This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

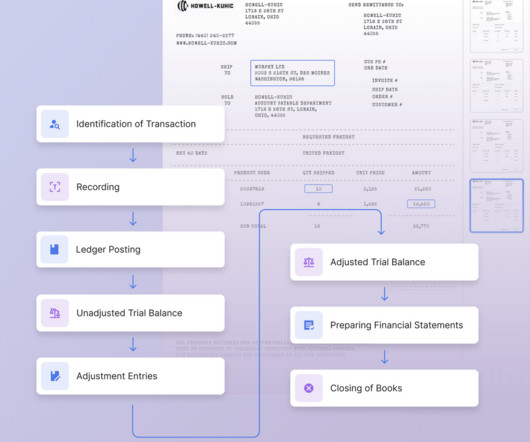

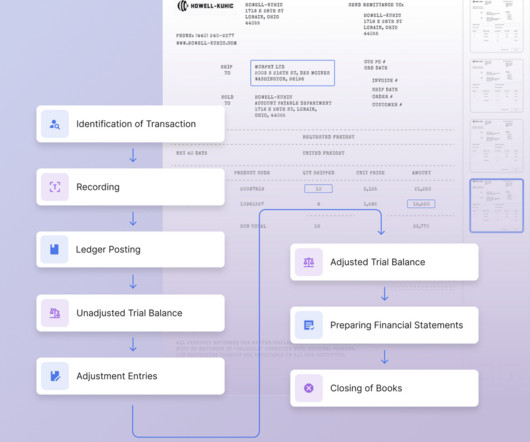

Bookkeepers ensure these buckets are properly categorized and meticulously record every deposit and withdrawal. This ongoing process provides a clear picture of a company’s financial health at any given time. This involves strong data entry skills and a keen eye for detail.

Sales orders and invoices are essential documents in business transactions, but they serve different purposes and play distinct roles in the sales process. On the other hand, an invoice is sent by the business to request payment from the customer after the products or services have been delivered.

Take a look at this bookkeeping cleanup checklist to get all your financial ducks in a row. Collect all your financialrecords It’s hard to say which part of this process is the most difficult, but depending on the type of business you have, rounding up all your past financialrecords may be the most time-consuming.

A Bank Reconciliation Statement is a financial document that ensures that the cash balances recorded in the internal financialrecords align with the financialrecords presented in the bank statement. General Ledger ) and the bank’s records (e.g. Bank Statement ). Bank Statement ).

With automated reconciliation, your ecommerce accounting services will reconcile sales, bank deposits, and expenses across Shopify, Etsy, eBay, and other channels so that every dollar is accounted for. Establish Financial Goals and Monitor Progress Don’t do it without goals.

Book Reconciliation entails the comparison of different types of financialrecords of a company. These records may be internal financialrecords or external. Companies maintain various internal records to track their financial activities accurately and ensure compliance with accounting standards.

Fluctuating exchange rates, varying tax structures, and complex regulations make financial operations difficult to streamline. As the global e-invoicing market is expected to grow from USD 4.79 Key Features Reach Any Market with 125+ Currencies: With Invoicera, you can invoice clients in more than 125 different currencies.

This article highlights the importance of bank reconciliation, and its role in maintaining financial control, accountability, and protection against errors and fraud. Bank reconciliation involves comparing a company's internal financialrecords with those provided by the bank. What Is a Bank Reconciliation?

However, let's understand the manual bank reconciliation process once: Step 1: Gather documents On the bank side, you need the bank statements, outstanding checks, deposits, and any pending transactions. On the company side, you require the company's cashbook, which records both incoming and outgoing transactions.

However, let's understand the manual bank reconciliation process once: Step 1: Gather documents On the bank side, you need the bank statements, outstanding checks, deposits, and any pending transactions. On the company side, you require the company's cashbook, which records both incoming and outgoing transactions.

Payment reconciliation is the process of matching and verifying payments against records, ensuring that the transactions are accurate and complete. The role of payment reconciliation in maintaining financial accuracy is critical, as it helps businesses track their income, verify the legitimacy of transactions and prevent discrepancies.

Expense reconciliation is a process within finance and accounting that ensures that a company's financialrecords accurately reflect its spending activities. At its core, it involves comparing financial data from various sources within a business to identify any discrepancies or errors and bring them into alignment.

It helps you keep track of your expenses, invoices, and bank statements, and allows you to make informed decisions about the future of your business. We will cover everything you need to know , from tracking expenses and invoices to reconciling bank statements and choosing the right bookkeeping software.

A balance sheet is a financial statement that provides a snapshot of a company's financial position at a specific point in time. Balance sheet reconciliation is a critical financial process that aligns the financial statements with external documentation such as bank statements, invoices, and general ledger entries.

In the world of finance and accounting, the process of reconciliation plays a vital role in ensuring accurate and transparent financialrecords. It is a crucial process for businesses to identify discrepancies, resolve errors, and maintain the integrity of their financial statements.

