This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Skilled in all aspects of bookkeeping, including accounts payable/receivable, bank reconciliations, payroll processing, and financialreporting. Reconciled bank statements monthly, maintaining accurate financial records. Generated monthly financialreports, including profit and loss statements and balance sheets.

Regulatory bodies may use them to ensure companies comply with financialreporting standards. Account management: They manage accounts payable and receivable, process invoices, reconcile accounts, and ensure timely payments and collections.

In todays fast-paced business environment, achieving financial accuracy is critical for maintaining stakeholder trust and ensuring compliance with accounting standards. One cornerstone of accurate financialreporting is the matching principle in accounting, a concept that ensures revenues and expenses are recorded in the same period.

Streamlining FinancialReporting and Documentation For many SMEs in Singapore, managing financial records and preparing reports is a time-consuming task. ChatGPT can assist in summarising financial documents, creating templates for reports, and organising your records to ensure everything is in order.

However, simply recording transactions in the general ledger is not sufficient to ensure accurate financialreporting. It involves comparing and matching the account balances in the general ledger with supporting documentation, such as bank statements, invoices, receipts, and other financial records.

Not Reconciling Accounts Payable and Receivable Why This Happens: In the rush of running a business, SMEs in Singapore often overlook regular reconciliation, leading to discrepancies that can affect cash flow. Example: Bens construction company in Singapore didnt track overdue invoices, leading to cash shortages just before payroll.

Its primary purpose is to ensure the accuracy and completeness of financial records so that financial statements can be prepared for internal and external reporting purposes. As part of the process, the AP team takes steps to ensure the past month’s financial records are accurate.

The 10 Best Accounts Receivable Reporting Software of 2025 Different accounts receivable reporting software offer various automation and AI capabilities, functionality, and specialization for a variety of target audiences. You can also build your own specialized reports that answer your specific business needs.

It can help save time on financial processes like analyzing payments and keeping track of payment deadlines. Offering timely visibility into spending and fund allocation, spend management software helps businesses keep campaigns moving.

Collect all your financial records It’s hard to say which part of this process is the most difficult, but depending on the type of business you have, rounding up all your past financial records may be the most time-consuming. They can provide you with a printout list of each transaction or invoice between you.

Why is it Important to Reconcile your Bank Account? Reconciliation is a crucial accounting process that ensures the accuracy of the financial close process. Reconciling the bank statement involves comparing the company's internal financial records or ledger to the bank statement received via the bank.

It will also give you a great picture of your business’s overall financial health. Reconcile Accounts You won’t get far if your books aren’t up to date. Take the time to reconcile bank statements, credit card statements, and any other financial accounts. The same goes for your own bill payments.

However, most of the time goes into manually entering invoice data into Excel. And invoices come in all formats, word, excel, PDF, text, scanned images, or handwritten notes. Fortunately, PDF to-Excel converters streamline converting PDF invoices into Excel spreadsheets. Why should you convert PDF invoices to Excel spreadsheets?

The efficiency in organizing financial documents, such as tax records, invoices, receipts, bank statements, and reports can make a significant difference on their own efficiency and success and the organization’s compliance. Depending on how often the client creates reports. ex: “ClientName_Invoice001.pdf”)

Paperless document management allows you to upload, store, and manage your financial documents in one central location. With LedgerDocs, you can easily upload receipts, invoices, and other financial documents by scanning them or taking a picture with your smartphone.

If you're looking to streamline your invoicing, you're making a smart move that could save your company time and money. Many businesses face challenges with invoice processing —from data entry errors to delayed payments. Modern invoice management tools automate much of the process. Let's get started.

Introduction Have you ever found yourself juggling incomplete payments on your invoices? Imagine sending out a substantial invoice for a project, eagerly anticipating the full payment to fuel your operations, only to receive a fraction of the expected amount. ” In this case, the right tool is an invoicing solution like Invoicera.

Introduction Have you ever found yourself juggling incomplete payments on your invoices? Imagine sending out a substantial invoice for a project, eagerly anticipating the full payment to fuel your operations, only to receive a fraction of the expected amount. ” In this case, the right tool is an invoicing solution like Invoicera.

Their responsibilities often include: Data Entry: Traditional bookkeepers manually record financial transactions, including sales, purchases, receipts, and payments, into ledgers or accounting software. Whether managing expenses, invoicing clients, or tracking revenue, virtual bookkeeping ensures remote teams stay organized and informed.

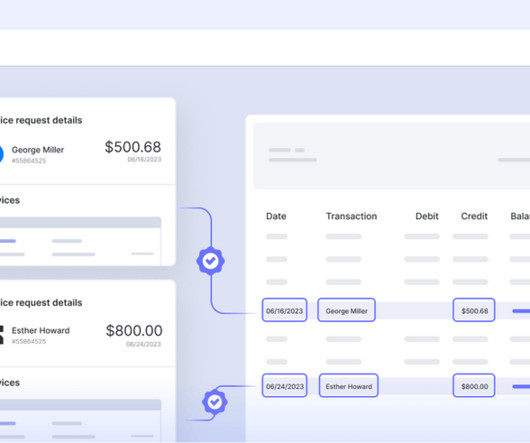

Reconciling accounts receivable involves comparing the balances in the accounts receivable ledger with supporting documentation, such as invoices, receipts, and customer payments. This process helps identify discrepancies, resolve outstanding balances, and maintain a clear understanding of the company's financial position.

Not only is this simplified to your accounting solutions for ecommerce, but it also facilitates proactive decision-making with precise financialreports at your disposal. Establish Financial Goals and Monitor Progress Don’t do it without goals. Moreover, when audited, well-organized records prove to be lifesavers.

