This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Payroll management becomes effortless because the system performs automatic payroll calculations, tax processing, and direct deposit functions. This integration allows entrepreneurs to save time and achieve precise financialrecord accuracy. Payment Processing Options Employees anticipate payments on time.

A Bank Reconciliation Statement is a financialdocument that ensures that the cash balances recorded in the internal financialrecords align with the financialrecords presented in the bank statement. General Ledger ) and the bank’s records (e.g. Bank Statement ).

However, let's understand the manual bank reconciliation process once: Step 1: Gather documents On the bank side, you need the bank statements, outstanding checks, deposits, and any pending transactions. On the company side, you require the company's cashbook, which records both incoming and outgoing transactions.

However, let's understand the manual bank reconciliation process once: Step 1: Gather documents On the bank side, you need the bank statements, outstanding checks, deposits, and any pending transactions. On the company side, you require the company's cashbook, which records both incoming and outgoing transactions.

Book Reconciliation serves as the umbrella term, encompassing a broader spectrum of financial data matching that involves comparing the ledger entries with figures from other financialdocuments. Book Reconciliation entails the comparison of different types of financialrecords of a company.

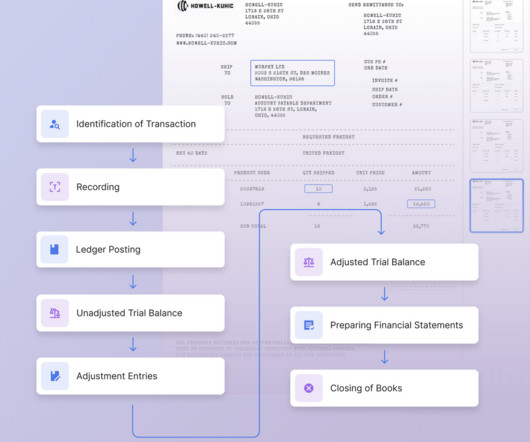

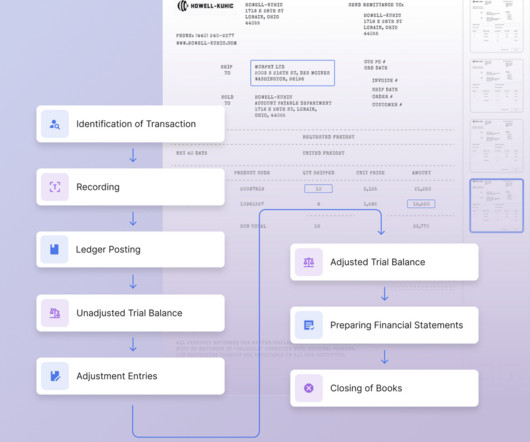

This article highlights the importance of bank reconciliation, and its role in maintaining financial control, accountability, and protection against errors and fraud. Bank reconciliation involves comparing a company's internal financialrecords with those provided by the bank. What Is a Bank Reconciliation?

What Types of Financial Services Are Available ? The types of financial services a small business may consider include: Banking services. Banking services include handling deposits into checking and savings accounts and lending funds to companies. Alternative funding. Accounting and tax services.

In the world of finance and accounting, the process of reconciliation plays a vital role in ensuring accurate and transparent financialrecords. It is a crucial process for businesses to identify discrepancies, resolve errors, and maintain the integrity of their financial statements.

Introduction to Bank Reconciliation Journal Entries Bank reconciliation is an important process in accounting that ensures the accuracy and integrity of a company's financialrecords. It involves the comparison between the company’s internal financialrecords and those of the bank.

Expense reconciliation is a process within finance and accounting that ensures that a company's financialrecords accurately reflect its spending activities. At its core, it involves comparing financial data from various sources within a business to identify any discrepancies or errors and bring them into alignment.

Recording Transactions: Accurate and timely recording of each transaction is essential. This includes documenting payment amounts, dates, and relevant details to maintain a comprehensive financialrecord. This minimizes the manual effort required for deposit handling.

Sales orders and invoices are essential documents in business transactions, but they serve different purposes and play distinct roles in the sales process. They provide a record of customer orders, helping businesses streamline their fulfillment processes and ensure efficient inventory management.

