This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Related Courses Bookkeeping Guidebook Corporate Cash Management How to Audit Cash Reconciling a bank statement involves comparing the bank's records of checking account activity with your own records of activity for the same account. To reconcile a bank statement, follow the steps noted below. If so, adjust your record of the deposit.

Regularly Reconcile Transactions Reconciling sales data with bank statements and payment processors prevents discrepancies. Steps include: Matching invoices with actual deposits Reviewing transaction reports for inconsistencies Ensuring marketplace fees and commissions are properly recorded 6.

Whether it was a lost package, a delayed delivery, or a stolen piece of mail, it can be frustrating and time-consuming to handle the fallout. Many businesses are starting to realize that trusting critical documents like check payments to arrive securely by mail may not be worth the risk. to $14 per transaction.

Why is it Important to Reconcile your Bank Account? Reconciling the bank statement involves comparing the company's internal financial records or ledger to the bank statement received via the bank. How Often Should You Reconcile Your Bank Statements? They can benefit by reconciling their bank statements monthly.

Balance sheet reconciliation is a critical financial process that aligns the financial statements with external documentation such as bank statements, invoices, and general ledger entries. Finance teams can also follow specific templates designed to reconcile their balance sheets manually. What is Balance Sheet Reconciliation?

However, let's understand the manual bank reconciliation process once: Step 1: Gather documents On the bank side, you need the bank statements, outstanding checks, deposits, and any pending transactions. Match the deposits in the two statements. Why is it important to reconcile your bank statements?

However, let's understand the manual bank reconciliation process once: Step 1: Gather documents On the bank side, you need the bank statements, outstanding checks, deposits, and any pending transactions. Match the deposits in the two statements. Why is it important to reconcile your bank statements?

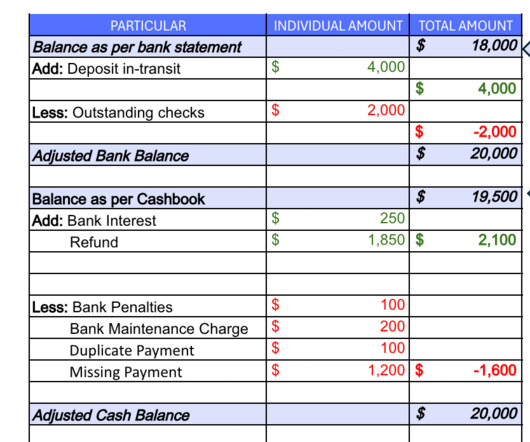

A Bank Reconciliation Statement is a financial document that ensures that the cash balances recorded in the internal financial records align with the financial records presented in the bank statement. In effect, the reconciliation statement is a document that presents the comparison between the internal financial records of a company (e.g.

Our free Bank reconciliation template provides a simple way to reconcile your cashbook with your bank statement. Here’s how we can do bank reconciliation: Gather documents You will need the company cashbook and bank statements. Match documents We need to find out the matching transactions in the bank statement and the cashbook.

Book Reconciliation serves as the umbrella term, encompassing a broader spectrum of financial data matching that involves comparing the ledger entries with figures from other financial documents. This comparison helps detect differences such as outstanding checks, deposits in transit, bank fees, errors, or unauthorized transactions.

Learning to reconcile with QuickBooks Online is a starting step for using QuickBooks to manage books. QuickBooks is a handy tool to help you reconcile your accounts without using any external tools. Step 1: Go to the reconciliation menu Search for “Reconcile” in the top help menu bar.

It involves recording, reviewing, and reconciling records at the end of every month. Closes can be quite stressful as the general turnaround time is <1 week, while you just have 2-3 days to reconcile all your accounts. Now find the corresponding type in your bank statement and mark them as reconciled or “not found.

One method involves a thorough review of documents and transactions to verify their accuracy and consistency with bank statements. Identifying and Investigating Discrepancies: Searching for missing deposits or unauthorized charges, and contacting the bank if needed.

I recommend starting out with all invoices, customer payments, and deposits. Tip #2: Reconcile business bank and credit card accounts. Symptom #1: Whenever they go into bank deposits , they see that they have a lot of old unclear transactions in undeposited funds. Step #3: A deposit is recorded to the correct bank account.

At the core of accounts management lies account reconciliation, the process of comparing various financial documents to ensure accuracy and accountability. Document Process: Maintain detailed records of steps, findings, and adjustments. Investigate Discrepancies: Analyze differences, trace transactions and rectify errors.

The aim is to reconcile the data and ensure that transactions match supporting documents across different sources. Here are the general steps involved: Gather relevant documents Collect all the necessary financial documents that need to be reconciled. What are the steps in the Process of Reconciliation?

