This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

As tax season approaches, many small business owners find themselves scrambling to organize their financialrecords and ensure they comply with the intricate web of tax regulations. The IRS requires businesses to keep detailed records of all financial transactions. Get Caught Up Overwhelming by bookkeeping backlog?

Reconciled bank statements monthly, maintaining accurate financialrecords. Generated monthly financial reports, including profit and loss statements and balance sheets. Reconciled bank statements and cash accounts, maintaining accurate financialrecords.

Account management: They manage accounts payable and receivable, process invoices, reconcile accounts, and ensure timely payments and collections. Basic financial reporting: They generate basic financial reports, such as income statements and balance sheets, summarizing financial activity for a specific period.

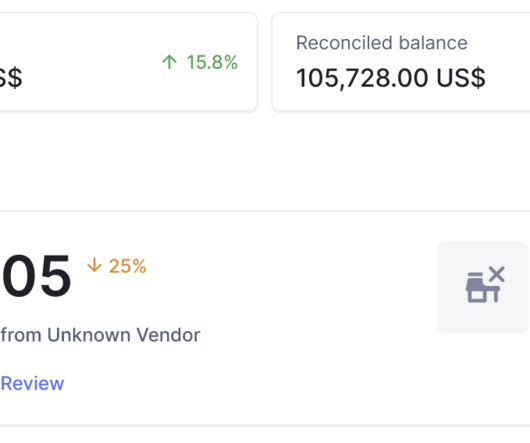

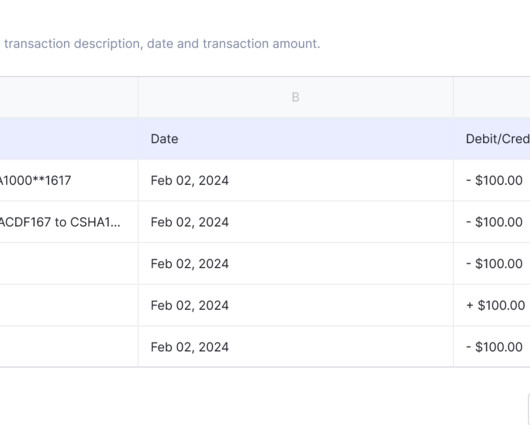

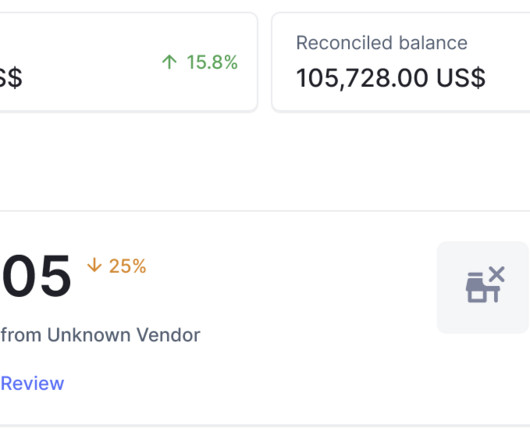

Why is it Important to Reconcile your Bank Account? Reconciliation is a crucial accounting process that ensures the accuracy of the financial close process. Reconciling the bank statement involves comparing the company's internal financialrecords or ledger to the bank statement received via the bank.

While its not an extension to pay taxes owed, it grants businesses the flexibility to organize their financialrecords. This extension offers invaluable support for companies managing complex financials or experiencing delays in gathering necessary documents. Alternatively, they could incur penalties and interest.

While its not an extension to pay taxes owed, it grants businesses the flexibility to organize their financialrecords. This extension offers invaluable support for companies managing complex financials or experiencing delays in gathering necessary documents. Alternatively, they could incur penalties and interest.

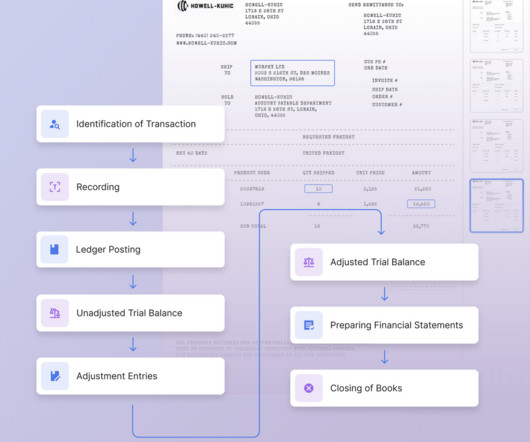

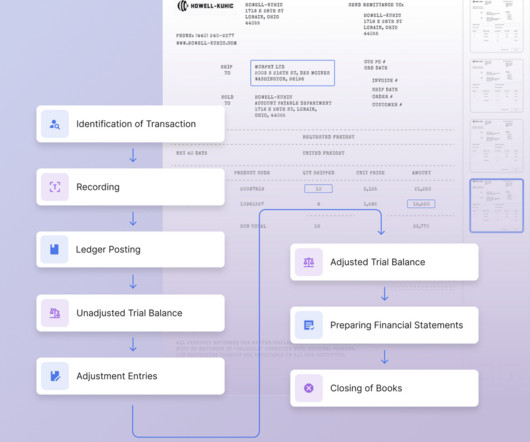

The end of month close process plays a vital role in ensuring the accuracy, integrity, and transparency of financialrecords for businesses of all sizes. Its primary purpose is to ensure the accuracy and completeness of financialrecords so that financial statements can be prepared for internal and external reporting purposes.

