right strategies and utilizing modern technologies, businesses can overcome these accounting hurdles and ensure a smoother financial flow. These errors can have a significant impact on financialstatements, leading to incorrect financial analysis and decision-making.

A balance sheet is a financialstatement that provides a snapshot of a company's financial position at a specific point in time. Balance sheet reconciliation is a critical financial process that aligns the financialstatements with external documentation such as bank statements, invoices, and general ledger entries.

Petty cash reconciliation is the process of verifying and documenting petty cash transactions to ensure that the amount of cash on hand matches the recorded balance in the petty cash account. It serves as a control mechanism to maintain accurate financialrecords and prevent misuse or misappropriation of funds.

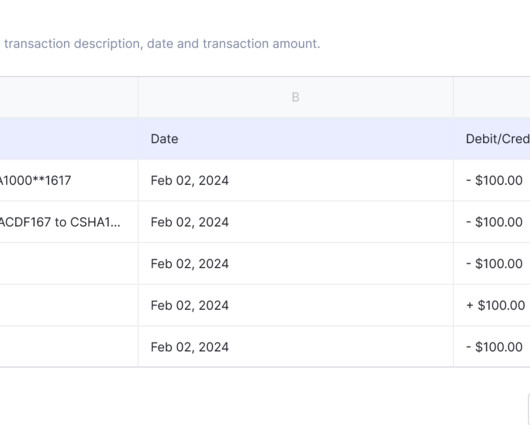

Introduction to Bank Reconciliation Journal Entries Bank reconciliation is an important process in accounting that ensures the accuracy and integrity of a company's financialrecords. It involves the comparison between the company’s internal financialrecords and those of the bank.

Expense reconciliation is a process within finance and accounting that ensures that a company's financialrecords accurately reflect its spending activities. At its core, it involves comparing financialdata from various sources within a business to identify any discrepancies or errors and bring them into alignment.

Finance reconciliation plays a pivotal role in ensuring the reliability and accuracy of a business's financialrecords. This essential practice involves comparing transactions and other financial activities with supporting documentation and resolving any discrepancies that may arise. What is finance reconciliation?

Bookkeeping is an essential part of managing any business and staying on top of your financialrecords can make or break your success. This can lead to stress and bigger financial issues down the road. Keeping accurate records is crucial to securing financing. This could lead to audits, fines, or even legal action.

Throughout the reconciliation process, attention to detail, accuracy, and adherence to accounting principles are paramount to ensure the integrity and reliability of the company's financialrecords. This integration facilitates data exchange, improves data accuracy, and eliminates manual dataentry errors.

To Ensure Accurate Records of a Business's Finances A well-prepared AP audit report offers insights into the organization's performance and highlights areas for improvement. To ensure accuracy in financialstatements, auditors conduct accounts payable audit procedures. Can Accounts Payable Audit be Automated?

Accurate financialrecords are essential for businesses to meet auditing requirements and avoid potential fines or penalties for non-compliance. By having a systematic process in place for reconciling payments, business users can ensure that all transactions are recorded properly and that financial reports are reliable.

This article highlights the importance of bank reconciliation, and its role in maintaining financial control, accountability, and protection against errors and fraud. Bank reconciliation involves comparing a company's internal financialrecords with those provided by the bank. What Is a Bank Reconciliation?

Streamlined Bookkeeping Bookkeeping encompasses various tasks, including chart of accounts preparation, dataentry, and financialstatement management. These professionals possess the specialized knowledge and experience essential for maintaining efficient bookkeeping processes.

Accounts receivable reconciliation is a fundamental accounting process that involves comparing and verifying the balances in the accounts receivable ledger against supporting documentation and external records. Any discrepancies found are investigated and resolved to maintain the integrity of the financialrecords.

That’s because the credit and debit entries should balance each other out. Consider whether the following reasons apply to your financialrecords. DataEntry Errors Dataentry errors can happen if the user forgets to record a payment or enters it in the wrong column on the worksheet.

Scaling traditional underwriting operations becomes increasingly challenging as underwriters spend a significant amount of time gathering and verifying data from multiple sources. These include customer applications, financialrecords, medical reports, and external risk assessments such as geographic or weather-related data.

Maintaining accurate financialrecords is vital for any business, and the general ledger, as the central repository of financial transactions, plays a critical role in this process. Regular and timely reconciliation is essential to maintain accurate financial information and support informed decision-making.

Integrate Nanonets Reconcile financialstatements in minutes Try for Free What are Outstanding Checks? It poses a liability for the issuer until reconciled with financialrecords, potentially leading to overdraft risks if funds aren't maintained.

In this blog, we'll delve into what invoice audits entail and why they are crucial for the financial integrity of businesses. An Account Payable Audit is a process by which the financialrecords of the accounts payable department are examined by an auditor. What is an Accounts Payable Audit?

It’s the light guiding the way to financial clarity. By aligning and verifying financialrecords, expense reconciliation brings order to chaos, giving a clear view of a company’s financial health. It ensures audit-ready financialstatements, saving time and potential penalties during audits.

Reconciling the bank statement involves comparing the company's internal financialrecords or ledger to the bank statement received via the bank. Key takeaways: Bank reconciliation is the transaction matching of your records against the bank statement.

." Reconciliation in accounting refers to the comparing of details of transactions and financial activities between various documents. The vendor reconciliation process is the systematic procedure of verifying and aligning the financialrecords of a company with those of its vendors.

Seek seamless integration, automated dataentry, accurate sales tax tracking, and comprehensive financial reporting features. With these capabilities, you will efficiently manage finances, save time, comply with tax regulations, and gain valuable insights into your online business’s financial health.

Book Reconciliation entails the comparison of different types of financialrecords of a company. These records may be internal financialrecords or external. Companies maintain various internal records to track their financial activities accurately and ensure compliance with accounting standards.

Reconciling payments involves verifying whether the payments received in the company's bank account match the corresponding invoices or payment records in the company's financial system. It ensures accuracy, financial integrity, fraud detection, compliance, efficient cash flow management, and informed decision-making.

How do I keep proper records? What are financialstatements, and how do I get them? Bookkeeping is the process of keeping financialrecords for your business. A single-person small business can get away with keeping written financialrecords in a notebook but large businesses need detailed entries.

The aim is to ensure all transactions are accurately recorded in the company's cashbooks and to find any errors or fraud. Reconciliation includes matching the company’s balance sheet, income statement, bank statements, and expenses. Filing tax returns requires an accurate record, or you can incur penalties.

The aim is to ensure all transactions are accurately recorded in the company's cashbooks and to find any errors or fraud. Reconciliation includes matching the company’s balance sheet, income statement, bank statements, and expenses. Filing tax returns requires an accurate record, or you can incur penalties.

We organize all of the trending information in your field so you don't have to. Join 52,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content