Balance sheet reconciliation is a critical financial process that aligns the financial statements with external documentation such as bank statements, invoices, and general ledger entries. These involve check-marking, the ability to adjust balances, and documenting any findings during the balance sheet reconciliation process.

Maintaining accurate financialrecords is vital for any business, and the general ledger, as the central repository of financial transactions, plays a critical role in this process. These documents will serve as a basis for comparing and reconciling the account balances in the general ledger.

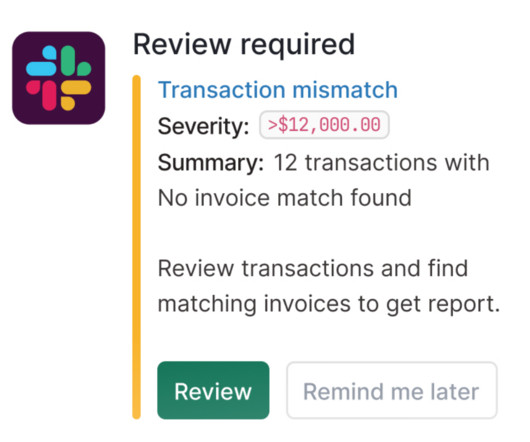

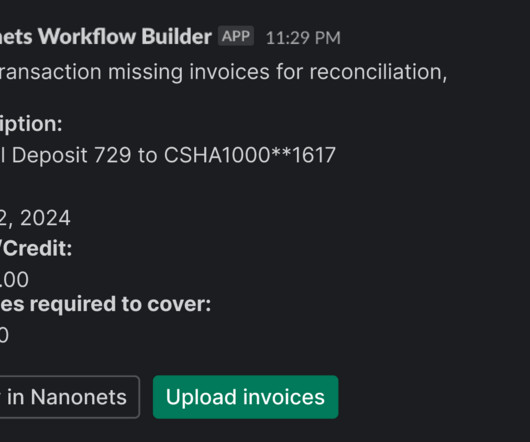

Integrate Nanonets Reconcile financial statements in minutes Try for Free What are Outstanding Checks? An outstanding check is a payment yet to be cashed or deposited, remaining within the bank's clearing cycle. Accounting discrepancies may occur when outstanding checks are not accurately recorded and tracked.

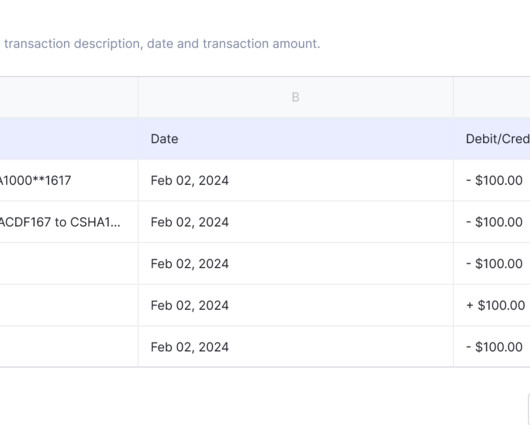

The two ledgers generally don’t match due to factors such as bank fees, interest, outstanding checks, and deposits in transit. These discrepancies must be accounted for in a bank reconciliation statement to represent the current financial position accurately. What Is a Bank Reconciliation Statement?

Month-end close is a widely accepted accounting standard that is aimed at keeping an accurate set of financialrecords and detecting errors/fraud. It involves recording, reviewing, and reconciling records at the end of every month. Once you finish your reconciliation, you can send your record and statement for review.

