This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Bookkeepers ensure these buckets are properly categorized and meticulously record every deposit and withdrawal. Account management: They manage accounts payable and receivable, process invoices, reconcile accounts, and ensure timely payments and collections. Looking for an accounting or bookkeeping job?

Keeping track of these ensures: Accurate cash flow forecasting Identification of delayed or missing payments Better financial planning and tax compliance 5. Regularly Reconcile Transactions Reconciling sales data with bank statements and payment processors prevents discrepancies.

Tax season is a busy time for finance departments. According to H&R Block , a 1099 is a tax form used in the United States to report various types of income that are not wages, salaries, or tips. It is commonly issued to independent contractors, freelancers, or supplier s who have been paid $600 or more during the tax year.

Why is it Important to Reconcile your Bank Account? Reconciling the bank statement involves comparing the company's internal financial records or ledger to the bank statement received via the bank. How Often Should You Reconcile Your Bank Statements? They can benefit by reconciling their bank statements monthly.

Navigating transactions across different platforms, staying abreast of constantly changing sales tax codes, and properly monitoring expenses can quickly become daunting. The intricate nature of sales tax legislation makes accounting services for ecommerce businesses a necessity in maintaining compliance.

Once you’ve cleaned your bookkeeping, your business will be better prepared for growth, tax season, and investment opportunities. This also greatly impacts your taxes. Reconcile bank statements The next step in your bookkeeping cleanup checklist is to reconcile your bank statements.

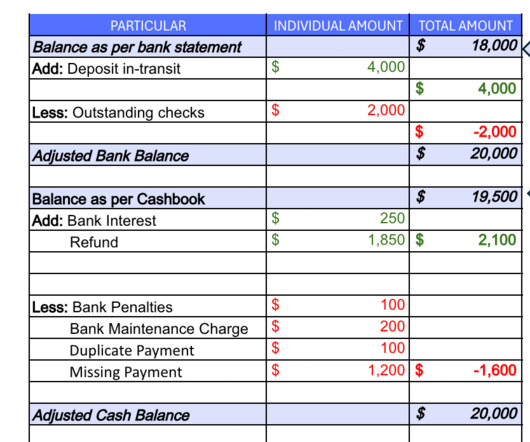

Having an accurate set of financial statements is essential, or it can lead to complications in financial planning, tax compliance, and legal matters. Step 2: Match deposits Following double-entry accounting, a debit in the bank statement is recorded as a credit in the cashbook, and vice versa. Match the deposits in the two statements.

Having an accurate set of financial statements is essential, or it can lead to complications in financial planning, tax compliance, and legal matters. Step 2: Match deposits Following double-entry accounting, a debit in the bank statement is recorded as a credit in the cashbook, and vice versa. Match the deposits in the two statements.

Our free Bank reconciliation template provides a simple way to reconcile your cashbook with your bank statement. Download them in CSV format and paste them into individual Excel sheets.Also, find all the outstanding checks, deposits, and any pending transactions. Reconciling 100s of transactions can take days to resolve completely.

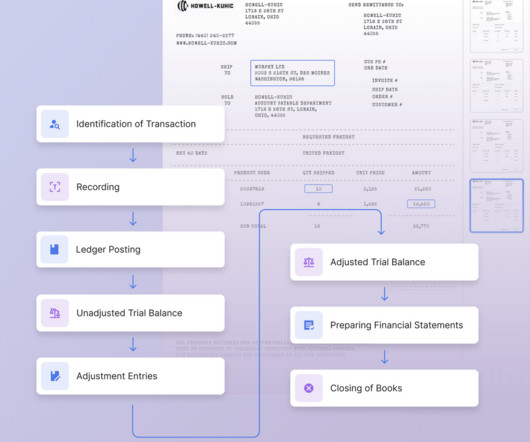

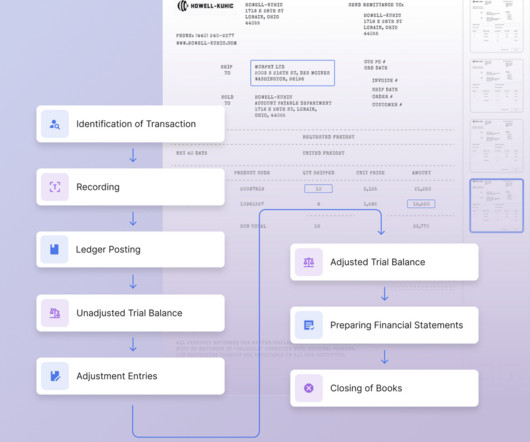

It involves recording, reviewing, and reconciling records at the end of every month. It’s a crucial step to ensure that you prepare an accurate set of statements for financial reporting, planning, and tax compliance. Now find the corresponding type in your bank statement and mark them as reconciled or “not found.”