Month-end close is a widely accepted accounting standard that is aimed at keeping an accurate set of financialrecords and detecting errors/fraud. It involves recording, reviewing, and reconciling records at the end of every month. Once you finish your reconciliation, you can send your record and statement for review.

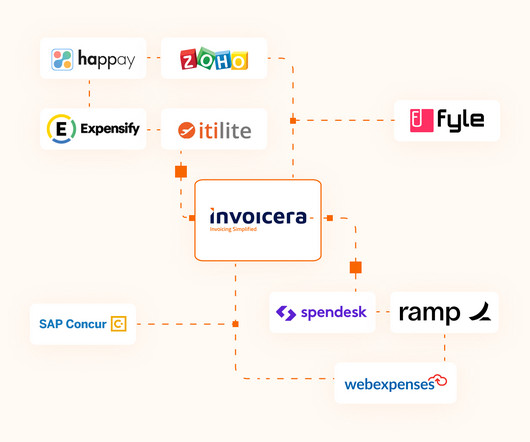

Invoicera Invoicera is a versatile expense management tool offering comprehensive features to simplify financial processes. From expense tracking and reporting to invoice generation , this tool provides businesses with a one-stop solution for managing expenses efficiently. It can lead to better job satisfaction and better morale.

Adopt Effective Accounting Software Simplify Financial Management: Implement accounting software like QuickBooks or Xero to streamline your bookkeeping. These tools automate tasks such as recording transactions, generating invoices, and creating financial reports. Establish a Robust Bookkeeping System 1.1

Maintaining accurate financialrecords is vital for any business, and the general ledger, as the central repository of financial transactions, plays a critical role in this process. Regular and timely reconciliation is essential to maintain accurate financial information and support informed decision-making.

One misplaced digit could lead to miscalculations, resulting in financial discrepancies that could harm your business. Accounting automation ensures precision, minimizes errors, and maintains the integrity of your financialrecords. Invoice Processing: From Chaos to Clarity Automation streamlines the invoice processing journey.

Finance reconciliation plays a pivotal role in ensuring the reliability and accuracy of a business's financialrecords. This essential practice involves comparing transactions and other financial activities with supporting documentation and resolving any discrepancies that may arise.

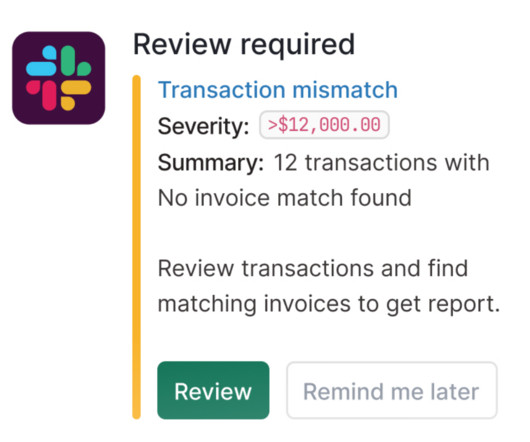

As transactions flow through various channels, the risk of human oversight increases, leading to inaccuracies in recording payment details. This dilemma of mistakes can result in misaligned financialrecords, delayed reconciliations, and a potential domino effect on downstream financial processes.

Reconciling the bank statement involves comparing the company's internal financialrecords or ledger to the bank statement received via the bank. On the company side, you require the company's cashbook, which records both incoming and outgoing transactions. Match the deposits in the two statements.

Payment reconciliation refers to the process of comparing and matching financial data from different sources to ensure accuracy and consistency in the recorded transactions. This process helps identify any missing or unmatched payments, duplicate transactions, or other errors that may impact the financialrecords.

Need for Account Reconciliation Account Reconciliation ensures the accuracy and integrity of financialrecords by identifying discrepancies and errors, thus fostering trust among stakeholders and facilitating informed decision-making. It's essential to ensure that all transactions are accurately recorded and accounted for.

That’s why keeping tabs on all your supplier invoices is essential for ensuring they don’t fall past due. What Your Accounts Payable Template Should Include The accounts payable ledger is an aging report that allows you to track the payments and due dates for all your supplier’s invoices.

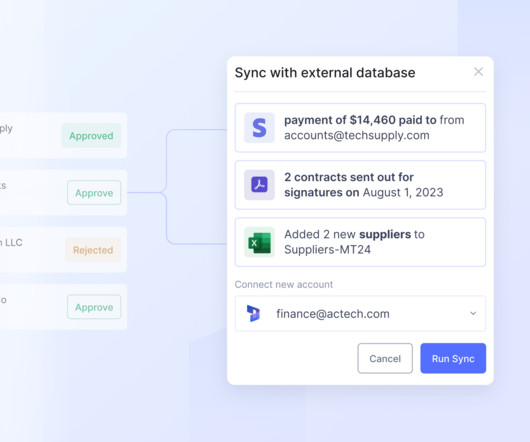

Stripe can be used to automate the comparison of internal records like invoices with external data such as settlement files and bank statements, reducing manual effort and errors. It ensuresthat the money flowing through the Stripe account matches what your business expects, leaving no room for discrepancies or errors.