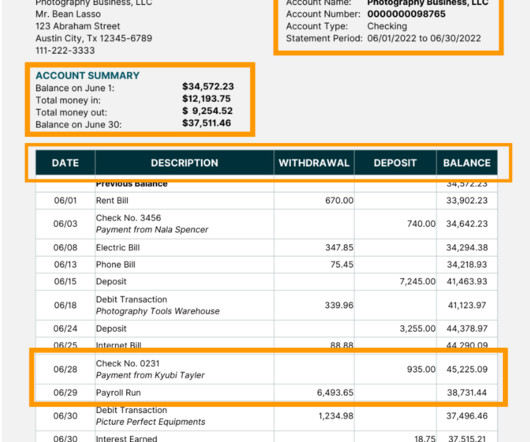

A bank reconciliation statement is a financialdocument that compares a company's bank account balance to the transactions recorded on its general ledger, often called the "cash books." Step #3 Identify items that have hit the company records but are missed on the bank statement.

At the core of accounts management lies account reconciliation, the process of comparing various financialdocuments to ensure accuracy and accountability. Make Adjustments: Record missing transactions and correct errors for accurate balances. Document Process: Maintain detailed records of steps, findings, and adjustments.

Finance reconciliation plays a pivotal role in ensuring the reliability and accuracy of a business's financialrecords. This essential practice involves comparing transactions and other financial activities with supporting documentation and resolving any discrepancies that may arise.

Reconciling the bank statement involves comparing the company's internal financialrecords or ledger to the bank statement received via the bank. On the company side, you require the company's cashbook, which records both incoming and outgoing transactions. Match the deposits in the two statements.

It is a record of all financial transactions of an enterprise and provides a comprehensive account of the organization's monetary activities. However, the GL is not the sole repository of financial data. What is the General Ledger? What is General Ledger Reconciliation and What are Its Types?

Direct Bank Transfers Seamless Payments: Automated payroll systems facilitate direct deposits into employees’ bank accounts, streamlining the payment process and eliminating the need for manual cheque handling. Reduced Administrative Work: Simplifies the management of financialrecords. Enhanced Data Security 6.1

Matching and validating entries would mean data consolidation across sub-ledgers, vendor invoices, bank statements, receipts, and account receivables to ensure timely and accurate month-end and year-end closing of the financial books. Overall, accurate reconciliation is essential for maintaining a business's financial health.

With financial transactions and digital verifications happening at the click of a button, a new trend has emerged - the rise of fake bank statements. It records your financial activity and is widely accepted as proof of creditworthiness in different applications for loans, jobs, insurance claims, etc.

Recording purchase invoices as soon as they are received and verified helps detect potential fraud related to duplicate payments, fictitious vendors, or inflated expenses. Prompt depositing and recording cash receipts minimizes the risk of theft or misappropriation. Approval and authorization records.

Stripe directly fetches this data through Financial Connections on a daily basis, ensuring alignment between Stripe's records and actual bank deposits. It helps to document these protocols and ensure adherence across the organizational spectrum. How to Set up Stripe Reconciliation?

PDF → Excel Convert PDF bank statements to Excel Try for Free The digitization of financialdocuments is an important task for financial institutions like banks as well as individual banking customers and businesses. The various areas of application of bank statements OCR are also discussed.

Payment reconciliation refers to the process of comparing and matching financial data from different sources to ensure accuracy and consistency in the recorded transactions. This process helps identify any missing or unmatched payments, duplicate transactions, or other errors that may impact the financialrecords.

Establishing a record-keeping system for tracking income and expenses is essential. Accurate financialrecords can simplify tax preparation, inform business decisions, and ensure legal and financial compliance. First and foremost, you need to establish a record keeping system to maintain accurate financialrecords.

Incorrect data entries and data omissions can lead to inaccurate financialrecords. Lack of security Manual accounting processes typically involve maintaining physical records. Inefficient collaboration Manual accounting often relies on an exchange of physical documents and interpersonal communication.

If a customer calls you and asks about their payment, can you see the date it was received and deposited? Audit trails should include key information such as what, who, when, where, and how to document each step of a transaction or event. An audit trail can track multiple documents or transactions related to a single project.

Account reconciliation is a critical process in accounting, which ensures that financialrecords are accurate and consistent. By incorporating efficient reconciliation in accounting practices, organizations can maintain a solid financial foundation, detect discrepancies, and reduce the risk of financial errors.

Whether you're a loan officer reviewing an application or a business owner ensuring your clients’ payments are in order, bank statement verification is integral to ensuring financial accuracy and fraud prevention. Let’s discuss bank statement verification and find answers to some of your biggest challenges.