Here are some examples: · Bank Statements · Credit Card Statements · Vendor Invoices · Customer Invoices · Loan Agreements · Lease Agreements · Insurance Policies · Government Tax Notices. Once identified, these discrepancies are investigated and reconciled to bring the two balances into agreement.

I recommend starting out with all invoices, customer payments, and deposits. Tip #2: Reconcile business bank and credit card accounts. Symptom #1: Whenever they go into bank deposits , they see that they have a lot of old unclear transactions in undeposited funds. Step #3: A deposit is recorded to the correct bank account.

By maintaining your books regularly, reviewing reports, and reconciling your accounts at the end of each month, you can avoid bookkeeping disasters. Finally, having clean books simplifies making wise business choices and helps you stay organized for tax season. Is your bookkeeping disorganized?

Reconcile Cash and Receipts At the end of each day, reconcile all cash payments and payment receipts received in the general ledger to get a good idea of each client’s cash balance. Deposit Cash and Check Payments Most client transactions these days likely take place electronically.

Cash that has been received and recorded by the company but has not yet been recorded on the bank statement is called " deposits in transit." For example, a deposit of $5,000 on June 1st and a check #123 for $1,000 on June 3rd. Step #3 Identify items that have hit the company records but are missed on the bank statement.

Manually reconciling bank statements. A report by Oxford University concluded that there was a 99% chance that tax preparers’ jobs would be automated and a 98% chance that it will happen to bookkeepers and accountants. We rely on bank and credit card transaction data to help us reconcile a set of accounts. Easy peasy!

As a matter of fact, by reconciling payments regularly, businesses can quickly detect discrepancies, such as missed or duplicate payments, incorrect amounts or unauthorized transactions. When payments are reconciled promptly, businesses have a clearer understanding of their incoming revenue, allowing for better planning and forecasting.

Many small business owners undervalue the importance of a tax expert, but your business can work much better with the help of a tax preparer. A tax preparer gives you peace of mind to work on what matters. You also have the certainty that your taxes are in order and you are making the most deductions.

We will cover everything you need to know , from tracking expenses and invoices to reconciling bank statements and choosing the right bookkeeping software. Accurate financial records can simplify tax preparation, inform business decisions, and ensure legal and financial compliance.

By comparing and reconciling expenses against various financial documents, businesses can detect and correct any discrepancies or errors, ensuring that their financial statements reflect the true state of their finances. Compliance and Regulation : Expense reconciliation is crucial for compliance with financial regulations and standards.

Our blogs regularly detail how professional bookkeeping can help businesses survive and thrive beyond simply recording transactions and preparing tax filings, like driving profitability with financial reporting , forecasting cash flow , and optimizing your accounts receivable. To list just a few: Accounts receivable reconciliation.

It ensures that all bank transactions, including deposits, withdrawals, and bank fees, are accurately recorded in the general ledger. Inventory Reconciliation : Inventory reconciliation involves reconciling the quantities and values of inventory recorded in the general ledger with the actual physical inventory on hand.

The bookkeeper also reconciles accounts to ensure their accuracy. The creation of financial transactions includes posting information to accounting journals or accounting software from such source documents as invoices to customers, cash receipts , and supplier invoices.

After that, we obtain the documents we need from our clients, anything from bank statements to a copy of their last business tax return. You’ll generally be recording expenses, deposits, and transfers from the bank feeds. You’ll need to reconcile the bank and credit card statements. 3: Kickoff meeting.

Tax preparation : Bank statements are valuable for tracking deductible expenses and verifying income when preparing tax returns. Accounting: For companies, bank statements are crucial for reconciling accounts and ensuring accurate financial records. Look for data entry errors on the bank statement.

Recording transactions, Managing accounts receivable and payable, Monitoring the cash flow, Reconciling bank accounts, Creating journal entries, Issuing invoices, Payroll tax preparation, income tax, sales tax, tax return, etc. A full-charge bookkeeper is not a certified public accountant.

It enables you to monitor cash flow, build strong relationships with vendors, comply with tax regulations, and demonstrate financial transparency to stakeholders. You use direct deposit to transfer funds into her employees' bank accounts. Tax Payment Disbursement Using disbursement for quarterly estimated tax payments.