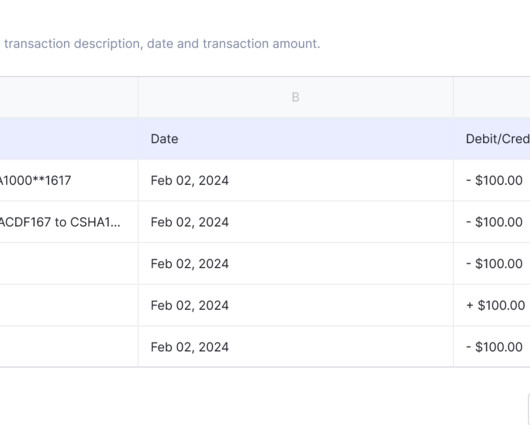

A bank reconciliation statement is a financial document that compares a company's bank account balance to the transactions recorded on its general ledger, often called the "cash books." For example, a deposit of $5,000 on June 1st and a check #123 for $1,000 on June 3rd. What Is a Bank Reconciliation Statement?

If any checks recorded by the bank as having cleared are listed incorrectly by the bank, contact the bank and send them documentation of the error. In the meantime, the difference will be a reconciling item. Update Deposits in Transit Go to the deposits section of the bank reconciliation module. Check printing fees.

With disconnected data sources and innumerable documentation, accounting teams can face the added task of figuring in interest rates, exchange rates, and timing differences to reconcile balances effectively. Bank service fees, deposits in transit, outstanding checks, and interest rates must be factored into the reconciliation process.

They are needed to ensure that checks are recorded correctly, deposited promptly, and not stolen or altered anywhere in the process. Also, stamp “ for deposit only ” and the company’s bank account number on every check received; this makes it more difficult for someone to extract a check and deposit it into some other bank account.

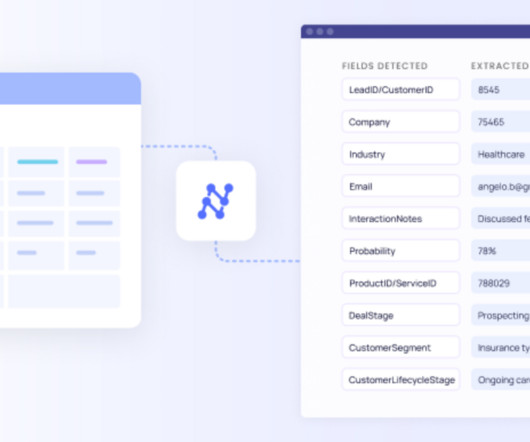

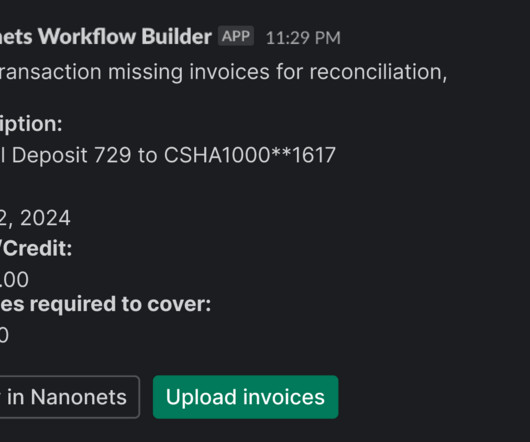

Integrate Nanonets Reconcile financial statements in minutes Try for Free What is Journal Entry in accounting? These differences may arise due to outstanding checks, deposits in transit, bank fees, interest earned, or other transactions that have not been accurately recorded or reflected in both sets of records.

This process typically involves reviewing transactions, invoices, receipts, and other financial documents to verify that they match up with the company's records and budget. By reconciling expenses, businesses can ensure that they comply with these regulations and avoid potential penalties or legal issues.

QuickBooks is one of the most widely used apps for bookkeeping, and it offers a convenient way to reconcile credit cards without needing external tools. Step 1: Go to the reconciliation menu In the top help menu bar, search for 'Reconcile.' ' Then, select the account you wish to reconcile.

By choosing an enhanced direct deposit option , Leading Edge Construction Services Inc. We receive big physical checks and not only do they arrive late, we have to then take them to the bank to deposit and wait even longer for the 3-5 day hold to lift to finally have access to the funds.”

It involves comparing and matching the account balances in the general ledger with supporting documentation, such as bank statements, invoices, receipts, and other financial records. The process may vary depending on the complexity of the organization and the specific accounts being reconciled.

Whether it's ensuring that expenses align with available funds or guaranteeing that business transactions accurately reflect the company's financial standing, tracking checks outstanding and reconciling bank statements is non-negotiable. Checks outstanding can disrupt cash flow management.

