This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Payments are reconciled automatically, your ERP is updated with the new payment data, and the customer receives payment confirmation within a few minutes. But many don’t consider it a problem until the receivables are “very” late (a different definition at every company, but usually an invoice reaches this definition at around 60 days).

What is a Reconciling Item? A reconciling item is a difference between balances from two sources that are being compared. These items are stated in an account reconciliation , so that the balance from one source is adjusted by reconciling items to arrive at the balance from the other source.

Why is it Important to Reconcile your Bank Account? Reconciling the bank statement involves comparing the company's internal financial records or ledger to the bank statement received via the bank. How Often Should You Reconcile Your Bank Statements? They can benefit by reconciling their bank statements monthly.

How to Use a Cash Voucher The petty cash custodian uses the cash voucher to reconcile the petty cash fund. If they are prenumbered, then a common control is to track these numbers, to ensure that no vouchers were used but not stored in the petty cash box.

Reconcile the differences between the two columns. Related Articles Bank Reconciliation Procedure How to Reconcile a Bank Statement Reasons Why the Bank Balance Differs from the Book Balance The Bank Reconciliation Process The Purpose of a Bank Reconciliation Sign and date the form, and submit to a supervisor for review.

The report may also be used as part of the bank reconciliation process, to determine which issued checks have not yet cleared the bank, and so are reconciling items. The report is used to determine the exact payments included in a check run; as such, it is considered a necessary part of the accounts payable process.

Related Articles Accounts Payable Analysis Accounts Payable Controls How to Reconcile Accounts Payable How to Set Up an Accounts Payable System Voucher System Also, vouchers are not used in the payroll process. In the payroll process, payments are made based on an approved timesheet or timecard.

To avoid this potentially large write-off, track all deferred asset items on a spreadsheet, reconcile the amounts on the spreadsheet to the account balance listed in the general ledger at the end of each reporting period, and adjust the account balance (usually with a periodic charge to expense) as necessary.

Related Articles Basic Accounting Concepts Books of Original Entry Cleaning Up Messy Books Double Entry Accounting How to Reconcile the General Ledger The Steps in the Accounting Process Terms Similar to Ledger Account A ledger account is also known as an account.

Deferred Revenue While both terms involve timing differences between revenue recognition and cash flow, they are opposites: Deferred Revenue (Unearned Revenue): Definition : Cash is received upfront for goods or services yet to be delivered. Accrued Revenue: Definition : Revenue is earned but not yet billed or collected.

If this occurs at month-end, the deposit will not appear in the bank statement, and so becomes a reconciling item in the bank reconciliation. If it has not yet cleared the bank by the end of the month, it does not appear on the month-end bank statement, and so is a reconciling item in the month-end bank reconciliation. NSF check.

Related Articles Account Analysis Account Reconciliation Books of Original Entry Final Accounts How to Reconcile an Account The Aging of Accounts An offsetting entry was recorded prior to the entry it was intended to offset.

Thus, if a controller were to illegally withdraw $10,000 from the company accounts near the beginning of the month for his personal use and replaced the funds before the end of the month, the issue would not appear in a normal bank reconciliation as a reconciling item.

Responsibilities of a Full Charge Bookkeeper The subject areas over which the full charge bookkeeper has responsibility are as follows: Record and pay accounts payable Issue invoices to and collect from customers Calculate pay and issue payments to employees Create financial statements and related financial reports Remit payroll taxes , sales taxes (..)

Related Articles Accounting for Accounts Payable Clean the Vendor Master File How to Reconcile Accounts Payable How to Set Up an Accounts Payable System Scrubbing Accounts Payable The Net Method of Recording Accounts Payable These automated systems are so expensive that they are not a viable solution for smaller businesses.

Dealing with Confirmation Variances If the information received from a customer varies from the receivable amount listed in the company's receivable report, the auditor usually asks the company to reconcile the difference, which the auditor can then take further action on, as necessary. Related Articles Accounts Receivable Auditing

Related Articles How to Reconcile Inventory Inventory Control An active cycle counting program will at least improve the accuracy level of the inventory records, and may even make it unnecessary to conduct a month-end physical inventory count.

Adjustments to general ledger accounts that have been reconciled as part of the closing process. Some smaller businesses do not bother to recognize depreciation and amortization on a monthly basis, choosing to instead do so just once, at the end of the year.

Related Articles Account Analysis Accounting Adjustments Accounting System Design Accounts Reconciliation (podcast) How to Reconcile an Account When an Accounting Error is Material If so, the liability suspense account is classified as a current liability.

Another control is to reconcile the balances in accounts to the supporting source documents to see if either some documents have not been recorded, or if some transactions recorded in the accounts do not appear to have any supporting source documents.

This schedule is used by the accounting staff to reconcile the balance in the deferred charges account at the end of each accounting period, and to ensure that all required amortization has been completed. Accounting for Deferred Charges Deferred charges should be itemized on a schedule that states the remaining balance of each item.

Some of the common customizations that you should definitely try are – Layout Modification – If you are comfortable using older versions of QuickBooks, you can easily go back to your desired version of QuickBooks by following the steps – Click on View > Top Icon Bar > Click on Edit > Preferences > Desktop View.

Are cash accounts being reconciled? Have checks written but not mailed been classified as liabilities? Is there a reconciliation of intercompany transfers? Receivables. Is there an adequate allowance for doubtful accounts ?

