This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Bookkeepers ensure these buckets are properly categorized and meticulously record every deposit and withdrawal. This ongoing process provides a clear picture of a company’s financial health at any given time. Software proficiency: Proficiency in bookkeeping software like QuickBooks is essential.

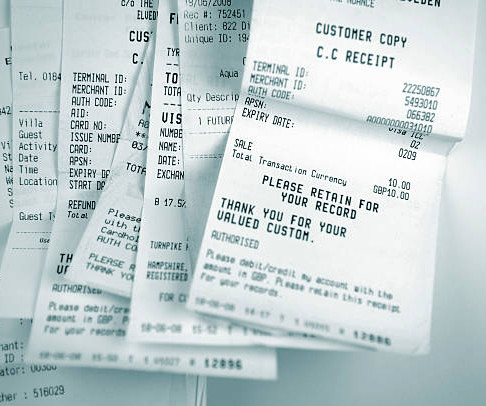

Why is it Important to Reconcile your Bank Account? Reconciliation is a crucial accounting process that ensures the accuracy of the financial close process. Reconciling the bank statement involves comparing the company's internal financialrecords or ledger to the bank statement received via the bank.

A Bank Reconciliation Statement is a financial document that ensures that the cash balances recorded in the internal financialrecords align with the financialrecords presented in the bank statement. General Ledger ) and the bank’s records (e.g. Bank Statement ).

However, let's understand the manual bank reconciliation process once: Step 1: Gather documents On the bank side, you need the bank statements, outstanding checks, deposits, and any pending transactions. On the company side, you require the company's cashbook, which records both incoming and outgoing transactions.

However, let's understand the manual bank reconciliation process once: Step 1: Gather documents On the bank side, you need the bank statements, outstanding checks, deposits, and any pending transactions. On the company side, you require the company's cashbook, which records both incoming and outgoing transactions.

Take a look at this bookkeeping cleanup checklist to get all your financial ducks in a row. Collect all your financialrecords It’s hard to say which part of this process is the most difficult, but depending on the type of business you have, rounding up all your past financialrecords may be the most time-consuming.

Introduction to Bank Reconciliation Journal Entries Bank reconciliation is an important process in accounting that ensures the accuracy and integrity of a company's financialrecords. It involves the comparison between the company’s internal financialrecords and those of the bank.

Book Reconciliation entails the comparison of different types of financialrecords of a company. These records may be internal financialrecords or external. Companies maintain various internal records to track their financial activities accurately and ensure compliance with accounting standards.

With automated reconciliation, your ecommerce accounting services will reconcile sales, bank deposits, and expenses across Shopify, Etsy, eBay, and other channels so that every dollar is accounted for. No more lying awake at night worrying that payments are missing or that there are duplicate postings.

This article highlights the importance of bank reconciliation, and its role in maintaining financial control, accountability, and protection against errors and fraud. Bank reconciliation involves comparing a company's internal financialrecords with those provided by the bank. What Is a Bank Reconciliation?

The role of payment reconciliation in maintaining financial accuracy is critical, as it helps businesses track their income, verify the legitimacy of transactions and prevent discrepancies. Accurate financialrecords are essential for businesses to meet auditing requirements and avoid potential fines or penalties for non-compliance.

Expense reconciliation is a process within finance and accounting that ensures that a company's financialrecords accurately reflect its spending activities. At its core, it involves comparing financial data from various sources within a business to identify any discrepancies or errors and bring them into alignment.

In the world of finance and accounting, the process of reconciliation plays a vital role in ensuring accurate and transparent financialrecords. It is a crucial process for businesses to identify discrepancies, resolve errors, and maintain the integrity of their financial statements.

Month-end close is a widely accepted accounting standard that is aimed at keeping an accurate set of financialrecords and detecting errors/fraud. It involves recording, reviewing, and reconcilingrecords at the end of every month. Month-end reconciliation is the most important part of the month-end close process.

Integrate Nanonets Reconcilefinancial statements in minutes Explore for Free Manual reconciliation processes are more complex when balance sheet transactions require reconciliation across multiple general ledgers, ERPs, invoices, and bank accounts.

Maintaining accurate financialrecords is vital for any business, and the general ledger, as the central repository of financial transactions, plays a critical role in this process. The process may vary depending on the complexity of the organization and the specific accounts being reconciled.

Need for Account Reconciliation Account Reconciliation ensures the accuracy and integrity of financialrecords by identifying discrepancies and errors, thus fostering trust among stakeholders and facilitating informed decision-making. Make Adjustments: Record missing transactions and correct errors for accurate balances.

Whether it's ensuring that expenses align with available funds or guaranteeing that business transactions accurately reflect the company's financial standing, tracking checks outstanding and reconciling bank statements is non-negotiable.

We will cover everything you need to know , from tracking expenses and invoices to reconciling bank statements and choosing the right bookkeeping software. Establishing a record-keeping system for tracking income and expenses is essential. To reconcile your bank statements, you’ll need to take a few simple steps.