The information included on a sales order may extend beyond the order details, often including customer shipping information, deposit and balance information, and space for signatures. Deposit and Balance Details Indicates the amount of any deposit paid by the customer and provides information on any outstanding balance.

Once approved, the reconciled data is securely stored in a centralized database, ensuring an auditable trail. It quickly matches cash outgoings and receipts, reconciles bank accounts with accounting records, and verifies totals against balance sheets, cash flow statements, and income statements.

Accounting professionals often find themselves wrestling with mundane tasks: reconciling transactions, generating reports, or manually inputting data, leaving them little time for value-added activities. GST Invoicing: Invoicera ensures GST compliance with accurate tax calculations, making invoicing easy while adhering to GST requirements.

Tasks with deadlines, like tax preparation, need to be logged and then assigned to team members so that you can all collaborate together. With accounting firms & tax professionals having hundreds and even thousands of tasks across the business, you’ll need more than Quickbooks Online or Xero. kinda like your tax software).

Tax returns: Bank extraction software can be used to extract income and employment details from tax returns for customer onboarding and loan approvals. It typically includes information such as deposit and withdrawal transactions, account balances, and any fees or charges.

Key aspects of bank statement analysis Transaction categorization: Classify entries as deposits, withdrawals, transfers, payments, etc. Taxation and accounting In taxation, bank statement analysis helps verify income, track deductible expenses, and ensure accurate tax filings.

This feature makes it easier to process and check the Indian tax laws to avoid any legal challenges. Invoice Taxation: Automate tax calculations and application to your invoices, guaranteeing compliance with a wide range of tax laws. It helps you reconcile transactions quickly and get real-time insights into your spending.

This makes it difficult for them to reconcile their general ledger, chase down any errors, and can ultimately slow down the accounting cycle overall. It makes supplier onboarding easy, reduces the cost of processing every invoice, and has built-in tax compliance capabilities on a global scale.

Oh, I got to talk to my accountant and I talked to my tax rep, I talked to my CPA. Right now it's tax season we're having to, we're doing tax returns where, you know, if you're in public accounting you're in the grind right now. So a quick example would be tax returns. A lot of clients see us as an expense.

Top features: Real-time feeds on existing credit cards Reimburses employees on time with ACH payments Pros: Real-time credit card reconciliations for cards like Visa, Mastercard, AmEx, etc.

InnovateX adopted an expense system that automatically updated with the latest tax and regulatory requirements, ensuring compliance and avoiding a potential hefty fine due to an overlooked tax regulation. With ever-changing regulations, managing compliance manually is like juggling dynamite.

I am CEO and founder of Reconciled. If you have been paying payroll tax, you'll have all of that. There's gonna be a process for it of being able to prove, from your taxes and what you filed. When we're talking for the PPP, if you employ people, it's people on payroll, you pay payroll taxes for. They don't.

Payment Terms The Buyer shall pay the Supplier 30% of the total Price upon the execution of this Agreement as a deposit. Tax (10%): $77.50 Reconciliation and Record Keeping Process: The finance department periodically reconciles the payments made with the bank statements to ensure accuracy. 1002 Bluetooth Keyboard 5 $45.00 $225.00

I've got follow up on Wirecard, the Ernst & Young audit that apparently did not detect $2 billion in money that was missing. David Leary: [00:04:18] I've got some Wirecard, as well. Blake Oliver: [00:04:19] IRS news, appropriate for Tax Day coming up. 2 Was Key to the Firm’s Rapid Rise. . - PPP, of course, is still in the news.

So at the end of the month, instead of reconciling which you need to do, which is reviewing every transaction in your bank account versus what you think it is. the two deposits on the 15th and the 30th and one, two, three transfers to your expense account just to cover your expenses. And the other one, it's just your expense account.

Bank feed integration allows your bank transactions deposits, payments, transfers to sync directly into your accounting platform. With bank feeds, transactions appear in your accounting system in real time, ready to be categorised and reconciled. This leads to more accurate books and less stress during tax season.

If you've ever tried to get your clients' Stripe, Square, or PayPal transactions into QuickBooks or Xero, you've probably pulled your hair out a few times trying to get income and fees recorded correctly so that the deposit amounts match the bank statement so you can reconcile. David Leary: [00:12:44] Yeah.

We organize all of the trending information in your field so you don't have to. Join 52,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content