Businesses maintain a multitude of other financial documents, including bank statements, invoices , bills, cash payment receipts, and more. These documents provide supplementary details and serve as external sources of validation for the transactions recorded in the general ledger. What is the General Ledger?

From forging bank statements in job and loan applications to issuing fake bank statements for visa processing and insurance claims, these fake documents seriously threaten individuals, businesses, and financial institutions. Fake bank statements Fake bank statements are fraudulent documents designed to look like genuine bank statements.

This includes documenting payment amounts, dates, and relevant details to maintain a comprehensive financial record. Bank Deposits: Depositing received funds into the appropriate bank accounts ensures liquidity and provides a clear trail for financial reconciliation.

How do you communicate, share documents, and collaborate on the books? Document management. Document storage and document management: Box. 2: Paperless document management. When it comes to paperless document management, there are several areas you need to address for virtual bookkeeping. Document fetching.

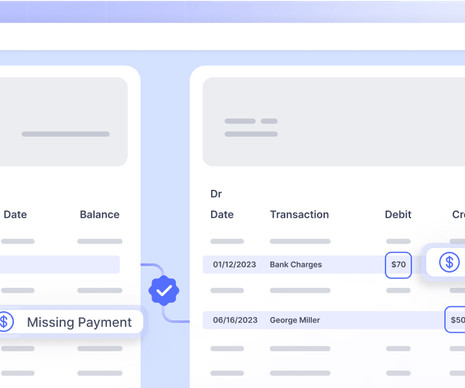

Deposits in transit. As was the case with outstanding checks, this difference will vanish when the bank receives the deposits. Interest on deposited cash. Examples are outstanding checks and deposits in transit. This difference will eventually vanish, when the bank receives the checks.

Account reconciliation is the process of comparing general ledger accounts (usually from the balance sheet) with supporting documents, such as bank statements, sub-ledgers, and other underlying transaction details. How to Reconcile Accounts? Furthermore, not all reconciling items necessitate adjustments to the balance.

This essential practice involves comparing transactions and other financial activities with supporting documentation and resolving any discrepancies that may arise. The source documents include invoices, receipts, and transaction statements. How to reconcile financial statements?

Prompt depositing and recording cash receipts minimizes the risk of theft or misappropriation. A rigorous bookkeeping process regularly reconciles accounts receivable balances with customer statements and payments. A quality bookkeeping process will regularly reconcile company credit card statements with internal expense records.

As transactions flow in and out, reconciling payments becomes crucial to ensure accuracy, identify discrepancies, and maintain a clear financial picture. This article will provide a comprehensive guide to reconciling payments, its importance, challenges faced, best practices, and the role of automation in enhancing the process.

Stripe directly fetches this data through Financial Connections on a daily basis, ensuring alignment between Stripe's records and actual bank deposits. It helps to document these protocols and ensure adherence across the organizational spectrum. How to Set up Stripe Reconciliation?

A reconciliation statement is a document that begins with a company's own record of an account balance , adds and subtracts reconciling items in a set of additional columns, and then uses these adjustments to arrive at the record of the same account held by a third party. Debt accounts.

Sales orders and invoices are essential documents in business transactions, but they serve different purposes and play distinct roles in the sales process. While sales orders may not always be recorded in accounting records, invoices should always be properly documented.

A bank statement is a document that is issued by a bank once a month to its customers, listing the transactions impacting a bank account. Any discrepancies may have arisen at the bank (such as a transposed number in a check payment or a deposit), for which the bank should be contacted at once to make an adjusting entry.

We will cover everything you need to know , from tracking expenses and invoices to reconciling bank statements and choosing the right bookkeeping software. This allows you to track your expenses on-the-go, making it easier to remember to document your expenses as they happen. One of the most popular methods is mobile expense tracking.

The creation of financial transactions includes posting information to accounting journals or accounting software from such source documents as invoices to customers, cash receipts , and supplier invoices. The bookkeeper also reconciles accounts to ensure their accuracy.

It’s not like a traditional bank account where you deposit money but instead more of a relationship with a merchant account provider that serves as a bridge between your customer’s credit account and your business bank account. In total, the time from payment to deposit is about 1-2 days with a merchant account.

PDF → Excel Convert PDF bank statements to Excel Try for Free A bank extract is data extracted from bank statements or other financial documents. These are official documents issued by a bank that provide detailed information on a customer's account transactions and balances.

This process involves comparing general ledger accounts with supporting documents using reconciliation software to identify discrepancies and take corrective measures. Once approved, the reconciled data is securely stored in a centralized database, ensuring an auditable trail. Pros: Unlimited users with customizable permissions.

We organize all of the trending information in your field so you don't have to. Join 52,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content