In this blog, we will explore the essential task of filling out receipt books, a foundational element of financialrecord-keeping for both small and large businesses. Documenting transactions in receipt books ensures accuracy in financial management, compliance with tax regulations, and the ability to resolve discrepancies with ease.

One misplaced digit could lead to miscalculations, resulting in financial discrepancies that could harm your business. Accounting automation ensures precision, minimizes errors, and maintains the integrity of your financialrecords. Automatic online payments directly deposited into your bank account.

Record-Keeping: Accurate record-keeping is essential. Each disbursement is documented with details such as the recipient, payment amount, purpose, date, and any relevant reference numbers. Checks are widely used for various financial transactions.

The goal of an expense reimbursement process is not just to ensure that employees are compensated in a timely and fair manner but also to maintain accurate financialrecords and comply with tax laws and regulations. Receipt and Documentation Requirements : Specify the documentation needed to substantiate expenses.

Think of subscriptions paid upfront or deposits for future work—income waiting to be earned. Unlike assets you own outright, operating leases involve using resources without long-term ownership rights, making them less visible in financialrecords. That’s deferred revenue—an often overlooked aspect on balance sheets.

Think of subscriptions paid upfront or deposits for future work—income waiting to be earned. Unlike assets you own outright, operating leases involve using resources without long-term ownership rights, making them less visible in financialrecords. That’s deferred revenue—an often overlooked aspect on balance sheets.

To ensure the integrity of financial data, accountants and bookkeepers rely on the general ledger account reconciliation process. This process involves comparing general ledger accounts with supporting documents using reconciliation software to identify discrepancies and take corrective measures.

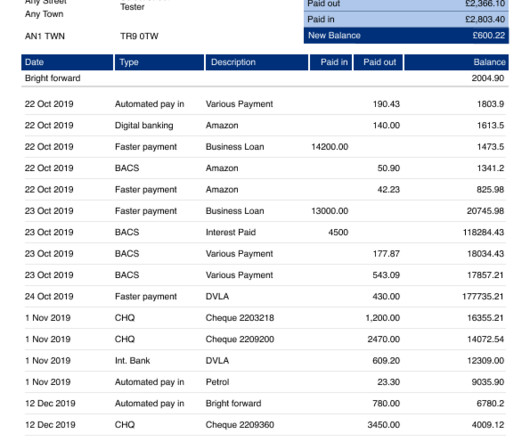

Recording business transactions in Excel is simple. You can see every activity: your direct deposit, your cell phone bill, the pizza you ordered, and a balance that shows how much is in the account after every transaction. Try Nanonets Now Schedule a Demo How to Generate Financial Statements in Excel? No credit card is required.

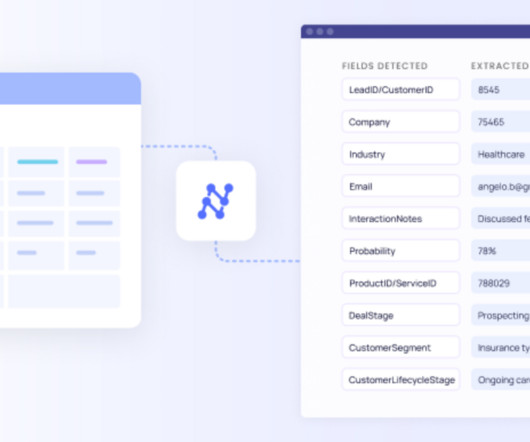

Reconciliation This step involves matching the extracted data with the company’s internal records. For instance, if the bank statement shows a $1,000 deposit on a specific date, it matches the corresponding entry in the accounting records. Establish a structured adjustment process with thorough documentation.

In many organizations, they’re a necessary tool for organizing financialrecords and setting up accounting systems. The central purpose of a COA is to provide a foundation within which all of a company’s financialrecords are kept according to an easy-to-follow, logical structure. Fortunately, the answer is simple.

We organize all of the trending information in your field so you don't have to. Join 52,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content