Efficient reconciliation of payments is a vital aspect of financial management for businesses of all sizes. As transactions flow in and out, reconciling payments becomes crucial to ensure accuracy, identify discrepancies, and maintain a clear financial picture. Why is payment reconciliation crucial for businesses?

Finance reconciliation plays a pivotal role in ensuring the reliability and accuracy of a business's financialrecords. This essential practice involves comparing transactions and other financial activities with supporting documentation and resolving any discrepancies that may arise. What is finance reconciliation?

This includes documenting payment amounts, dates, and relevant details to maintain a comprehensive financialrecord. Bank Deposits: Depositing received funds into the appropriate bank accounts ensures liquidity and provides a clear trail for financial reconciliation.

With disconnected data sources and innumerable documentation, accounting teams can face the added task of figuring in interest rates, exchange rates, and timing differences to reconcile balances effectively. Bank service fees, deposits in transit, outstanding checks, and interest rates must be factored into the reconciliation process.

Step #3 Identify items that have hit the company records but are missed on the bank statement. Cash that has been received and recorded by the company but has not yet been recorded on the bank statement is called " deposits in transit." These need to be adjusted in the company's records.

There are several types of general ledger reconciliations: Bank Reconciliation : This type of reconciliation involves comparing the transactions recorded in the general ledger with those reflected in the company's bank statements. Incomplete Records : Missing or incomplete records can hinder the reconciliation process.

As transactions flow through various channels, the risk of human oversight increases, leading to inaccuracies in recording payment details. This dilemma of mistakes can result in misaligned financialrecords, delayed reconciliations, and a potential domino effect on downstream financial processes.

Recording purchase invoices as soon as they are received and verified helps detect potential fraud related to duplicate payments, fictitious vendors, or inflated expenses. Prompt depositing and recording cash receipts minimizes the risk of theft or misappropriation. To list just a few: Accounts receivable reconciliation.

They provide a record of customer orders, helping businesses streamline their fulfillment processes and ensure efficient inventory management. In contrast, invoices are important for accounting records and tracking payments. Invoice date 5. Due date 6. Accepted payment methods 7.

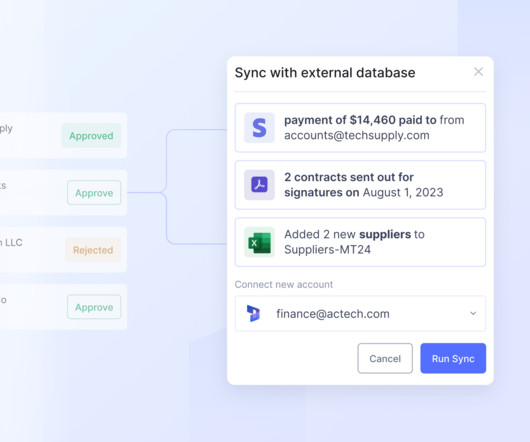

Stripe directly fetches this data through Financial Connections on a daily basis, ensuring alignment between Stripe's records and actual bank deposits. Fortify Security Measures : Financialrecords and systems must be secured by restricting access to authorized personnel and instituting stringent security protocols.

Account reconciliation is a critical process in accounting, which ensures that financialrecords are accurate and consistent. By incorporating efficient reconciliation in accounting practices, organizations can maintain a solid financial foundation, detect discrepancies, and reduce the risk of financial errors.

Recording transactions, Managing accounts receivable and payable, Monitoring the cash flow, Reconciling bank accounts, Creating journal entries, Issuing invoices, Payroll tax preparation, income tax, sales tax, tax return, etc. Bookkeeping is the process of tracking finances and keeping records.

Accounting: For companies, bank statements are crucial for reconciling accounts and ensuring accurate financialrecords. Fraud detection: A periodic review of bank statements can help financial institutions detect unauthorized transactions, fraud, and identity theft early. Look for data entry errors on the bank statement.

Once approved, the reconciled data is securely stored in a centralized database, ensuring an auditable trail. Additionally, reconciliation software offers features such as document upload, access to company policies, electronic signatures, comments, process controls, and user-friendly dashboards for financial insights.

Accounting and Reporting: After making the disbursement, the payer reconciles their financialrecords to ensure that the payment has been accurately recorded and that the account balances reflect the transaction.The disbursement is accounted for in financial statements and reports.

Accounting professionals often find themselves wrestling with mundane tasks: reconciling transactions, generating reports, or manually inputting data, leaving them little time for value-added activities. One misplaced digit could lead to miscalculations, resulting in financial discrepancies that could harm your business.

Whether you're a loan officer reviewing an application or a business owner ensuring your clients’ payments are in order, bank statement verification is integral to ensuring financial accuracy and fraud prevention. Let’s discuss bank statement verification and find answers to some of your biggest challenges.

For businesses processing thousands of bank statements daily—from insurance companies to financial institutions, bank statement processing presents a challenge and an even bigger opportunity for automation. Traditional manual processing and reconciling, which consumes an average of 10-12 hours per week , is no longer an option.

We organize all of the trending information in your field so you don't have to. Join 52,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content