QuickBooks Online Now Offers Shipping

Insightful Accountant

AUGUST 11, 2024

Murph takes you step-by-step through configuring the new QBO shipping feature, setting up your ShipEngine account, and processing your first shipment.

Insightful Accountant

AUGUST 11, 2024

Murph takes you step-by-step through configuring the new QBO shipping feature, setting up your ShipEngine account, and processing your first shipment.

Accounting Tools

AUGUST 11, 2024

What is a Process Costing System? A process costing system accumulates costs when a large number of identical units are being produced. In this situation, it is most efficient to accumulate costs at an aggregate level for a large batch of products and then allocate them to the individual units produced. The assumption is that the cost of each unit is the same as that of any other unit, so there is no need to track information at an individual unit level.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

Nanonets

AUGUST 11, 2024

Quickbooks is an accounting software that helps small and medium businesses perform financial operations such as expense tracking, reconciliation, and invoicing. Quickbooks imports transaction data from uploaded bank statements to perform financial operations. In order to import transaction data, bank statements need to be uploaded in Quickbooks supported formats such as Quicken (QFX), QuickBooks Online (QBO), Quickbook Supported CSV, or Microsoft Money (OFX).

Accounting Tools

AUGUST 11, 2024

Who are the Users of Financial Statements? There are many users of the financial statements produced by an organization. The following list identifies the more common users and the reasons why they need this information. In short, there are many possible users of financial statements, all having different reasons for wanting access to this information.

Speaker: Dave Sackett

Traditional budgeting and forecasting methods can no longer keep pace with today’s rapidly evolving business environment. Static budgets, rigid annual forecasts, and outdated financial models limit an organization’s ability to adapt to market shifts and economic uncertainty. To stay ahead, finance leaders must leverage a future-forward approach—one that leverages real-time data, predictive analytics, and continuous planning to drive smarter financial decisions.

Nanonets

AUGUST 11, 2024

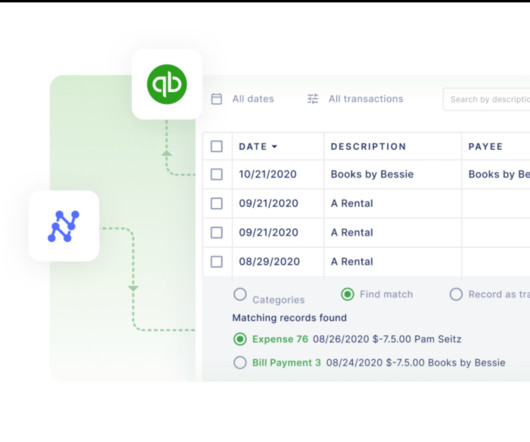

Businesses often use a third-party finance and accounting software, such as Quickbooks, to process financial and transactional data for efficient accounting and financial due diligence. A firm’s financial data is mostly present in PDF documents such as invoices, receipts, bank statements, and purchase orders. However, financial data in this form cannot be uploaded or imported directly into Quickbooks.

Accounting Tools

AUGUST 11, 2024

When to Classify an Asset as a Fixed Asset When assets are acquired, they should be recorded as fixed assets if they meet the following two criteria: Have a useful life of greater than one year; and Exceeds the corporate capitalization limit. The capitalization limit is the amount of expenditure below which an item is recorded as an expense , rather than an asset.

Financial Ops World brings together the best financial operations content from the widest variety of thought leaders.

Accounting Tools

AUGUST 11, 2024

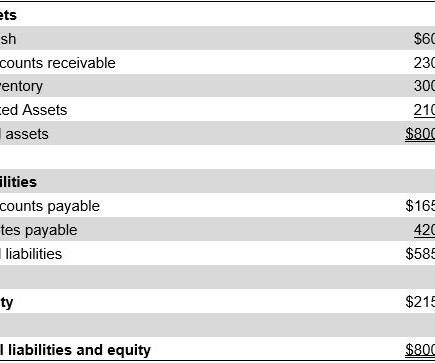

What is an Unclassified Balance Sheet? An unclassified balance sheet does not provide any sub-classifications of assets , liabilities , or equity. Instead, this reporting format simply lists all normal line items found in a balance sheet in their order of liquidity , and then presents totals for all assets, liabilities, and equity. This approach does not include subtotals for any of the following classifications: Current assets Long-term assets Current liabilities Long-term liabilities A balance

Accounting Tools

AUGUST 11, 2024

What is a Labor Rate? A labor rate is the cost of labor that will be charged or incurred over a specific period of time. It is most commonly expressed as an hourly rate, but may also be quoted or calculated on a daily, weekly, or monthly basis. Labor rates are used to determine both the price of employee time charged to customers , and the cost of that employee time to the employer.

Expert insights. Personalized for you.

Let's personalize your content