By evolving your bookkeeping process, you can be more confident that your financialrecords are accurate and up-to-date. You will be able to reconcile accounts faster and more accurately. Since bookkeeping is critical to running a successful business, the process must continually improve over time as the business grows.

Bookkeeping is the process of recording and organizing all financial transactions for your business. It involves tracking every dollar that goes in and out of your accounts, ensuring your financialrecords are accurate and up to date. While bookkeeping and accounting are often used interchangeably, they are different.

Types of Accounting Services and Their Cost Factors The cost of accounting services largely depends on what you need from basic bookkeeping to comprehensive financial management. Bookkeeping Typically charged monthly or quarterly, bookkeeping services involve recording daily transactions, reconciling bank statements, and maintaining ledgers.

Take a look at this bookkeeping cleanup checklist to get all your financial ducks in a row. Collect all your financialrecords It’s hard to say which part of this process is the most difficult, but depending on the type of business you have, rounding up all your past financialrecords may be the most time-consuming.

Use Clearing Accounts Clearing accounts serve as a pivotal tool in preventing A/R fraud by centralizing and reconciling all related transactions, thereby enabling companies to promptly identify and investigate anomalies that could indicate fraudulent activities.

Accounts receivable reconciliation is a crucial process within accounting and financial management practices undertaken regularly by a business. Reconciling accounts receivable involves comparing the balances in the accounts receivable ledger with supporting documentation, such as invoices, receipts, and customer payments.

Picture this: a team of expert bookkeepers diligently managing your financialrecords and transactions without setting foot in your office. These professionals play a crucial role in ensuring the accuracy and integrity of a company's financialrecords. Sounds futuristic?

The role of payment reconciliation in maintaining financial accuracy is critical, as it helps businesses track their income, verify the legitimacy of transactions and prevent discrepancies. Accurate financialrecords are essential for businesses to meet auditing requirements and avoid potential fines or penalties for non-compliance.

Heres how SMEs in Singapore can use ChatGPT to improve efficiency, particularly in managing financial and operational tasks. Streamlining Financial Reporting and Documentation For many SMEs in Singapore, managing financialrecords and preparing reports is a time-consuming task.

Review and ReconcileFinancialRecords Before filing your taxes, take the time to review and reconcile your financialrecords for accuracy. Ensure that all income and expenses are properly recorded, and resolve any discrepancies or errors.

Expense reconciliation is a process within finance and accounting that ensures that a company's financialrecords accurately reflect its spending activities. At its core, it involves comparing financial data from various sources within a business to identify any discrepancies or errors and bring them into alignment.

A Bank Reconciliation Statement is a financial document that ensures that the cash balances recorded in the internal financialrecords align with the financialrecords presented in the bank statement. General Ledger ) and the bank’s records (e.g. Bank Statement ).

That’s because you have a moral and legal responsibility to protect your client’s financialrecords. Keep on Reconciling When a human is inserting information into the machine, there is a very high chance that an error might occur. Create Backup You can secure your data on QuickBooks by backing it up.

Introduction Diving into the world of accounting, reconciling accounts becomes a routine yet crucial task, especially when bank or credit card statements roll in. However, the dynamic nature of business means changes or oversights can occur, necessitating a revisit to previously reconciled accounts. The answer is a Yes.

In the world of finance and accounting, the process of reconciliation plays a vital role in ensuring accurate and transparent financialrecords. It is a crucial process for businesses to identify discrepancies, resolve errors, and maintain the integrity of their financial statements.

We will cover everything you need to know , from tracking expenses and invoices to reconciling bank statements and choosing the right bookkeeping software. Establishing a record-keeping system for tracking income and expenses is essential. To reconcile your bank statements, you’ll need to take a few simple steps.

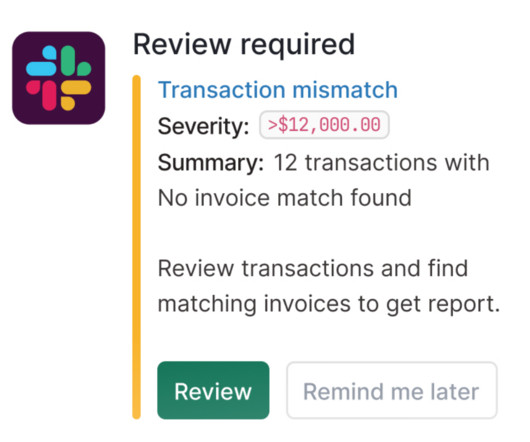

Need for Account Reconciliation Account Reconciliation ensures the accuracy and integrity of financialrecords by identifying discrepancies and errors, thus fostering trust among stakeholders and facilitating informed decision-making. Make Adjustments: Record missing transactions and correct errors for accurate balances.