Settlement of invoices isn’t simply about paying off a bill. It's a process that ensures every payment, adjustment, or write-off tied to an invoice is accounted for and settled. It paves the way for flawless financial records, better cash flow, and smooth business operations. What is the settlement of an invoice?

Yet, the leap from traditional bookkeeping to a streamlined, automated financial ecosystem is one that many QuickBooks users are yet to fully embrace. Error-Prone Transactions : The human factor introduces a margin for error in data entry, leading to discrepancies that can cascade through financialreporting. in real time.

Invoicing, bank reconciliations, bank and credit card feeds, financialreporting, managing accounts payable and accounts receivable, multi-currency, and the ability to connect to 100’s of 3rd party apps to help small businesses automate all parts of the accounting process. Ready to dive in? 11) Dext I love me some Dext.

To effectively manage procurement and financial processes, it is crucial to understand the distinction between a purchase order and an invoice. On the other hand, an invoice is sent by the seller to request payment once the order is fulfilled.

Has the manual effort of the invoicing process turned into daunting tasks that are resulting in errors and revenue loss? The research further concluded that the most common pain points for organizations are manual data entry (71%), manual routing of invoices for approval (61%), and lost or missing invoices (42%).

Invoice automation solutions control how customers pay and lower the investment cost on an Account Payable (AP) team. The AP team manages customer service and orders and tackles the arduous task of keying hundred of invoices and verifying them against their original purchase orders. It is a laborious and time-intensive task.

Recording accrued revenue involves double-entry bookkeeping and often requires subsequent reversal entries when payment is invoiced or received. So this fills this gap by recognizing income tied to obligations fulfilled before payment is invoiced. goods or services have been provided), but hasn’t been invoiced or paid.

Sales orders and invoices are essential documents in business transactions, but they serve different purposes and play distinct roles in the sales process. On the other hand, an invoice is sent by the business to request payment from the customer after the products or services have been delivered.

During this process, you’ll reconcile transactions with accounts, categorize transactions for analysis and tax purposes, and handle any employee or vendor reimbursements. Financialreporting and forecasting: You will typically provide the company’s management team with regular financialreports, financial forecasts, and more.

Responsibilities of a Full Charge Bookkeeper The subject areas over which the full charge bookkeeper has responsibility are as follows: Record and pay accounts payable Issue invoices to and collect from customers Calculate pay and issue payments to employees Create financial statements and related financialreports Remit payroll taxes , sales taxes (..)

Accounts payable teams must reconcile payments regularly to avoid double-processing them. This means consolidating paperwork like vendor invoices, payment receipts, and bank statements. Examine Vendor Invoices: It is critical to examine each vendor's invoice details and check for human-made errors.

Failure to Reconcile Bank Statements: Ignoring bank reconciliation is a recipe for disaster. Failing to reconcile your bank statements regularly can result in missed transactions, overdrafts, and errors in financialreporting. Take the time to properly classify expenses according to their nature (e.g.,

How to conduct Account Reconciliation The process of Account Reconciliation involves several key steps to ensure accuracy and completeness: Gather Documents: Collect financial records like bank statements, invoices, and ledger entries.

A balance sheet is a financial statement that provides a snapshot of a company's financial position at a specific point in time. Balance sheet reconciliation is a critical financial process that aligns the financial statements with external documentation such as bank statements, invoices, and general ledger entries.

However, with a shift towards Workflow Automation, application of AI is going beyond automating specific tasks but instead automating entire workflows including Accounts Payable, Accounts Receivable, Financial Close, FinancialReporting and Audits.

Here are some examples: · Bank Statements · Credit Card Statements · Vendor Invoices · Customer Invoices · Loan Agreements · Lease Agreements · Insurance Policies · Government Tax Notices. Any discrepancies, such as incorrect calculations or missed payments, are corrected.

It helps you keep track of your expenses, invoices, and bank statements, and allows you to make informed decisions about the future of your business. We will cover everything you need to know , from tracking expenses and invoices to reconciling bank statements and choosing the right bookkeeping software.

Discrepancies in your financialreports could lead to inaccurate data for future decisions, a mistake that could quickly spell disaster for any business. However, this frequently doesn’t happen due to a lack of reconciling items. That’s where reconciling a loan ledger to the balance in the statement comes in.

It is a record of all financial transactions of an enterprise and provides a comprehensive account of the organization's monetary activities. However, the GL is not the sole repository of financial data. It helps in identifying any discrepancies or overdue payments that need to be addressed.

Essentially, it involves comparing payment details from sources like invoices, bank statements and credit card transactions to confirm that the business has received and processed all payments correctly. The process begins by collecting all payment data from these sources, including invoices, receipts and bank statements.

Matching and validating entries would mean data consolidation across sub-ledgers, vendor invoices, bank statements, receipts, and account receivables to ensure timely and accurate month-end and year-end closing of the financial books. Account reconciliation is essential to ensuring the accuracy and integrity of financialreporting.

Otherwise, you may be able to enter expense data into an AI model directly with some context and explanations for your expense categories to automate classification and generate expense reports more quickly. Reconciling Accounts AI tools can help accountants work more efficiently.

Organize Receipts and Invoices Gather all receipts, invoices, and financial documents. Reconcile Bank Accounts Ensure your bank statements align with your accounting records. Reconcile bank accounts to identify discrepancies, such as outstanding checks or unrecorded transactions.

We organize all of the trending information in your field so you don't have to. Join 52,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content