For example, Timely recording of sales transactions reduces the likelihood of unrecorded sales or manipulation of revenue figures. Recording purchase invoices as soon as they are received and verified helps detect potential fraud related to duplicate payments, fictitious vendors, or inflated expenses.

It is a record of all financial transactions of an enterprise and provides a comprehensive account of the organization's monetary activities. However, the GL is not the sole repository of financial data. It helps in identifying any discrepancies or overdue payments that need to be addressed.

Incorrect data entries and data omissions can lead to inaccurate financialrecords. Lack of security Manual accounting processes typically involve maintaining physical records. Easy access to essential data helps track trends, detect fraud, and assess a business's financial health.

Step #3 Identify items that have hit the company records but are missed on the bank statement. Cash that has been received and recorded by the company but has not yet been recorded on the bank statement is called " deposits in transit." These need to be adjusted in the company's records.

Matching and validating entries would mean data consolidation across sub-ledgers, vendor invoices, bank statements, receipts, and account receivables to ensure timely and accurate month-end and year-end closing of the financial books. This includes bank statements, credit card statements, vendor invoices and ledgers.

Recording transactions, Managing accounts receivable and payable, Monitoring the cash flow, Reconciling bank accounts, Creating journal entries, Issuing invoices, Payroll tax preparation, income tax, sales tax, tax return, etc. Bookkeeping is the process of tracking finances and keeping records.

For corporations, the extraction of data from bank statements helps monitor the business’s progress and serves as a financialrecord for tax filing operations. Businesses can use data extracted from bank statements to assess the financial health of the company, total assets, identity liabilities, and list out deductions.

Key Features for Financial Reporting Invoicera has several cool features that make it a real champ for financial reporting: Automated Invoicing: With Invoicera, you can send out invoices quickly and properly. This lets you have the right financialrecords which are a must for reporting and tax times.

Think of subscriptions paid upfront or deposits for future work—income waiting to be earned. Unlike assets you own outright, operating leases involve using resources without long-term ownership rights, making them less visible in financialrecords. That’s deferred revenue—an often overlooked aspect on balance sheets.

Accounting and Reporting: After making the disbursement, the payer reconciles their financialrecords to ensure that the payment has been accurately recorded and that the account balances reflect the transaction.The disbursement is accounted for in financial statements and reports.

The goal of an expense reimbursement process is not just to ensure that employees are compensated in a timely and fair manner but also to maintain accurate financialrecords and comply with tax laws and regulations. Approval workflow is integrated into the company's expense management software for tracking and record-keeping.

Whenever you need to find a line item on an old invoice, do you find yourself having to go back and search through mountains of paperwork, or thumb through rows of filing cabinets drawers? In many organizations, they’re a necessary tool for organizing financialrecords and setting up accounting systems.

If a customer calls you and asks about their payment, can you see the date it was received and deposited? 💡 Key Takeaways Every business can benefit from implementing audit trails to ensure transparency and accuracy in financialrecords. How easy is it to go back and find information about your business?

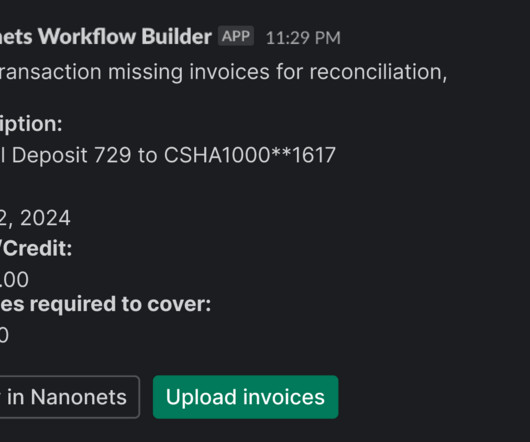

Excel can also be used to create a full accounting system, complete with financial statements, for a complex business with lots of expenses, income streams, assets, and debts. Try Nanonets to get access to 24x7 support and pay your invoices without leaving Nanonets. Recording business transactions in Excel is simple.

Reconciliation software is a specialized application that automates and streamlines the financial closing process for businesses. Acting as a centralized platform, it retrieves data from the general ledger and compares it with bank statements and invoices, facilitating accurate and swift account reconciliation.

Record your deposits in a correct way. Business owners generally make a variety of deposits into their bank account throughout the year. Their range of deposits may include the loans they have made from other banks, the revenue from their sales and cash infusions from their personal savings. Monitor your invoices.

A federal credit union told the Justice Department that 59 out of 60 SBA deposits it received appeared to be fraudulent. David Leary: [00:20:22] Because it's Intuit's account, you connect your merchant service to it; do instant deposits. You can get instant deposits to that account free of charge. They have a cashflow planner.

We organize all of the trending information in your field so you don't have to. Join 52,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content