Efficient reconciliation of payments is a vital aspect of financial management for businesses of all sizes. As transactions flow in and out, reconciling payments becomes crucial to ensure accuracy, identify discrepancies, and maintain a clear financial picture. Why is payment reconciliation crucial for businesses?

Maintaining accurate financialrecords is vital for any business, and the general ledger, as the central repository of financial transactions, plays a critical role in this process. The process may vary depending on the complexity of the organization and the specific accounts being reconciled.

Below are some of the main benefits of implementing this automation into your workflow: Time Efficient Bookkeeping Manually logging into various banking platforms, downloading bank statements, and reconciling the transactions one by one, can quickly become very time-consuming. Bookkeepers are no strangers to this concept.

Book Reconciliation entails the comparison of different types of financialrecords of a company. These records may be internal financialrecords or external. Companies maintain various internal records to track their financial activities accurately and ensure compliance with accounting standards.

If they match, it means your records and the bank statement are reconciled, and there are no discrepancies. Why is it important to reconcile your bank statements? It's important to reconcile bank statements to identify errors, detect fraud, and maintain an accurate ledger.

If they match, it means your records and the bank statement are reconciled, and there are no discrepancies. Why is it important to reconcile your bank statements? It's important to reconcile bank statements to identify errors, detect fraud, and maintain an accurate ledger.

There seem to be so many ways to mess up your financialrecords without knowing it. Bookkeeping is not for the faint of heart. But don’t worry, a lot of these mistakes are common, and, most importantly, they are correctable if they are caught early enough. This can result in errors and missed discrepancies.

Introduction to Bank Reconciliation Journal Entries Bank reconciliation is an important process in accounting that ensures the accuracy and integrity of a company's financialrecords. It involves the comparison between the company’s internal financialrecords and those of the bank.

As we approach the end of the year, it’s essential for small business owners to review their financialrecords and ensure everything is in order. Reconcile Bank Accounts Ensure your bank statements align with your accounting records. This step helps maintain accuracy in your financialrecords.

Invest in accounting software or hire a professional bookkeeper to maintain organized and up-to-date records. Failure to Reconcile Bank Statements: Ignoring bank reconciliation is a recipe for disaster. Failing to reconcile your bank statements regularly can result in missed transactions, overdrafts, and errors in financial reporting.

The Critical Role of Clean FinancialRecords At the heart of every successful business is the ability to make informed decisions. Clean financialrecords provide a clear picture of a company’s financial health, enabling business owners to confidently make strategic choices. We can help!

Finance reconciliation plays a pivotal role in ensuring the reliability and accuracy of a business's financialrecords. This essential practice involves comparing transactions and other financial activities with supporting documentation and resolving any discrepancies that may arise. What is finance reconciliation?

There seem to be so many ways to mess up your financialrecords without knowing it. Bookkeeping is not for the faint of heart. But don’t worry, a lot of these mistakes are common, and, most importantly, they are correctable if they are caught early enough. This can result in errors and missed discrepancies.

Effective financial management is crucial for the success and growth of any business. One important aspect of financial management is invoice reconciliation. The primary goal of invoice reconciliation is to ensure that the financialrecords of a business are accurate, complete, and in alignment with the goods or services received.

With disconnected data sources and innumerable documentation, accounting teams can face the added task of figuring in interest rates, exchange rates, and timing differences to reconcile balances effectively. Account Reconciliation can be a fairly manual task, especially right before the monthly close. Retain all supporting documentation.

A Guide to NetSuite Account Reconciliation Accurate financialrecords are an important part of any business’ ability to make informed decisions and also adhere to legal regulations. NetSuite Account Reconciliation Software Overview NetSuite offers robust account reconciliation software as part of its comprehensive ERP suite.

This article highlights the importance of bank reconciliation, and its role in maintaining financial control, accountability, and protection against errors and fraud. Bank reconciliation involves comparing a company's internal financialrecords with those provided by the bank. What Is a Bank Reconciliation?

Accounts Payable Reconciliation : Accounts payable reconciliation entails verifying that the transactions recorded in the general ledger align with the amounts owed by the company to its suppliers and vendors as reflected in accounts payable reports or invoices.

Whether it's ensuring that expenses align with available funds or guaranteeing that business transactions accurately reflect the company's financial standing, tracking checks outstanding and reconciling bank statements is non-negotiable.

Best Reconciliation Software Tools Reconciliation software is a tool specifically designed to compare financial data from different sources such as invoices, bank statements, general ledgers, and other financialrecords. If Pricing is an issue you may try to use Power Query to reconcile in excel. Use CubeSoftware.

We organize all of the trending information in your field so you don't have to. Join 52,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content