As part of the closing process, the accounting staff may engage in the following reconciliation activities: Reconcile the bank statement Reconcile balance sheet accounts to the supporting detail Reconcile inventory records to on-hand balances (if a periodic inventory system is used) Reconciliations are considered an important control activity.

If the payment portal is connected to a cash application tool, it will be reconciled automatically. The post B2B Customer Payment Portal: Definition, Types & Process appeared first on Gaviti. Once the payment is made, the payment will go automatically to your bank account or other destination of choice.

If they match, it means your records and the bank statement are reconciled, and there are no discrepancies. Why is it important to reconcile your bank statements? It's important to reconcile bank statements to identify errors, detect fraud, and maintain an accurate ledger. How do you reconcile a bank statement?

With this added time, businesses can verify their financial information, reconcile discrepancies, and identify all eligible deductions. Yes definitely, extension of IRS business tax only extends the filing deadline. The time gained through a business tax extension allows for meticulous preparation.

Related Articles How to Reconcile Inventory How to Reduce Inventory Just-in-Time Inventory Control Stock Control Terms Similar to Inventory Control Inventory control is also known as stock control.

With this added time, businesses can verify their financial information, reconcile discrepancies, and identify all eligible deductions. Yes definitely, extension of IRS business tax only extends the filing deadline. The time gained through a business tax extension allows for meticulous preparation.

Reconcile the agreed amount of transactions by the agreed timeframe. These definitions are crucial to success in starting a bookkeeping business. . The “pricing and services” section describes what’s included in the mandate and the definition of what’s included can be found in the Service Terms section.

A business will make adjusting entries to its own cash book balance to reconcile the difference between its own balance and the balance per bank. Balance per bank is the ending cash balance appearing on a bank statement. Examples of these adjustments are to record the fees for check processing and bank overdrafts.

A reconciliation statement is a document that begins with a company's own record of an account balance , adds and subtracts reconciling items in a set of additional columns, and then uses these adjustments to arrive at the record of the same account held by a third party. Debt accounts.

All outstanding deposits are listed as reconciling items on the periodic bank reconciliation prepared by the receiving entity. Deposits are typically only outstanding for one business day, so there tend to be few of these deposits listed as reconciling items whenever a bank reconciliation is prepared.

Related AccountingTools Courses Bank Reconciliation Essentials Corporate Cash Management How to Audit Cash Related Articles Bank Charge Debit Memo How to Reconcile a Bank Statement Memo Debit If you are not sure about the nature of a debit, contact your bank for an explanation.

In this blog, you will learn about cross-border payments including its history, definition and the benefits it can provide organizations. AP staff would have to enter payments into multiple systems, account for changes in exchange rates and manually reconcile invoice and payment amounts, which is inefficient and time-consuming.

Examples of Reconciling an Account A company controller wants to reconcile all balance sheet accounts at the end of the year, so that their ending balances can be justified to the auditors. Account reconciliations are also useful for spotting instances of inappropriate purchases.

Related Articles Accounting for Accounts Payable How to Reconcile Accounts Payable How to Record Invoices with No Invoice Number How to Set Up an Accounts Payable System Scrubbing Accounts Payable Once this voucher is approved, the disbursement system is authorized to issue payment.

Fourth, regularly reconcile not only the bank account, but all significant asset and liability accounts, to ensure that they only contain valid transactions; all other items should be recognized through the income statement.

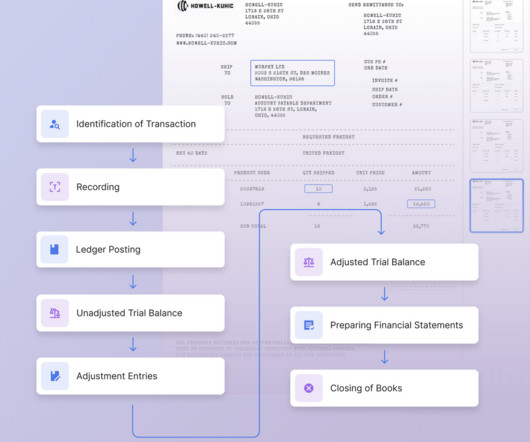

Comparing an Unadjusted and Adjusted Trial Balance Given these definitions, the difference between the two types of trial balance are the adjusting entries made into the accounting system after the unadjusted trial balance is prepared.

Related AccountingTools Courses Accountants’ Guidebook Bookkeeper Education Bundle Bookkeeping Guidebook Related Articles Books of Original Entry General Ledger Overview How to Post to the General Ledger How to Reconcile the General Ledger The Difference Between a Journal and a Ledger The Difference Between the General Ledger and General Journal

Related Articles Accounts Receivable Accounting Accounts Receivable Analysis How to Calculate Average Accounts Receivable How to Reconcile Accounts Receivable The result is more consistent trend lines in the outcomes of reported ratios.

Related AccountingTools Courses How to Audit Liabilities Payables Management Related Articles Accounts Payable Controls How to Reconcile Accounts Payable How to Set Up an Accounts Payable System Scrubbing Accounts Payable This results in a central repository of supplier information, making it easier to spot duplicate payments.

We organize all of the trending information in your field so you don't have to. Join 52,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content